The year 2026 opens with an economic anomaly: large deficits + moderating inflation + rate cuts—a post-cyclical cocktail supercharging asset prices outside of a recession. This is the new policy nexus where monetary easing meets unprecedented fiscal firepower.

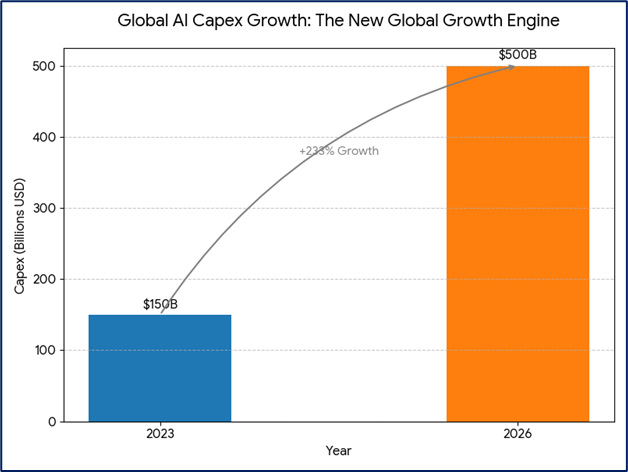

- AI is the New GDP Driver: Corporate AI capital expenditure is projected to exceed $500 Billion in 2026 (up from ~$150B in 2023). This represents a historic shift, driving more US GDP growth than households—a phenomenon experts compare to the biggest productivity shock since the Internet.

- Structural Inflation: Inflation is no longer cyclical; it’s structural. This is powered by: 1) massive AI energy demand, 2) commodity scarcity, and 3) supply chain reconstruction driven by geopolitics.

- The Fragmentation Dividend: Global fragmentation and industrial nationalism are creating multi-year, government-backed investment booms in defense, energy grids, robotics, and reshoring. These spending cycles are sticky and durable.

- Risks & Guardrails: The main risks include policy misalignment (too many Fed cuts priced in), valuation stretch in concentrated sectors, and global government debt surpassing $100T, maintaining bond-market volatility.

Source: Kalkine Group

The New Macro Engine: AI's $500B Power Surge & The Age of "Controlled Disorder"

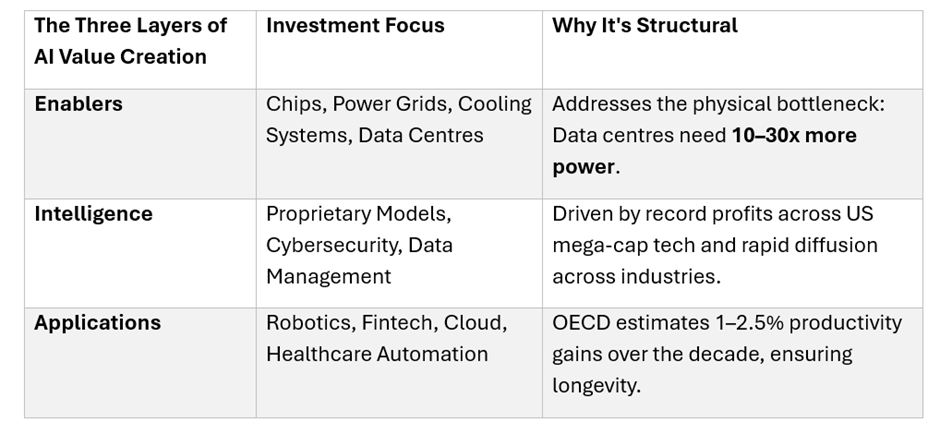

I. The AI Super-Cycle: From Software to Physical Infrastructure

Mega-cap US tech firms are entering a hyper-investment cycle, but the value creation is broadening far beyond the "Intelligence" layer.

Source: Kalkine Group

The Physical Bottleneck: Energy, Metals & Infrastructure

The AI race has triggered a scramble for physical resources. Utilities, Industrials, Energy Services, and Grid Infrastructure evolve from defensive "plodders" into high-growth sectors to support the data centre boom.

- Commodity Scarcity: Copper, lithium, uranium, and rare metals remain in structural deficit, making commodities a core inflation hedge.

