Loblaw Companies has shown resilience amid inflation and shifting consumer demand. Could this TSX grocery giant continue delivering stable returns in 2026?

Key Takeaways – February 2026 Market Update

- Loblaw Companies Limited shares advanced approximately 2.5% on 12 February 2026, outperforming segments of the S&P/TSX Composite Index

- Capital rotated into defensive consumer staples stocks amid global volatility and Bank of Canada rate-cut expectations

- Strong food same-store sales and pharmacy momentum supported earnings visibility (Company release, Q4 2025, January 2026)

- Private-label growth led by President’s Choice and No Name continues to support margin stability

- Dividend growth and resilient free cash flow reinforce long-term defensive positioning

Source: Kalkine Group

Why Is Loblaw Stock Trending in February 2026?

As of February 2026, search trends for “best TSX dividend stocks 2026,” “top Canadian defensive stocks,” “recession-proof grocery stocks,” and “consumer staples outperforming TSX” are accelerating globally. Loblaw Companies Limited is emerging as a high-search-volume stock amid renewed investor focus on stability, predictable earnings, and dividend growth.

With global equity markets experiencing volatility due to fluctuating bond yields, geopolitical risk, and mixed economic data from the U.S., Europe, and Asia, investors are strategically reallocating toward essential-service companies. Defensive stocks with pricing power, inflation resilience, and stable cash flow are regaining leadership — and Loblaw fits squarely into that theme.

Loblaw’s 2.5% move reflects both sector rotation and company-specific strength.

How Are Global Markets, the Canadian Economy, and the CAD Influencing Loblaw’s Momentum?

Global Market Dynamics

Global markets remain cautious as central banks balance inflation control with economic growth stabilization. Rate-cut speculation in North America is driving renewed interest in yield-generating equities.

Canadian Economic Backdrop

- Moderate GDP growth trajectory

- Cooling but persistent food inflation

- Consumer spending prioritizing essentials over discretionary items

- Stable employment levels supporting grocery demand

Canadian Dollar (CAD) Analysis

The CAD remains range-bound amid commodity price volatility. A stable currency environment benefits large domestic retailers with predictable sourcing structures.

TSX Composite Outlook

The TSX shows sector divergence. Energy and materials remain cyclical, while consumer staples and utilities demonstrate defensive strength. Loblaw’s outperformance aligns with this defensive capital rotation.

How Strong Is Loblaw’s Core Business Model in 2026?

Loblaw operates a diversified and vertically integrated retail model built around:

- National grocery brands including Loblaws, Real Canadian Superstore, and No Frills

- Pharmacy and healthcare exposure through Shoppers Drug Mart

- High-margin private-label brands including President’s Choice and No Name

Structural Advantages:

- Non-discretionary demand profile

- National supply chain scale

- Private-label margin enhancement

- Data-driven loyalty ecosystem

- Omnichannel grocery and pharmacy integration

Private-label penetration continues to grow as consumers seek value in a higher-cost environment. This supports margin defense even as promotional intensity fluctuates.

What Did the Latest Financial and Operational Updates Reveal?

According to the company’s Q4 2025 earnings release (January 2026):

- Revenue growth remained stable year-over-year

- Comparable food retail sales posted positive gains

- Pharmacy and healthcare segments delivered steady expansion

- Adjusted EPS growth supported dividend sustainability

- Strong operating cash flow funded dividends and share buybacks

Capital Allocation Priorities:

- Sustainable dividend increases

- Balance sheet discipline

- Store modernization and digital investments

Dividend growth remains aligned with earnings trajectory, reinforcing Loblaw’s defensive income appeal.

How Does Loblaw Compare With Canadian Grocery Peers?

Peer Benchmarking Against:

- Metro Inc.

- Empire Company Limited

Competitive Positioning:

- Largest national footprint among peers

- Diversified grocery and pharmacy model

- Strong private-label ecosystem

- Comparable dividend growth consistency

- Defensive valuation relative to earnings stability

Loblaw’s integrated healthcare exposure through Shoppers Drug Mart differentiates it structurally from grocery-only competitors.

