In the current 2026 market environment, global fund managers and institutional "smart money" are pivoting toward "quality defensives." With the TSX facing headwinds from subdued energy prices and geopolitical trade uncertainties—specifically the upcoming USMCA review—investors are seeking sanctuary in businesses with inelastic demand, pricing power, and robust dividend profiles.

The following three TSX-listed companies represent the premier "Volatility Hedge" for 2026, backed by latest analyst upgrades and operational stability.

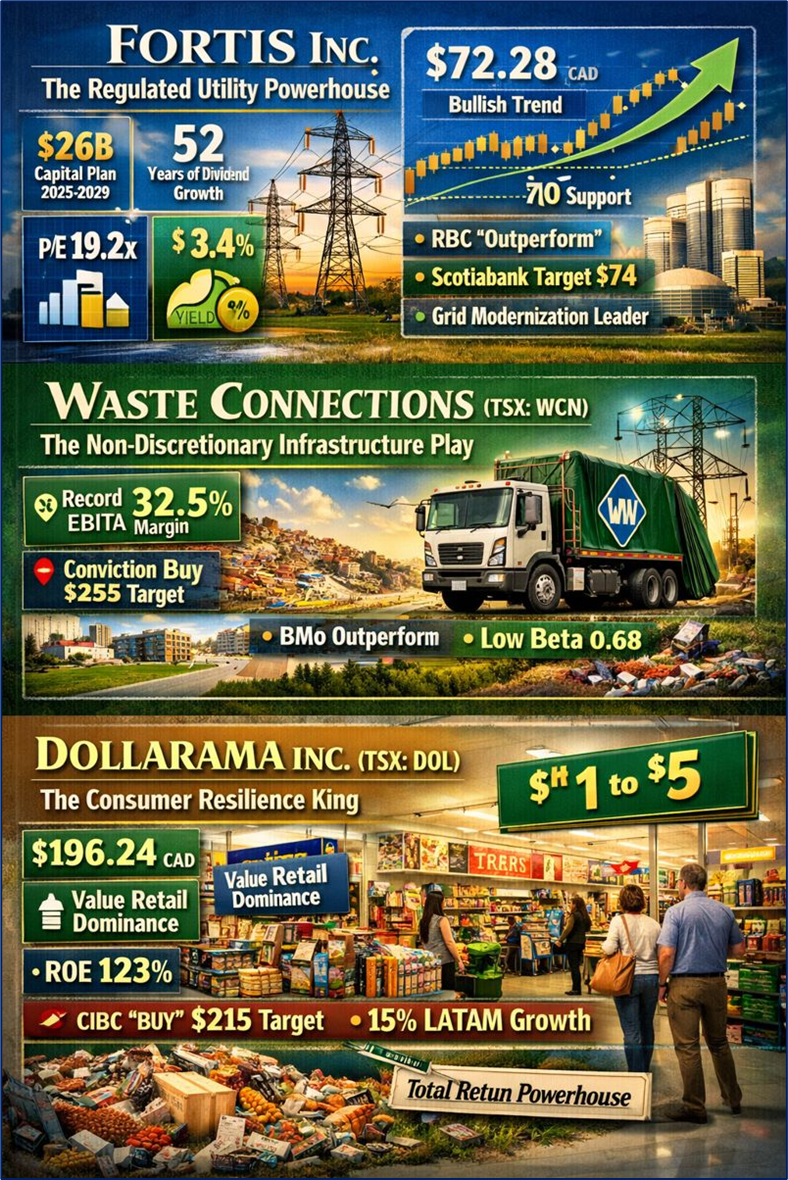

Source: Kalkine Group

Fortis Inc. (TSX: FTS)

The Regulated Utility Powerhouse

- Latest Key Reasons & Drivers: Fortis is benefiting from its massive $26 billion 5-year capital plan (2025–2029). As of early 2026, the primary driver is the "de-risking" of its rate base growth. With inflation stabilizing, the company’s regulated returns are more attractive to "smart money" seeking yield without exposure to cyclical downturns.

- Technical Analysis: Fortis is currently trading at CAD 72.28. Technically, the stock is exhibiting a strong bullish trend, trading significantly above its 200-day moving average. It recently broke through a key resistance level at $70.00, which has now transitioned into a support floor. The RSI (Relative Strength Index) is at 49.1, suggesting it is not yet overbought and has room for further appreciation within its current upward channel.

- Analysts Upgrades/Downgrades: In January 2026, RBC Capital Markets reiterated an "Outperform" rating, while Scotiabank raised its price target to $74.00, citing superior execution in the ITC transmission segment.

