To generate $500 per week ($26,000 annually) in 2026, the amount of capital you need is fundamentally a function of the dividend yield you are willing to target. In the current Canadian market where the "Big Six" banks are trading at premium valuations and the Bank of Canada has paused rates at 2.25%—your strategy must balance high yield with capital preservation.

Here is the analytical breakdown of how to achieve this goal using the latest data from January 2026.

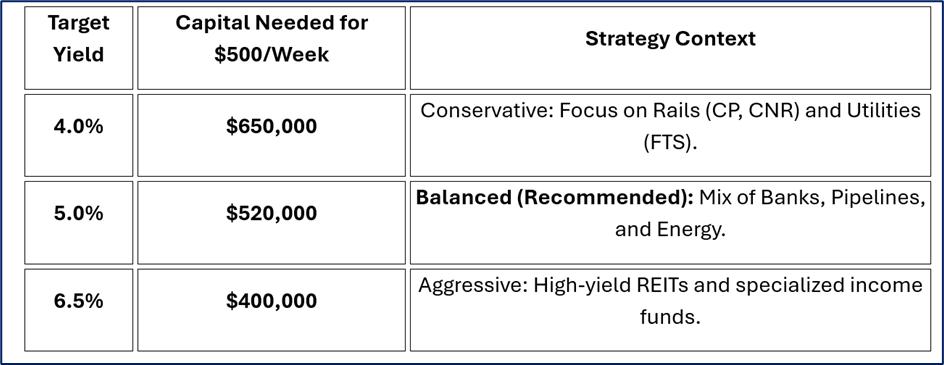

1. The Financial Requirement: Yield vs. Capital

The higher the yield you chase, the less money you need upfront—but the higher the risk of a dividend cut. Analysts from TD Securities and RBC Wealth Management currently suggest that a "quality-first" portfolio in 2026 should aim for a 4.5% to 5.5% yield.

Source: Kalkine Group Analysis

2. 2026 "Bay Street" Top Picks

Source: Kalkine Group

According to recent reports from Scotiabank and BMO, the 2026 landscape is defined by "trade-insulated" sectors. Here are the specific stocks to consider to build that $26,000/year income:

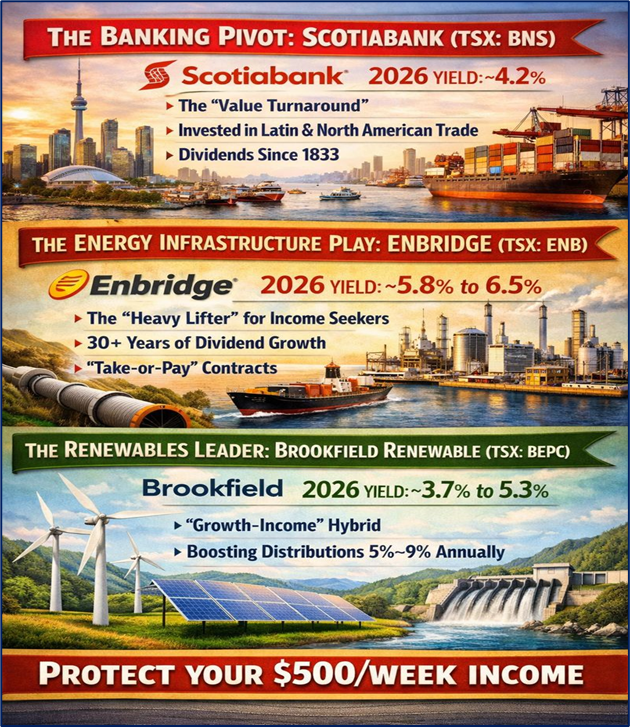

The Banking Pivot: Scotiabank (TSX: BNS)

- 2026 Yield: ~4.2%

- The Analyst View: While most Canadian banks are trading at high P/E multiples, Scotiabank is frequently cited by analysts as a "value turnaround." Its heavy investment in Latin American and North American trade corridors makes it a unique play as global trade recalibrates in 2026. It has paid dividends since 1833, making it a bedrock for weekly income.

The Energy Infrastructure Play: Enbridge (TSX: ENB)

- 2026 Yield: ~5.8% to 6.5%

- The Analyst View: Enbridge remains the "heavy lifter" for income seekers. With a 30-year track record of dividend increases, it provides the high yield necessary to keep your required capital closer to the $500k mark. Analysts at BMO Global Asset Management highlight its predictable cash flow from "take-or-pay" contracts, which are immune to daily oil price swings.

The Renewables Leader: Brookfield Renewable (TSX: BEPC)

- 2026 Yield: ~3.7% to 5.3% (depending on entry price)

- The Analyst View: As the federal government pushes for $1 trillion in new capital investment by 2030, Brookfield is a primary beneficiary. Analysts suggest that its plan to increase distributions by 5%–9% annually makes it a "growth-income" hybrid that protects your $500/week from being eroded by inflation.

3. Current Market Sentiment & Risks

The "Banker’s Opinion" for 2026 is currently split into two camps regarding interest rates, which directly affects dividend stocks:

- The "Rate Hike" Warning: Scotiabank Economics warns of a potential 50-basis-point hike in the second half of 2026 if inflation remains sticky above 2%. This could cause temporary price drops in "bond-proxy" stocks like utilities.

- The "Productivity" Argument: BMO expects a possible rate cut to 1.75% to stimulate Canada’s lagging productivity. If BMO is right, dividend-paying stocks will likely see a massive price surge as investors flee low-yielding bonds.

Conclusion: The "Wealth Effect" Strategy

Earning $500 weekly in 2026 is less about finding a "magic stock" and more about sector allocation. With the TSX 60 showing 3.23% YTD growth as of mid-January, the market is favoring established giants over speculative growth.

To secure your second income, aim for a $520,000 portfolio diversified across Financials, Energy Infrastructure, and Utilities. This provides a "safety buffer"—if one company pauses its dividend growth, the others (like CNQ or Enbridge, which are in "renaissance" modes) can carry the load. By utilizing your TFSA and RRSP to house these assets, you can ensure that the $500 arriving in your account every week is as tax-efficient as possible.

Please wait processing your request...

Please wait processing your request...