Summary

- TFSAs offer tax-free growth and withdrawals; RRSPs offer a Tax deduction and tax-deferred growth.

- The 2026 TFSA limit is $7,000; the RRSP limit is $33,810 (or 18% of prior-year Earned income).

- RRSPs tend to win when contributions are made in high-tax-bracket years and withdrawals in lower-bracket years.

- TFSAs tend to win when current and future tax brackets are similar or for lower-income earners.

- Most Canadians benefit from using both.

What readers need to know

There is no universal 'better' account. The right answer depends on income, Tax Bracket, time horizon and personal goals.

Both accounts can be self-directed and hold most listed securities.

Introduction

Few personal-finance debates are as enduring as TFSA vs RRSP. Both are powerful tax-advantaged accounts. Both are widely available. Both can be self-directed. And both have different strengths depending on who is using them.

This article steps through the comparison without taking sides.

How they work

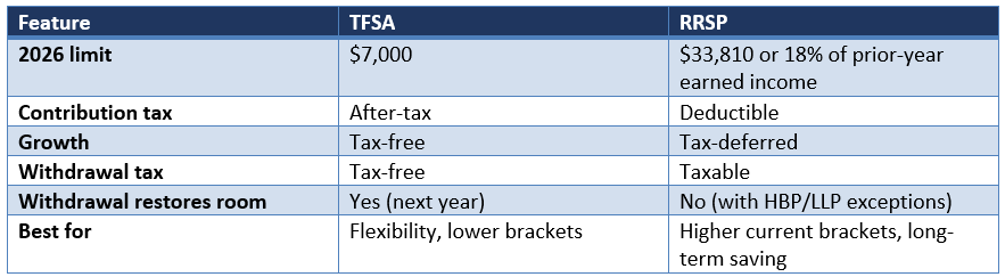

RRSPs: contributions deductible from income, tax-deferred growth, taxable on Withdrawal.

TFSAs: contributions from after-tax dollars, tax-free growth, tax-free on withdrawal. Withdrawals create new room the following calendar year.

Tax bracket dynamics

RRSPs work best when the contribution is deducted from high-bracket income and the withdrawal happens in a lower bracket later.

TFSAs work best when current and future tax rates are similar, or when after-tax dollars are easier to spare.

Younger Canadians with rising incomes may prefer TFSAs initially and RRSPs later as income grows.

Contribution limits

The 2026 TFSA limit is $7,000 plus any unused room. The RRSP limit is the lesser of 18 per cent of 2025 earned income or $33,810, plus unused room.

RRSP room scales with income; TFSA room does not.

Withdrawal flexibility

TFSA withdrawals are flexible and tax-free; the amount withdrawn restores room the next year.

RRSP withdrawals are taxable and reduce room (except under Home Buyers' Plan or Lifelong Learning Plan rules).

Which account first?

Lower-income Canadians often prefer TFSAs first. Higher-income Canadians may prefer RRSPs for the larger deduction. Most benefit from using both — the optimal split depends on individual circumstances.

TFSA vs RRSP (2026)

Key takeaways

- Both TFSAs and RRSPs have a role in Canadian Retirement Planning.

- TFSAs are flexible and tax-free; RRSPs are deduction-driven and tax-deferred.

- Tax bracket dynamics drive much of the choice.

- Most Canadians benefit from using both.

- Get professional advice for personalised planning.

Please wait processing your request...

Please wait processing your request...