The Nuclear Renaissance: Why Smart Money is Betting Big on Yellowcake

The global energy landscape in 2026 has reached a definitive turning point, with uranium evolving from a niche commodity into the "AI proxy" of choice for institutional portfolios. Investment giant like Bloomberg are increasingly highlighting a structural supply deficit that is no longer theoretical—it is here.

As data centres demand 24/7 carbon-free baseload power and major economies triple down on nuclear capacity to meet 2030 climate goals, "Smart Money" has identified the Toronto Stock Exchange (TSX) as the premier jurisdiction for securing supply. Fund managers are shifting away from speculative "penny plays" and consolidating positions in established producers and world-class developers that offer both scale and geological certainty.

Source: Kalkine Group

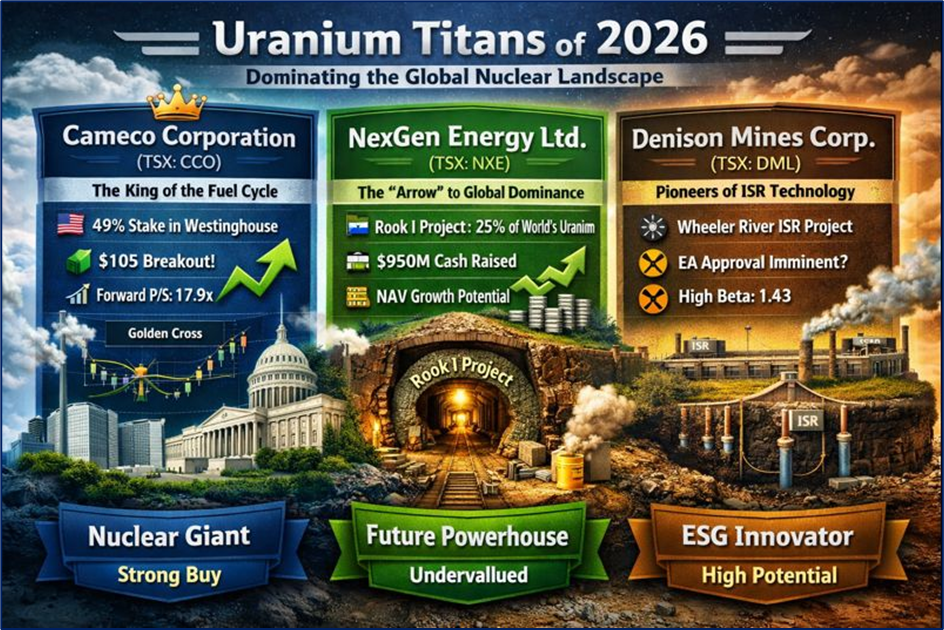

Cameco Corporation (TSX: CCO) – The Unrivaled Global King of the Fuel Cycle

Key Reasons and Market Drivers Cameco remains the "gold standard" for institutional exposure, operating as a vertically integrated powerhouse that spans mining, refining, and enrichment. The primary driver for 2026 is its strategic partnership with the U.S. government and its 49% stake in Westinghouse, which allows it to capture revenue not just from raw uranium, but from the entire lifecycle of nuclear technology. As term prices for uranium sustain levels above $85/lb, Cameco’s long-term contracting strategy is beginning to yield massive margin expansions.

Technical Analysis and Analyst Sentiment As of January 2026, CCO is exhibiting a strong "Golden Cross" on the daily charts, with its 50-day moving average trending decisively above the 200-day line. Recent technical breakouts above the $105 resistance level suggest a new bullish phase. Analysts from firms like Bernstein and Zacks currently maintain a "Buy" or "Strong Buy" consensus, with 2026 earnings projected to grow by 55% year-over-year. While the RSI indicates the stock is occasionally overbought, institutional "buy-the-dip" behavior at support levels around $92 remains highly consistent.

Financial and Operational Updates

- Business Model: Transitioned to a "full-service" nuclear energy provider, blending mining production with high-margin reactor services.

- Financials: Reported a narrowed 2025 delivery target of 32–34 million pounds, indicating a focus on "value over volume."

- Latest Dividend: Maintains a modest but reliable annual dividend of roughly $0.12 per share, though capital appreciation remains the primary draw.