- Asia Takes the Lead: BNP Paribas and UBS point to Asia (Taiwan, Korea, Japan, China) as the global tech powerhouse—dominating the semiconductor hub, robotics manufacturing, and critical metals processing.

II. Canada's Strategic 2026 Edge: The Scarcity Play

Despite the broader "controlled disorder" in global markets, the Canadian S&P/TSX Composite Index is forecast to hit new highs in 2026, supported by resource strength and expected interest rate cuts from the Bank of Canada. Canada is uniquely positioned to capitalize on the physical AI and fragmentation themes.

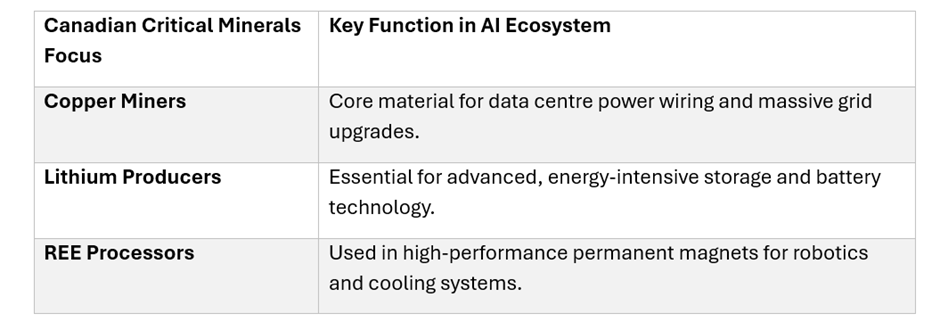

1. Critical Minerals & The Reshoring Trade

Global strategic autonomy requires secure, non-hostile sources for essential inputs. Canada's vast reserves of metals crucial for AI and the energy transition are its major structural advantage.

- Thesis: Canada is focusing on securing supply chains for EVs, defense, and data infrastructure. This is supported by government initiatives, including securing massive foreign investment (e.g., UAE).

- Why Canadian Stocks Win: They benefit from sustained, high demand for Copper (grid expansion, data centers), Nickel (batteries, defense), and Lithium/REEs (AI hardware, high-density batteries).

Source: Kalkine Group

Illustrative Names: Companies involved in exploration, processing, and high-growth production (e.g., Sigma Lithium, Li-FT Power, and mid-cap miners focused on strategic industrial metals).

- Utilities & The AI Power Surge

The massive, sudden electricity demand from new AI data centres is transforming Canadian utilities. Provinces with access to cheap, clean power (hydro) are attracting hyperscalers.

- Rationale: Canadian Utilities are becoming high-growth infrastructure plays. They are the toll booths for the AI Super-Cycle, profiting from multi-year projects to upgrade grids, deliver firm capacity, and integrate smart systems.

- The Power Factor: The IEA projects global data center consumption will double by 2026. Canada’s utilities are racing to integrate this unpredictable, but lucrative, demand.

Illustrative Names: Leading Canadian Utilities and Independent Power Producers (IPPs) with strong, secured pipelines for power generation and grid reinforcement (e.g., Hydro-Quebec partners, ATCO, or firms involved in AI-enabled grid optimization).

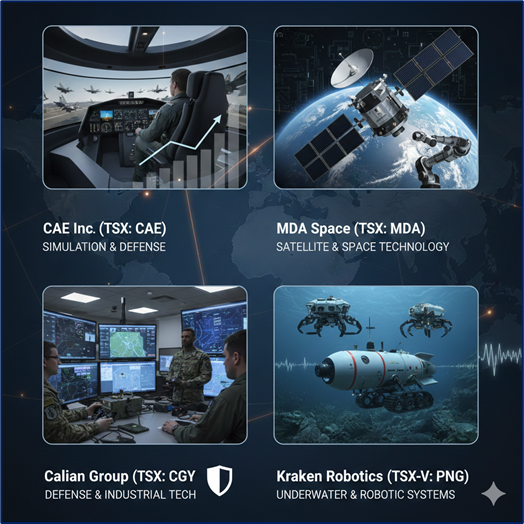

- Industrial Technology & Defense Backlogs

Geopolitical tensions translate directly into higher, non-cyclical defense and technology spending, supported by Canada's commitment to boost its NATO spending.

