Mirasol Resources Ltd. (TSX-V: MRZ) delivered a staggering performance on January 23, 2026, with its share price catapulting 31.34% to close at $0.88. This sharp upward trajectory marks a significant breakout for the Vancouver-based explorer, which has now seen its valuation climb over 66% in the preceding two weeks. The surge reflects a convergence of high-conviction geological data, strategic capital infusion, and the commencement of a much-anticipated maiden drilling program in one of the world's most watched copper-gold jurisdictions. As the stock reaches a new 52-week high, the market appears to be pricing in the potential for a transformational discovery within the prolific Vicuña District.

Latest Key Reasons for the Surge and Latest Drivers

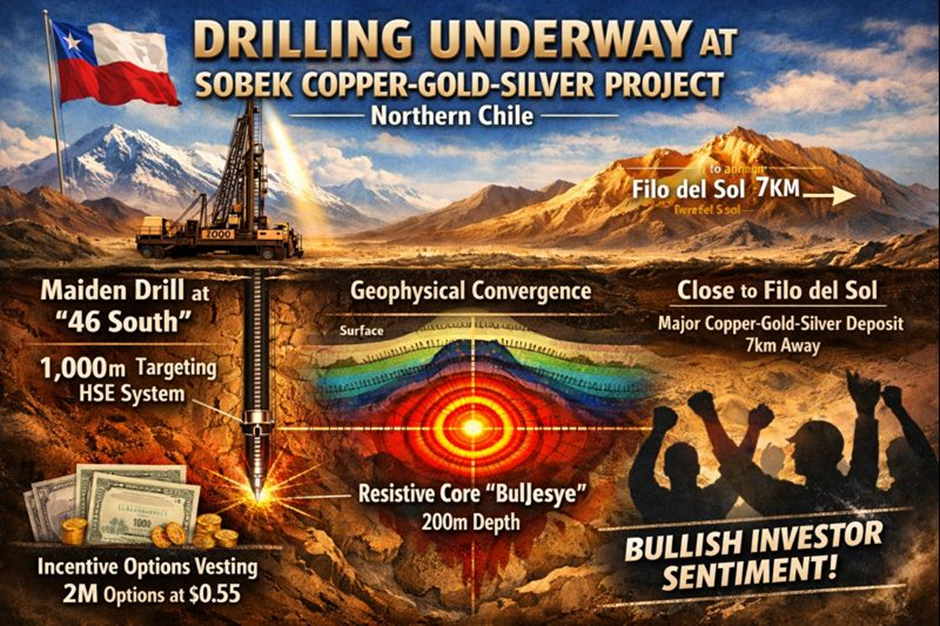

Source: Kalkine Group

The primary catalyst for the January 23rd surge was the company’s official announcement that drilling is now underway at the 100%-owned Sobek Copper-Gold-Silver Project in Northern Chile. Investors reacted bullishly to the technical specifics of the "46 South" target, which the company described as its most "technically compelling" to date.

- Maiden Drilling at 46 South: The market is responding to the initiation of a 1,000-meter drill hole targeting a high-sulphidation epithermal (HSE) system.

- Vicuña District Proximity: Sentiment is heavily influenced by Sobek’s location—just 7km west of the massive Filo del Sol deposit. In the exploration world, "closeology" to world-class discoveries often drives significant speculative premiums.

- Geophysical Convergence: Recent Deep Vectoring IP and MT surveys have defined a coherent resistive core starting just 200m below the surface, providing a clear "bullseye" for the current drill program (Mirasol Resources News Release, Jan 22, 2026).

- Vesting of Incentive Options: The recent grant of nearly 2 million options to directors and officers at $0.55 per share has been viewed by some as a sign of internal confidence ahead of the drilling results (Mirasol Resources News Release, Jan 24, 2026).

Current Business Model

Mirasol Resources operates as a Project Generator, a strategy designed to provide shareholders with multiple "shots on goal" while minimizing financial risk. This hybrid model allows the company to manage a large portfolio of early-stage assets across Chile and Argentina.

- Self-Funded Exploration: For high-conviction "flagship" assets like Sobek, Mirasol chooses to self-fund exploration to retain 100% ownership and maximize the value of a potential discovery.

