The uranium sector is glowing, and Denison Mines Corp. (TSX: DML) is leading the charge. On December 19, 2025, the stock surged by approximately 7.3%, catching the attention of retail and institutional investors alike. This jump isn't just a random spike; it’s the result of a "perfect storm" of operational milestones and macro-economic tailwinds.

Key Drivers: Why the 7.3% Jump on Dec 19?

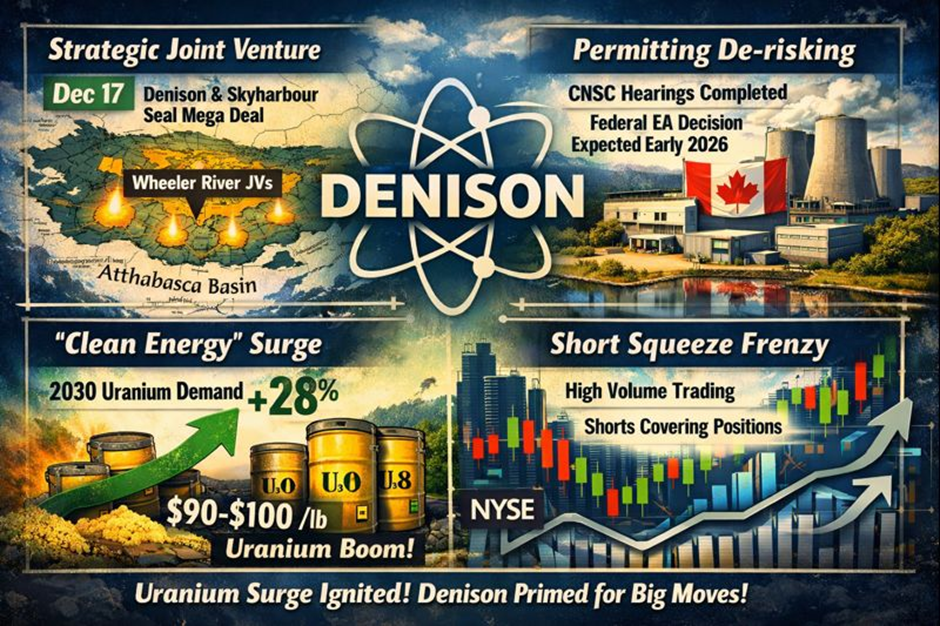

The mid-December rally was fueled by a combination of company-specific wins and a bullish uranium market:

Source: Kalkine Group

- Strategic Joint Venture Closing: On December 17, just 48 hours before the surge, Denison finalized a massive deal with Skyharbour Resources. This created four new JVs surrounding the flagship Wheeler River project, effectively expanding Denison’s dominance in the Athabasca Basin.

- Permitting De-risking: Reports circulated that the Canadian Nuclear Safety Commission (CNSC) public hearings for the Wheeler River Project concluded successfully in mid-December. Investors are betting on a positive Federal Environmental Assessment (EA) decision in early 2026.

- The "Clean Energy" Macro Tailwind: In late 2025, global uranium demand projections for 2030 were revised upward by 28%. With spot prices stabilizing in the $90–$100/lb range, Denison—as a low-cost producer in waiting—is a primary beneficiary of "uranium fever."

- Liquidity & Short Covering: High volume on the TSX and NYSE American (DNN) suggests that short-sellers may be exiting positions as the company nears a Final Investment Decision (FID) for its Phoenix deposit.

Latest Business Model: Transitioning to Producer

Denison is no longer just an "explorer." Its 2025 business model is built on three pillars:

- Flagship Development (Wheeler River): 95% interest in the largest undeveloped uranium project in the eastern Athabasca Basin.

- Low-Cost Innovation (ISR & SABRE): Using In-Situ Recovery (ISR) at the Phoenix deposit, which targets operating costs as low as US$16/lb. They are also using the SABRE (Surface Access Borehole Resource Extraction) method at McClean Lake.

- Toll Milling & Strategic Assets: 22.5% ownership in the McClean Lake Mill, one of the world's most technologically advanced uranium processing facilities, providing a recurring revenue stream through tolling for other miners.

2025 Financial & Operational Updates

- Cash King: As of Q3 2025, Denison reported a massive war chest of ~$720 million in cash, investments, and physical uranium holdings.

- Convertible Note Success: The company raised US$345 million via convertible notes in August 2025, ensuring it has the capital to move straight into construction once permits land.

- Engineering Milestones: Detailed engineering for the Phoenix project reached 85% completion by December 2025, with critical "Year 1" construction scopes at 100%.

- Production Proof: In July 2025, mining operations successfully commenced at the McClean North deposit using SABRE technology, yielding over 85,000 lbs of U₃O₈ in just the first quarter of operation at a cash cost of ~$19/lb.

SWOT Analysis

Source: Kalkine Group

Critical Risks

- Permitting Uncertainty: While the provincial EA is approved, the Federal (CNSC) license is the final hurdle. Any delay here would push the 2026 construction start.

- Technical Risk: ISR mining has never been done at this scale in the Athabasca Basin. While tests are positive, full-scale implementation carries operational risk.

- Market Volatility: Uranium is a "thin" market; price swings can be violent and decoupled from company fundamentals.

Conclusion

Denison Mines' 7.3% jump on December 19 reflects a market realizing that this company is no longer a speculative "if" but a high-probability "when." With nearly $720M in liquidity, engineering almost complete, and a massive expansion of its exploration footprint through the Skyharbour deal, Denison is positioned as the premier mid-tier uranium play for 2026.

Source: Trading View, 19 December 2025

Please wait processing your request...

Please wait processing your request...