- Rationale: Firms with large defense backlogs and expertise in specialized, high-tech systems (space, simulation, subsea robotics) are set for durable earnings growth.

- Key Growth Drivers: Subsea Robotics (for defense/monitoring), Flight Simulation (for new military aircraft fleets), and Cybersecurity/Consulting (for government transformation).

Illustrative Names:

- CAE Inc. (TSX: CAE): Leader in simulation with an extensive defense backlog, benefiting from global fleet modernization.

- MDA Space (TSX: MDA): Positioned for growth in government and commercial satellite/space technology, a key element of strategic security.

- Calian Group (TSX: CGY) / Kraken Robotics (TSX-V: PNG): Specialized defense and industrial tech plays with growing government and military revenue.

Source: Kalkine Group

III. Global Equity Architecture & Portfolio Resilience

The US & Global Leadership

- US Exceptionalism: S&P 500 targets for 2026 converge at 7,400 – 7,800, driven by required 13–15% AI-led earnings growth.

- The Must-Broaden Rally: Consensus warns that mega-cap concentration risk is too high. Rotation themes for 2026 include:

- Financials (valuation reset, post-rate-cut resilience).

- Industrials & Utilities (AI power demand, fragmentation spending).

- Small & Mid-Caps (benefiting from rate cuts and broadening economic cycle).

- Asia = High-Conviction: Asia tech remains the structural winner across all institutional reports, driven by semiconductor dominance, governance reforms (Japan/Korea), and regional stimulus.

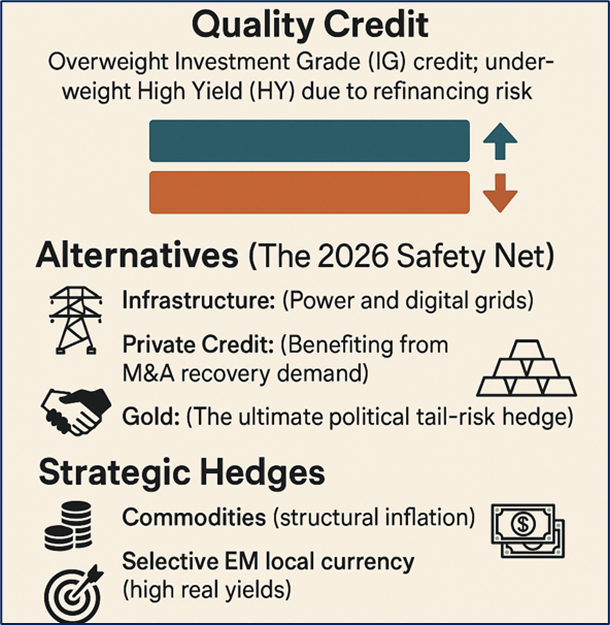

Portfolio Resilience: Quality is King

In a regime of structural inflation and volatility, traditional bond diversification fails. Strategic hedges and quality are paramount.

- Quality Credit: Overweight Investment Grade (IG) credit; under-weight High Yield (HY) due to refinancing risk.

- Alternatives (The 2026 Safety Net):

- Infrastructure: (Power and digital grids).

- Private Credit: (Benefiting from M&A recovery demand).

- Gold: (The ultimate political tail-risk hedge).

- Strategic Hedges: Commodities (structural inflation), selective EM local currency (high real yields), and tail-risk optionality around policy or geopolitical events.

Source: Kalkine Group

Conclusion: The Year of Complex Opportunity

2026 is defined by a triple paradox that requires active, disciplined investing:

- AI accelerates productivity but demands massive physical infrastructure.

- Fiscal expansion fuels growth but embeds structural inflation and debt risk.

- Geopolitical fragmentation creates volatility but unlocks multi-year spending cycles.

The winning strategy is to Own the AI infrastructure layer, rotate into Asia tech and Canadian industrials/resources, and use quality credit and alternatives for downside protection. Lean into the market dispersion - the world may be breaking apart, but the investment opportunities are multiplying.

Please wait processing your request...

Please wait processing your request...