- Strategic Partnerships: For other projects in its pipeline (such as Claudia or Nord), Mirasol seeks partners to fund the expensive drilling phase in exchange for an equity interest, while Mirasol retains a minority stake or a Net Smelter Return (NSR) royalty.

- Asset Monetization: The company actively sells non-core assets to fund its primary exploration goals, as seen with the recent sale of the Sascha-Marcelina projects (Mirasol Resources News Release, Dec 9, 2025).

Financial, Operational, and Dividend Updates (company sourced)

Based on recent company disclosures, Mirasol has significantly fortified its balance sheet to support the current drilling campaign.

- Financing: The company successfully closed a $3.01 million non-brokered private placement in late December 2025, issuing units at $0.45. This capital is specifically earmarked for the Sobek exploration program (Mirasol Resources News Release, Dec 16, 2025).

- Asset Sales: Mirasol completed the sale of the Sascha-Marcelina Projects to Pursuit Minerals for US$1.5 million plus a retained 1.5% NSR royalty. Proceeds were used to repay $2 million of an outstanding shareholder loan (Mirasol Resources News Release, Dec 9, 2025).

- Operational Focus: The current operational focus is 100% on the Sobek Project, specifically the 46 South target where a "chargeability neck" and "silica-rich core" have been identified through 3D inversion modeling.

- Dividend Status: As an early-stage exploration company, Mirasol does not pay a dividend and likely will not for the foreseeable future, as all available capital is reinvested into the ground to drive discovery (Mirasol Resources Website, Investor Relations).

- Financial Leadership: Francisco Del Castillo assumed the role of CFO on December 1, 2025, overseeing the company's transition into this high-activity exploration phase.

Latest SWOT Analysis

Source: Kalkine Group

Strengths

- Strategic Location: Sobek is situated in the Vicuña District, a premier global mining hotspot.

- Technical Expertise: Over 20 years of experience in the Andean region with a proven track record of target generation.

- Ownership Structure: 100% interest in the flagship Sobek project allows for full value capture upon discovery.

Weaknesses

- Capital Intensive: As a junior explorer, the company is reliant on equity markets for funding, leading to potential shareholder dilution.

- Cash Burn: Previous financial reports indicated a "FAIR" health score due to the high costs of self-funding deep-drill programs (InvestingPro Data, Dec 2025).

Opportunities

- Discovery Potential: A successful drill intercept at 46 South could lead to a massive re-rating of the stock.

- M&A Target: Major mining companies looking for copper-gold reserves in Chile often acquire juniors with successful discovery holes.

- Royalty Portfolio: The company’s retained royalties on sold projects provide long-term "free" upside.

Risks

- Exploration Risk: There is no guarantee that geophysical anomalies will translate into economic mineralization.

- Commodity Price Volatility: Fluctuations in copper and gold prices directly impact the company’s ability to raise capital.

- Geopolitical and Permitting: Operating in South America involves navigating evolving environmental regulations and community relations.

Outlook and Risks

The immediate outlook for Mirasol Resources is binary and tied to the assays from the maiden drill hole at Sobek. Over the next few months, the market will transition from speculating on "geophysical potential" to analyzing "drilling reality." If the 1,000-meter hole confirms the presence of a high-grade copper-gold porphyry system, Mirasol could transition from a project generator into a discovery-stage company.

However, the risks remain high. The current 31% surge has pushed the Relative Strength Index (RSI) into extremely overbought territory (RSI 88), suggesting a potential for short-term consolidation or a "sell-the-news" event if initial results are delayed. Furthermore, the company’s reliance on capital markets means that any broader market downturn could hinder its ability to fund subsequent drilling phases.

Conclusion

The 31.34% surge in Mirasol Resources on January 23, 2026, underscores a pivotal moment for the company as it moves from the theoretical realm of geophysics into the physical reality of drilling. By focusing its resources on the 46 South target within the world-class Vicuña District, Mirasol has captured the market's imagination. While the technical setup is as "compelling" as the company suggests, the ultimate validation rests in the core samples currently being pulled from the Chilean Andes. For now, Mirasol remains a high-octane story of strategic positioning and exploration audacity.

Please wait processing your request...

Please wait processing your request...