- Valuation: Currently trading at a forward P/S ratio of approximately 17.9x; while historically high, analysts argue this reflects its unique monopoly-like status in the Western supply chain.

- Risks: Potential operational disruptions at McArthur River or further delays in the global rollout of Small Modular Reactors (SMRs).

NexGen Energy Ltd. (TSX: NXE) – The "Arrow" Aiming for Global Dominance

Key Reasons and Market Drivers NexGen Energy is the darling of the "smart money" crowd due to its flagship Rook I project in the Athabasca Basin. It is widely considered the highest-grade, lowest-cost undeveloped uranium project on the planet. The core driver in 2026 is the transition from a "pre-revenue" story to a "construction-phase" reality. With the Rook I project anticipated to produce nearly 25% of the world’s uranium at an industry-leading cash cost of roughly $13.86/lb (CAD), it is a prime target for a strategic takeover or massive long-term offtake agreements.

Technical Analysis and Analyst Sentiment NexGen has seen a significant surge in momentum, recently posting a 20% gain over a 7-day period. Analysts from Simply Wall St and various investment banks note that while the Price-to-Book (P/B) ratio of 10.7x looks expensive on paper, Discounted Cash Flow (DCF) models suggest the stock is heavily undervalued based on future production capacity. Twelve-month price targets average a significant premium over current levels as the market prepares for the final 2026 federal permitting decision from the Canadian Nuclear Safety Commission.

Financial and Operational Updates

- Business Model: Rapidly evolving from an exploration company to a major mining operator; focusing on advanced mine design and ESG-compliant infrastructure.

- Financials: Successfully raised approximately C$950 million in late 2025, extending their cash runway to nearly 5 years and de-risking the construction phase.

- Latest Dividend: None. All capital is currently being reinvested into the development of the Rook I project.

- Valuation: Market cap sits around C$9.85 billion. Valuation is heavily tied to the "Arrow" deposit’s massive Net Asset Value (NAV).

- Risks: Regulatory hurdles in the final permitting stage and the inherent volatility of pre-production mining stocks.

Denison Mines Corp. (TSX: DML) – The Pioneer of Low-Cost ISR Technology

Key Reasons and Market Drivers Denison Mines has captured the attention of brokers and funds through its innovative use of In-Situ Recovery (ISR) mining in the Athabasca Basin—a method typically used in Kazakhstan but revolutionary for Canadian high-grade deposits. Its flagship Wheeler River project is nearing a Final Investment Decision (FID) in the first half of 2026. Because ISR is significantly more environmentally friendly and cheaper than conventional mining, Denison is positioned as the high-margin "ESG play" of the sector.

Technical Analysis and Analyst Sentiment Options activity for DML has spiked in early 2026, signaling that institutional traders are hedging for a major volatility event—likely the upcoming federal EA (Environmental Assessment) approval. The stock currently trades with a high beta of 1.43, making it a favorite for aggressive growth portfolios. Analysts generally maintain a "Hold" or "Outperform" rating, waiting for the "green light" on construction to re-rate the stock toward the C$3.50+ range.

Financial and Operational Updates

- Business Model: Pure-play uranium developer with a focus on ISR technology and strategic stakes in existing mills (McClean Lake).

- Financials: Achieved 85% completion of total engineering for the Phoenix ISR mine; currently seeing first-ever production from the McClean North satellite deposit.

- Latest Dividend: None; focus remains on the $200M+ capital requirement for Wheeler River construction.

- Latest Valuation: Price-to-Book ratio sits near 10x, reflecting high investor confidence in its undeveloped resources.

- Risks: Technical risks associated with the first-ever application of ISR in the Athabasca Basin and sensitivity to short-term spot price fluctuations.

The Verdict: A Sector Primed for an Atomic Breakout

The consensus among fund managers for 2026 is clear: the "easy money" from the initial uranium price rebound has been made, and the next phase of the bull market belongs to companies that can actually deliver physical pounds. Cameco provides the safety and stability of a global leader, NexGen offers the explosive potential of a generational asset, and Denison represents the technological edge of the next mining cycle. While risks such as regulatory delays and commodity volatility remain, the structural demand from the AI-driven energy crisis makes these three TSX stocks the primary focal points for any serious energy-focused portfolio this year.

Please wait processing your request...

Please wait processing your request...