Key Takeaways

- The Spike: Curaleaf Holdings (TSX: CURA) experienced a significant stock surge, reportedly driven by renewed optimism surrounding S. federal cannabis reform, specifically reports of an impending executive order to loosen federal restrictions or support for marijuana rescheduling. These headlines often act as a major catalyst for U.S.-focused cannabis multi-state operators (MSOs) like Curaleaf.

- The Drivers: Market sentiment is overwhelmingly tied to regulatory advancements. Other recent drivers include strategic international expansion (strong growth in Europe), completion of key acquisitions (like Virginia assets), and inclusion in a major index (S&P/TSX Composite).

- The Caution: Despite positive sentiment, the company faces headwinds from domestic price compression, leading to recent overall revenue declines year-over-year. The company also carries a significant debt burden and remains largely unprofitable on a net income basis.

The Explosive Drivers: Decoding the Surge

The reported 38% single-day jump is a classic example of how regulatory headlines can trigger massive volatility in the cannabis sector. For a U.S. multi-state operator (MSO) like Curaleaf, any progress toward federal reform—such as rescheduling cannabis from Schedule I—is a game-changer.

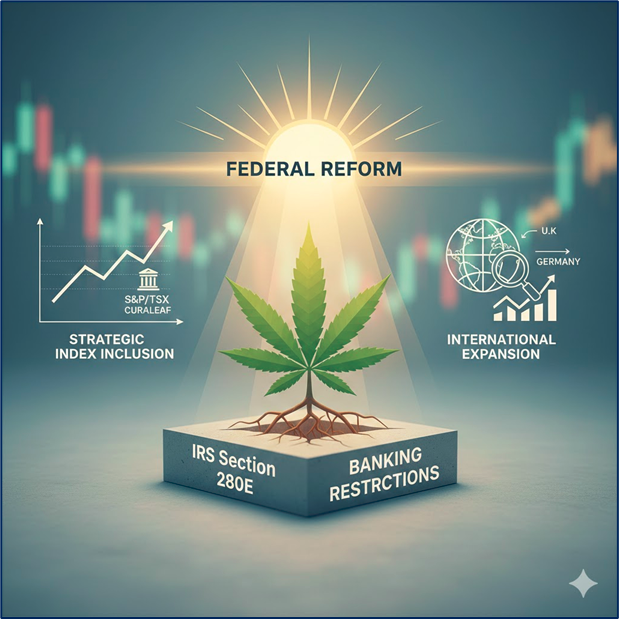

- Federal Reform Fever (The Primary Catalyst): The most recent and potent driver is the speculation around the U.S. government moving to relax federal restrictions on cannabis. Rescheduling or other forms of federal recognition could potentially:

- Alleviate the crippling tax burden of IRS Section 280E, which prohibits cannabis businesses from deducting standard business expenses. This alone could dramatically boost profitability across the sector.

- Improve access to institutional banking and capital markets, lowering the cost of doing business.

- Strategic Index Inclusion: Curaleaf was the first U.S.-headquartered cannabis company to be included in the S&P/TSX Composite Index. This is a powerful driver because it forces ETFs and index-tracking funds to purchase the stock, creating a new, automatic demand and significantly boosting liquidity and institutional visibility.

- International Expansion Success: While the U.S. domestic market has faced price compression, Curaleaf's International segment (primarily Europe, including the U.K. and Germany) has demonstrated strong growth, with international revenue increasing substantially year-over-year.

Source: Kalkine Group

Curaleaf's Business Model: Plant to Patient

Curaleaf operates as a leading vertically integrated multi-state operator (MSO) in the cannabis industry, meaning it controls the process from cultivation to manufacturing, and final retail sale.

- Vertical Integration: The company owns and operates cultivation sites, processing facilities, and a broad network of retail dispensaries (over 150 locations primarily in high-population U.S. states like Florida, New York, and Illinois). This model provides control over the supply chain, product quality, and cost of goods sold, creating economies of scale.

- Retail and Wholesale: Its revenue comes primarily from two channels:

- Retail: Sales through its own company-owned dispensaries.

- Wholesale: Supplying its branded products (like Select, Grassroots, and Curaleaf) to other licensed operators.

- Geographic Focus: The business is heavily skewed toward the Domestic U.S. market (around 85% of revenue), but its International business is the fastest-growing segment, focusing on medical cannabis markets in Europe.

Latest Business Updates: A Mixed Bag

While the stock price has surged on sentiment, recent financial results show a mixed operational picture:

- Q3 2025 Results: Net revenue of $320 million showed a sequential increase but a year-over-year decrease, highlighting the ongoing challenge of domestic price compression.

- Profitability: The company remains in a net loss position from continuing operations. However, it continues to post positive Adjusted EBITDA (around a 22% margin) and, notably, is a cash-generating rarity in the sector, reporting robust free cash flow.

- Strategic Moves: Recent news includes expanding its credit facility and an agreement to acquire Virginia assets from a competitor, consolidating its market position in key states. The company also announced plans to exit the hemp-derived THC market ahead of a potential federal ban, re-focusing on state-regulated cannabis.

The Risks: Why Volatility Remains King

The cannabis sector is inherently high-risk, and Curaleaf is no exception. Investors should be mindful of these key risks:

- Regulatory Dependency: The stock's valuation is heavily tied to the hope of U.S. federal reform. If legislative or executive action is delayed or fails to materialize, the stock could face a sharp reversal.

- Domestic Price Compression: Intense competition and market maturation in key states are driving down prices, which puts ongoing pressure on the company's gross margins and overall revenue growth.

- Debt Load: Curaleaf has a substantial debt pile (over $500 million), with a notable maturity looming in December 2026. While cash flow is positive, debt management remains a critical concern.

- Valuation: Despite operational headwinds, the stock's recent surges have left its price-to-sales (P/S) ratio looking high compared to many of its Canadian-listed peers, suggesting that positive sentiment may have outpaced fundamental improvements.

Conclusion: A Ride on Regulatory Waves

Curaleaf's stock rocketing upwards is a powerful reminder that in the cannabis sector, sentiment and regulatory catalysts often overshadow current financials. The surge reflects investor enthusiasm for potential U.S. federal reform and the company's market leadership and international growth. However, until federal policy provides a tangible reduction in the 280E tax burden and stabilizes domestic pricing, the stock will likely remain a high-beta, volatile vehicle that rewards regulatory hope while battling real operational challenges.

Source: Trading View, 12 December 2025

Please wait processing your request...

Please wait processing your request...