Top 3 TSX Energy Multi-Bagger Stocks for 2026 - Wealth Compounding

Global fund managers and "smart money" are increasingly rotating capital into Canadian energy for 2026, driven by a dual thesis: energy security (oil/gas) and the energy transition (nuclear). While the broader market chases tech, sophisticated capital is positioning in high-margin, cash-flowing Canadian producers that are trading at deep discounts to their intrinsic value.

Below is the deep-dive research on three high-conviction picks that cover three distinct strategies: The Uranium Explosion (Growth), The Royalty Compounder (Income + Growth), and The Deep Value Turnaround (Aggressive Value).

Source: Kalkine Group

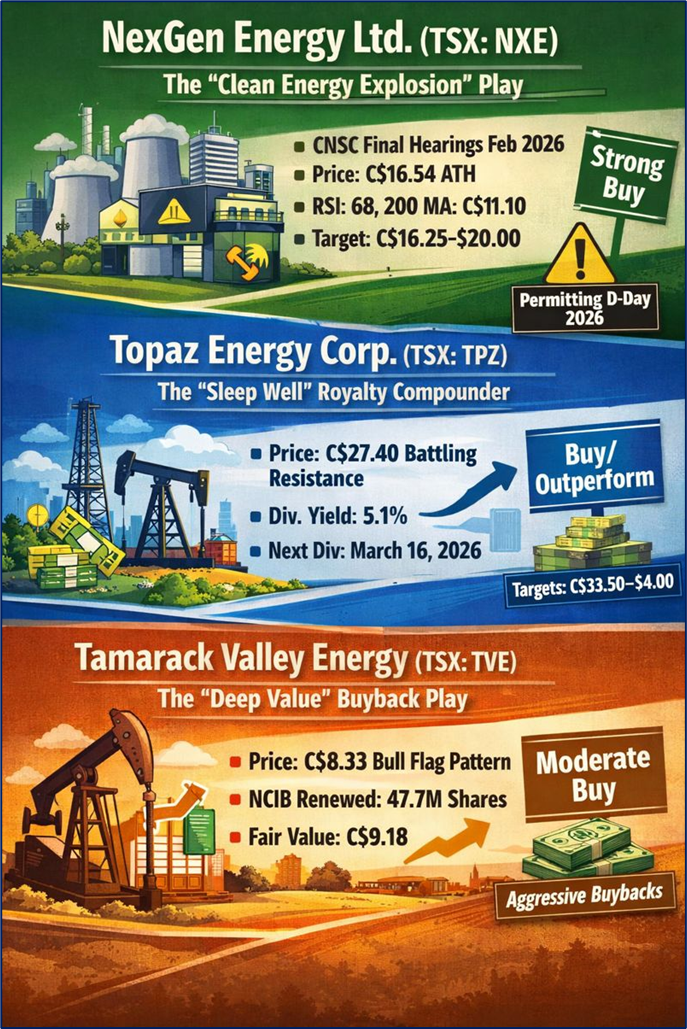

1. NexGen Energy Ltd. (TSX: NXE)

The "Clean Energy Explosion" Play

- Key Drivers: NexGen remains the premier global uranium play. The "Big Tech" pivot to nuclear for AI data centres has accelerated, with 2026 serving as the "Permitting D-Day." The Rook I project is now in the final stages of the CNSC (Canadian Nuclear Safety Commission) hearing process, with Part 2 of the public hearings scheduled for February 9–13, 2026, in Saskatoon.

- Current Technical Analysis: Price: Trading near C$16.54, testing new all-time highs.

- Indicators: The stock recently broke out from a consolidation zone ($14.00–$15.50). While the RSI is high (~68), it has not yet reached the "exhaustion" levels seen in previous runs. The 200-day Moving Average (C$11.10) continues to act as the primary long-term trend floor.

- Analyst Consensus: Strong Buy. BMO Capital Markets has lead the charge, recently raising their target to C$16.25–$20.00 as the project derisks.

- Outlook & Risks: The outlook is binary: final federal approval in early 2026 would trigger a massive re-rating. Risk: Any delay in the CNSC's final decision following the February hearings could cause a sharp "wait-and-see" pullback.

2. Topaz Energy Corp. (TSX: TPZ)

The "Sleep Well" Royalty Compounder

- Key Drivers: Topaz continues to dominate the royalty space by capturing high-margin revenue from the Montney and Clearwater plays. Its "toll-booth" business model is benefiting from increased production volumes by its main counterparty, Tourmaline Oil.

- Current Technical Analysis:

- Price: Stabilizing near C$27.40.

- Indicators: After a dip in early January, the stock issued a pivot bottom buy signal on Jan 7, 2026. It is currently battling resistance at the 50-day SMA (C$27.17) and the 200-day SMA (C$27.57). A clean break above $27.60 confirms the resumption of the primary uptrend.

- Dividend Update: Current yield sits at 5.1%. The next quarterly dividend of C$0.34 is confirmed with an ex-date of March 16, 2026.

- Analyst Consensus: Buy/Outperform. National Bank and Raymond James maintain targets in the C$33.50 to C$34.00 range, citing ~15%–24% upside from current levels.

- Outlook & Risks: The "South Montney" infrastructure expansion is the 2026 growth engine. Risk: Elevated payout ratios remain a point of discussion, though royalty cash flows typically support these levels.

3. Tamarack Valley Energy (TSX: TVE)

The "Deep Value" Aggressive Buyback Play

- Key Drivers: Tamarack is currently the "poster child" for capital returns in the Canadian mid-cap space. Having met debt targets in late 2025, the company is now a pure shareholder-return vehicle.

- Current Technical Analysis:

- Price: Surged to C$8.33, hovering near its 52-week high of C$8.49.

- Indicators: The stock has seen a massive "catch-up" trade, jumping nearly 60% over the last year. It is currently showing a "bull flag" pattern on the daily chart, supported by the January 19 renewal of its NCIB.

- The "Cannibalization" Update: As of today (Jan 19, 2026), the TSX has officially approved Tamarack’s renewed Normal Course Issuer Bid (NCIB). They are authorized to buy back up to 47.7 million shares (approx. 10% of the public float) over the next 12 months.

- Analyst Consensus: Moderate Buy. BMO and RBC recently boosted targets to C$9.00–$11.00, noting the significant valuation gap versus the company's C$9.18 "fair value" estimates.

- Outlook & Risks: Tamarack is transitioning from a "growth" company to a "yield and buyback" powerhouse. Risk: High sensitivity to the WTI/WCS differential; any pipeline constraints in 2026 could squeeze the free cash flow used for these buybacks.

Conclusion

For wealth compounding in 2026, these three offer a diversified basket: NexGen for the potential 5x-10x "home run" on the nuclear thesis, Topaz for the steady "double" via dividends and capital appreciation, and Tamarack Valley for a value-driven re-rating as they buy back their own float.

Please wait processing your request...

Please wait processing your request...