In a volatile global market environment, investors are searching for defensive dividend stocks, infrastructure plays, and high-quality industrial compounders. Toromont Industries has quickly emerged as a leading candidate in February 2026 after its shares surged 6.2% on 11 February, outperforming the broader Canadian market.

With resilient equipment rental demand, strong infrastructure spending, and mining capital expenditure recovery supporting fundamentals, Toromont appears positioned as a defensive-growth hybrid within the Canadian industrial sector.

Toromont’s recent rally came alongside renewed momentum in the S&P/TSX Composite Index, yet it significantly outpaced broader index gains.

Key February 2026 Highlights:

- Shares surged approximately 6.2% on 11 February 2026

- Outperformed the TSX Composite and several industrial peers

- Supported by strong Q4 2025 earnings results

- Benefiting from improving Canadian macroeconomic sentiment

- Reinforced dividend sustainability and free cash flow strength

This move placed Toromont at the center of searches for:

- Best TSX dividend stocks 2026

- Canada infrastructure stocks

- Industrial equipment leaders TSX

- Recession-resistant Canadian equities

Is Canada’s Economic Stabilization Driving the Rally?

Canada’s macro backdrop in early 2026 shows improving stability:

- Inflation moderating from prior peaks

- Interest rates expected to plateau before gradual easing

- Federal infrastructure commitments progressing

- Mining and resource capital expenditure strengthening

- Housing construction stabilizing

A relatively stable Canadian dollar (CAD) supports equipment import cost predictability while reinforcing mining sector activity — both constructive for Toromont’s earnings outlook.

Investors are increasingly rotating toward cash-generative industrial leaders as portfolio hedges against commodity and financial sector volatility.

A Diversified Industrial Model With Defensive Characteristics

Toromont operates through two core segments:

1️⃣ Equipment Group

Exclusive dealership territories for Caterpillar Inc. across large Canadian regions.

2️⃣ CIMCO

Industrial and recreational refrigeration systems supporting cold chain logistics and food infrastructure.

Why This Matters

- High-margin recurring parts & service revenue

- Long-term maintenance contracts

- Strong mining and infrastructure client relationships

- Asset-light distribution model

- Conservative leverage and disciplined capital allocation

Unlike pure construction cycle stocks, Toromont benefits from aftermarket services, which smooth earnings across economic cycles.

What Specifically Triggered the 6.2% Surge?

Several catalysts converged:

- Strong Q4 2025 earnings performance

- Order backlog strength across equipment categories

- Mining demand linked to copper, gold, and base metal capex

- Infrastructure execution visibility

- Dividend reaffirmation and stable payout ratio

- Positive analyst upgrades post-results

The earnings commentary suggested 2026 may exceed prior consensus expectations, prompting momentum inflows.

Dividend Growth Profile Remains Intact

Toromont continues to appeal to dividend-focused investors.

Dividend Strengths:

- Sustainable payout ratio

- Strong operating cash flow generation

- Moderate capital expenditure needs

- Low net debt profile

- Long-term history of dividend increases

Future dividend growth is expected to track earnings expansion rather than aggressive payout changes — a hallmark of quality compounders.

Analyst Outlook – February 2026

Leading Canadian brokerages remain broadly constructive:

- RBC Capital Markets – Outperform – CAD target mid-$130s

- TD Securities – Buy – CAD target low-$140s

- BMO Capital Markets – Market Perform – CAD target mid-$120s

- Scotiabank – Sector Outperform – CAD target upper-$130s

- National Bank Financial – Outperform – CAD target low-$140s

Consensus suggests moderate upside rather than speculative re-rating, reinforcing the thesis of steady compounding.

Short, Medium & Long-Term Outlook

Short Term (3–6 Months)

- Technical breakout following earnings

- Industrial sector rotation

- Improving TSX momentum

Bias: Cautiously bullish

Medium Term (6–18 Months)

- Dependent on Canadian macro resilience

- Mining capital expenditure cycle strength

- Infrastructure budget execution

Bias: Neutral-to-constructive

Long Term (3–5 Years)

- Structural infrastructure demand

- Energy transition project exposure

- Cold chain logistics growth

- Recurring service revenue compounding

Bias: Structurally positive

Key Risks to Monitor

- Canadian economic slowdown

- Sharp commodity price correction

- Infrastructure spending delays

- Equipment inventory normalization

- CAD volatility

- Competitive pricing pressure

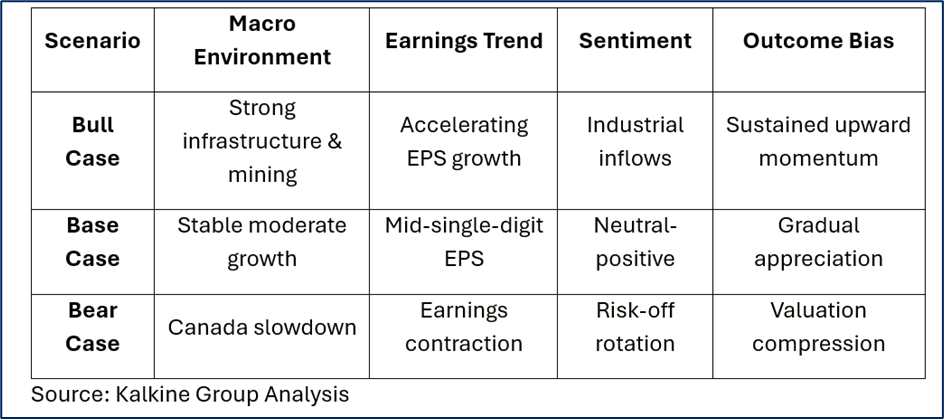

Bull vs Bear Scenario Matrix

Why Toromont May Be Recession-Resistant

Toromont’s combination of:

- Infrastructure-linked revenue

- Mining exposure

- High recurring service income

- Conservative balance sheet

- Dividend growth discipline

Positions it as a defensive industrial compounder rather than a purely cyclical machinery stock.

As investors rotate toward quality, free-cash-flow generative companies in 2026, Toromont stands out within the Canadian industrial landscape.

Final Investment Perspective – February 2026

Toromont Industries represents a high-quality TSX-listed industrial leader with diversified exposure to infrastructure, mining, and refrigeration markets.

The recent 6.2% surge reflects:

- Earnings resilience

- Strengthening macro sentiment

- Industrial sector rotation

- Institutional confidence

Short-term momentum appears constructive. Medium-term performance depends on Canada’s economic trajectory and mining capex trends. Long-term structural drivers remain favorable due to recurring service revenue and disciplined capital allocation.

For investors seeking TSX dividend growth stocks, Canadian infrastructure plays, and recession-resistant industrial equities in 2026, Toromont Industries remains firmly on the radar.

Frequently Asked Questions

Why did Toromont Industries rise 6.2% in February 2026?

Strong Q4 earnings, backlog visibility, mining demand recovery, and positive analyst sentiment.

Is Toromont a dividend growth stock?

Yes. It maintains a progressive dividend supported by stable free cash flow.

Is the stock bullish in 2026?

Short-term momentum is positive; longer-term performance depends on macro and capital expenditure cycles.

What sector does Toromont operate in?

Industrial equipment distribution and refrigeration systems within the Canadian industrial sector.

Please wait processing your request...

Please wait processing your request...