- Business Model: A diversified, regulated electric and gas utility leader with operations across Canada, the U.S., and the Caribbean. 99% of its assets are regulated, providing a virtual "moat" against economic recession.

- Dividend Analysis: FTS is a Canadian Dividend Aristocrat with 52 consecutive years of increases. The current yield is 3.4%. Management has reaffirmed a 4% to 6% annual dividend growth guidance through 2029.

- Valuation & Financials: Trading at a P/E of 19.2x, slightly below its historical premium. Recent operational updates confirm Q4 2025 earnings beat expectations, with net income rising 6% year-over-year.

- Outlook & Risks: Outlook remains stable with a focus on grid modernization. Risks include sudden spikes in long-term bond yields which can make utility yields less competitive.

Waste Connections, Inc. (TSX: WCN)

The Non-Discretionary Infrastructure Play

- Latest Key Reasons & Drivers: WCN is favored by hedge funds as a "pure-play" on essential services. The 2026 driver is the successful integration of recent regional acquisitions, which has boosted EBITDA margins to record levels of 32.5%.

- Technical Analysis: WCN is currently trading at 235.15 CAD. The stock is in a "discovery phase" near all-time highs. It has recently bounced off its 50-day moving average, signaling strong institutional "buying on the dip." Technical indicators show low volatility (Beta of 0.68), making it a preferred choice for low-variance portfolios.

- Analysts Upgrades/Downgrades: Goldman Sachs recently moved WCN to their "Conviction Buy" list for 2026, targeting a price of $255.00. BMO Capital upgraded the stock from Market Perform to Outperform this month.

- Business Model: Provides non-hazardous solid waste collection, transfer, and disposal services. It focuses on secondary or "exclusive" markets where competition is minimal, giving it unmatched pricing power.

- Dividend Analysis: The current yield is 0.75%. While the yield is low, the dividend growth rate has averaged 12% over the last five years, signaling a high-growth defensive profile.

- Valuation & Financials: Valuation is premium at 31x P/E, but justified by its 15% Free Cash Flow growth. Early 2026 operational updates show a 9% increase in revenue driven by price hikes that exceeded labor inflation.

- Outlook & Risks: Positive outlook due to its essential nature. Risks involve regulatory changes in landfill environmental standards and rising fuel costs for its fleet.

Dollarama Inc. (TSX: DOL)

The Consumer Resilience King

- Latest Key Reasons & Drivers: As Canadian consumers pivot to "value," Dollarama has captured massive market share in 2026. The latest driver is the outperformance of its Dollarcity stake in Latin America, which is contributing nearly 15% to its bottom-line growth.

- Technical Analysis: Dollarama is trading at 196.24 CAD. After hitting a 52-week high of $209.96, the stock has undergone a healthy 5% consolidation. It is currently testing support at its 100-day moving average. Support is firm at $195.00, with a bullish "MACD crossover" appearing on the daily chart, suggesting a potential rebound toward the $210 range.

- Analysts Upgrades/Downgrades: TD Securities maintained a "Buy" rating with a price target of $215.00 as of Jan 15, 2026. CIBC recently upgraded the stock, citing higher-than-expected "basket size" growth.

- Business Model: Canada's largest deep-discount retailer. The model relies on fixed price points ($1 to $5) and a massive private-label sourcing network that ensures high margins even during supply chain disruptions.

- Dividend Analysis: Yield stands at 0.22%. However, Dollarama is a "Total Return" play; it has returned over 46% to shareholders in the last 12 months through a combination of capital gains and aggressive share buybacks.

- Valuation & Financials: Trading at 42.1x P/E. While expensive, its ROE (Return on Equity) is a staggering 123%, among the highest on the TSX.

- Outlook & Risks: Guidance for 2026 suggests 4.5% same-store sales growth. Risks include a potential "thawing" of the economy which might lead consumers back to mid-tier retailers, and wage inflation in its 1,500+ store network.

Global Institutional Outlook for 2026

Major players like BlackRock, Franklin Templeton, and RBC Wealth Management are currently emphasizing a "Quality-First" approach. The consensus from the biggest global fund managers as of January 2026 is that the "Goldilocks" scenario (low inflation + high growth) is not yet guaranteed. Therefore, "overweighting" utilities (Fortis), waste management (WCN), and discount retail (Dollarama) provides the necessary defense to weather potential trade shocks or central bank pivots.

Please wait processing your request...

Please wait processing your request...