Fairfax Financial Holdings (TSX: FFH) delivered a steady 0.61% gain on December 24, 2025, closing at a robust CAD 2,584.28. While the broader market often winds down for the holidays, Fairfax continues to attract "smart money" investors. Known as the "Berkshire Hathaway of Canada," this insurance-investment hybrid is proving that its dual-engine model—disciplined underwriting and aggressive value investing—is a powerhouse for the 2026 outlook.

Key Drivers: Why FFH is Trending Up

The modest gain on Christmas Eve is the "cherry on top" of a massive year. Here are the catalysts:

Source: Kalkine Group

- Earnings Beat & Momentum: Following its Q3 2025 report, Fairfax has consistently outperformed analyst expectations, posting EPS of $52.04 (beating the $41.00 estimate). This "halo effect" has carried the stock to new 52-week highs.

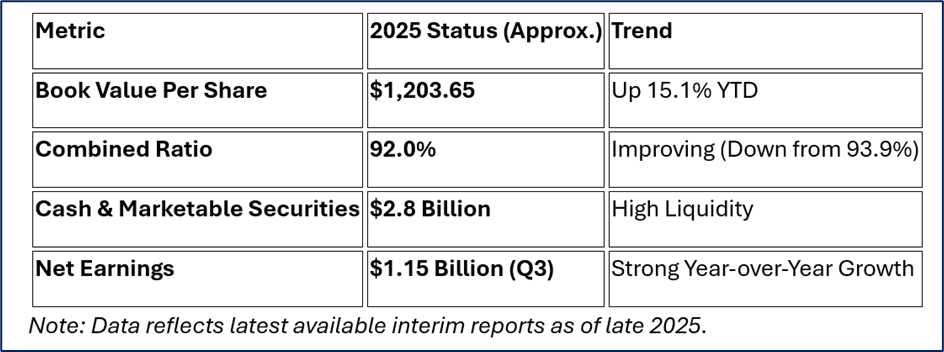

- Operational Efficiency: A consolidated combined ratio of 92.0% in late 2025 signifies high-profit insurance underwriting—every dollar in premiums is being managed with surgical precision.

- The "Euro" Play: The recent sale of an 80% stake in Eurolife for $945 million has injected significant liquidity, part of which is being re-allocated into higher-yield property and casualty (P&C) opportunities.

Latest Business Model & Strategy

Fairfax’s 2025 model is a refined version of Prem Watsa's "Total Return" philosophy. It operates on three distinct pillars:

- Core P&C Insurance: Leveraging global brands like Allied World, Odyssey Group, and Northbridge. The focus has shifted toward "increased retention," keeping more premium revenue in-house rather than ceding it to third-party reinsurers.

- The Investment Float: Fairfax manages a massive $70.9 billion investment portfolio. Unlike traditional insurers that stick only to bonds, Watsa utilizes the "float" to invest in undervalued equities and private companies.

- Strategic Divestment & Re-Focus: In late 2025, the company moved away from life insurance (Eurolife sale) to double down on high-margin commercial casualty lines in the US and emerging markets like India.

Financial & Operational Update (Q3/Q4 2025)

Source: Company Data

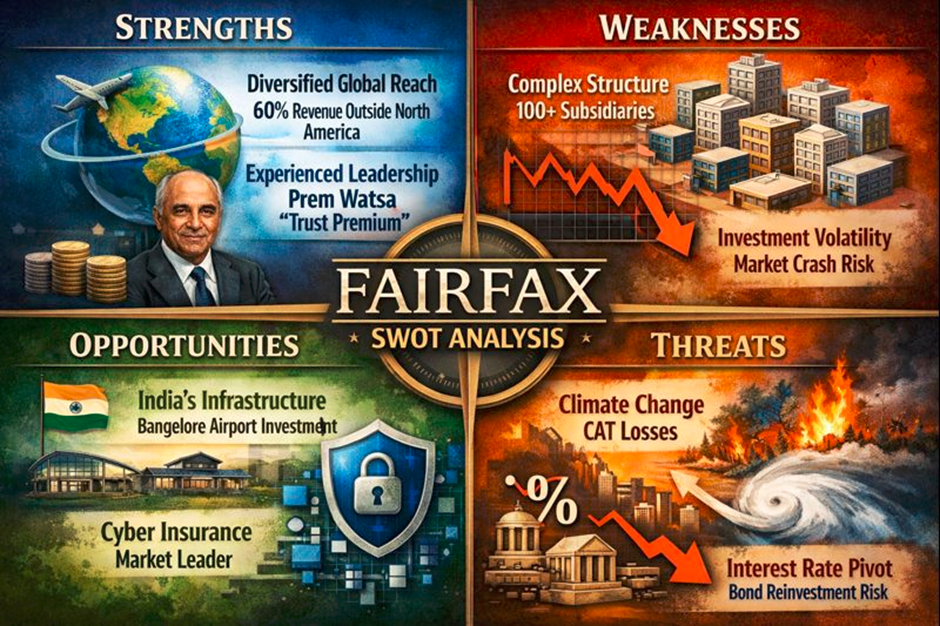

SWOT Analysis: The Analytical Deep Dive

Source: Kalkine Group

Strengths

- Diversified Global Reach: 60% of revenue originates outside North America, shielding the stock from localized economic downturns.

- Experienced Leadership: Prem Watsa’s 40-year track record of navigating market bubbles (like 2008) provides a "trust premium."

- Strong Credit: Recent upgrades by AM Best and S&P to "AA-" and "A+" levels lower the cost of borrowing.

Weaknesses

- Complexity: With over 100 subsidiaries, the corporate structure is often criticized as opaque by retail investors.

- Investment Volatility: Because Fairfax holds significant equity swaps and common stocks, a market crash can lead to large unrealized losses, even if the insurance side is healthy.

Opportunities

- India’s Infrastructure: Through Fairfax India, the company is heavily invested in Bangalore International Airport, poised to benefit from India's projected $1.4 trillion infrastructure boom.

- Cyber Insurance: A high-growth frontier where Fairfax is currently a market leader with profitable underwriting.

Threats

- Climate Change: Increased frequency of catastrophic (CAT) losses (wildfires, hurricanes) can spike the combined ratio unexpectedly.

- Interest Rate Pivot: As central banks shift rates, the yield on Fairfax’s $32.7 billion bond portfolio may face reinvestment risk.

Risks to Watch

Investing in FFH isn't without its "Watsa-sized" risks:

- Underwriting Pressure: While currently strong, a softening insurance market could lead to lower premiums.

- Concentration Risk: Heavy bets on specific sectors (like Indian finance or US casualty) mean the portfolio isn't as "indexed" as some might prefer.

- Foreign Exchange: As a global entity, a strengthening CAD can eat into international profits when converted.

Conclusion

Fairfax Financial is entering 2026 as a lean, high-performing machine. By trimming non-core assets (Life Insurance) and maintaining a pristine 92% combined ratio, the company has decoupled itself from the typical "boring" insurance stock profile. For retail investors, the stock represents a play on global value investing backed by a rock-solid insurance floor.

Please wait processing your request...

Please wait processing your request...