What Is the Short-Term, Medium-Term, and Long-Term Outlook?

Short-Term Outlook (3–6 Months)

Bullish Catalysts:

- Continued defensive rotation

- Potential Bank of Canada rate cuts

- Stable quarterly earnings

- Dividend-focused investor demand

Risks:

- Promotional competition

- Regulatory scrutiny in food pricing

Short-term tone: Moderately bullish.

Medium-Term Outlook (6–18 Months)

- Gradual normalization of food inflation

- Margin protection via private-label growth

- Pharmacy expansion and healthcare demand

Medium-term tone: Neutral to constructive.

Long-Term Outlook (3–5 Years)

- Structural grocery demand stability

- Aging demographic supporting pharmacy growth

- Digital retail expansion

- Dividend compounding

Long-term tone: Structurally bullish.

Is Loblaw Stock Bullish, Bearish, or Neutral in February 2026?

Short-Term Bias: Mildly bullish due to defensive flows and stable earnings.

Medium-Term Bias: Balanced with modest upside potential.

Long-Term Bias: Bullish based on durable fundamentals and recurring demand.

The absence of cyclicality combined with pricing power strengthens its defensive profile.

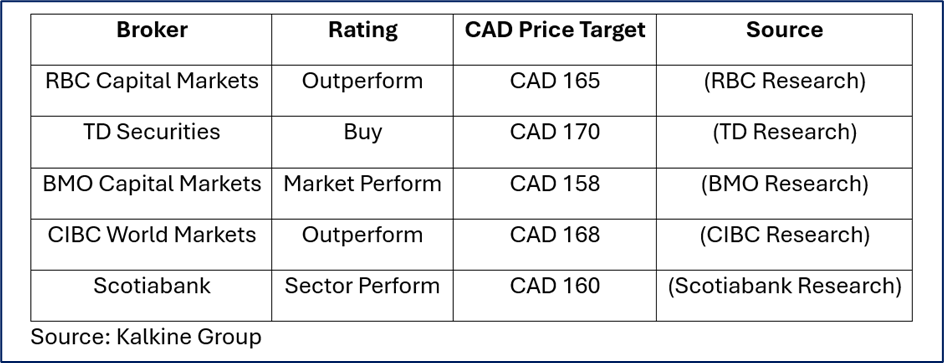

What Are Analysts Saying About Loblaw Stock in February 2026?

Latest consensus from major Canadian brokerages:

Consensus tone remains constructive with moderate upside implied based on earnings resilience.

What Does the Bull vs Bear Scenario Matrix Reveal?

What Key Risks Should Investors Monitor in 2026?

- Government intervention in grocery pricing

- Margin pressure from aggressive discounting

- Supply chain volatility

- Pharmacy reimbursement policy changes

- Consumer demand elasticity shifts

What Strategic Approaches Could Investors Consider Across Time Horizons?

Short-Term Focus

- Monitor Q1 2026 earnings momentum

- Track interest rate policy developments

- Observe same-store sales trends

Medium-Term Focus

- Evaluate private-label expansion impact

- Assess healthcare segment growth

Long-Term Focus

- Consider dividend compounding potential

- Monitor capital allocation discipline

- Evaluate structural grocery demand stability

Could Loblaw Be a Core Defensive Compounder in 2026 and Beyond?

Loblaw Companies Limited represents a high-quality Canadian consumer staples leader positioned at the intersection of grocery essentials, healthcare services, private-label brand strength, and dividend growth stability.

The 2.5% gain on 12 February 2026 reflects both macro defensive rotation and fundamental earnings durability. In an environment characterized by global volatility, moderated inflation, and evolving monetary policy, Loblaw stands as a structurally resilient TSX blue-chip.

While short-term fluctuations are possible, long-term fundamentals remain intact and aligned with defensive portfolio construction themes.

This content is for informational and educational purposes only and does not constitute financial advice.

Please wait processing your request...

Please wait processing your request...