Aris Mining (TSX: ARIS) kicked off the first week of 2026 with a notable ~4% gain on January 5, continuing a multi-year momentum streak that has seen the stock significantly outperform its mid-tier gold peers.

As of early 2026, the company has transitioned from a "buy-and-build" story into a high-execution production powerhouse.

The Catalyst: Why ARIS Jumped on Jan 5, 2026

Source: Kalkine Group

The upward move on January 5 is driven by a "perfect storm" of macro-tailwinds and micro-execution:

- Gold Price Support: Entering 2026, gold continues to hold strength as central banks pivot toward bullion over Treasuries, providing a high floor for Aris’s realized prices.

- Production Ramp-Up Confirmation: Investors are reacting to the successful ramp-up of the Segovia Mill Expansion (increasing capacity from 2,000 to 3,000 tpd), which is now contributing to record-level throughput.

- Anticipation of 2025 Full-Year Results: With the company tracking toward the high end of its 230,000–275,000 oz guidance for 2025, early-year positioning is favoring stocks with proven organic growth.

Latest Business Model: The "Partnership" Pivot

Aris Mining has refined a unique business model that differentiates it from traditional miners:

- Contract Mining Partner (CMP) Integration: Aris processes ore from local small-scale miners. This "formalization" strategy secures high-grade feed for their mills while reducing social and security risks in Colombia—a model now being studied as a global ESG benchmark.

- Asset Ownership Consolidation: In late 2025, Aris closed the acquisition of the remaining 49% of Soto Norte, giving them 100% control over their entire growth pipeline (Segovia, Marmato, Toroparu, and Soto Norte).

- Owner-Operator Efficiency: By shifting to owner-mining at Segovia and mechanized bulk mining at Marmato, the company is aggressively targeting lower AISC (All-In Sustaining Costs).

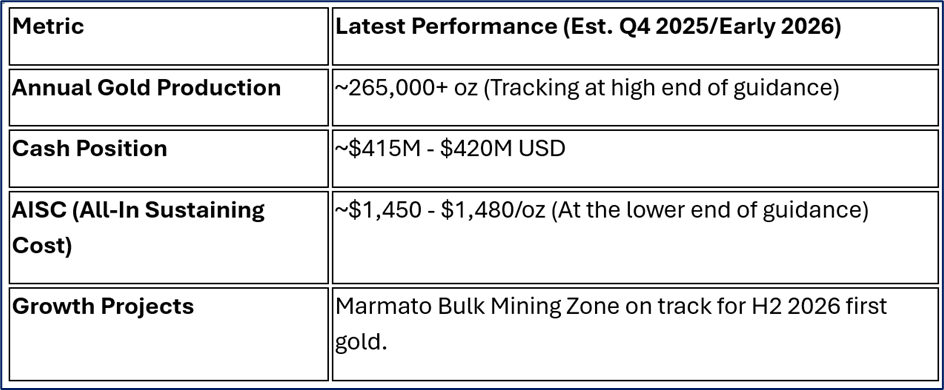

Financial and Operational Update (Q4 2025/Jan 2026)

Source: Company Data

Key Operations Focus:

- Segovia Operations: Now operating at a steady 3,000 tpd. Gold production is projected to scale toward 300,000 oz in 2026.

- Marmato Complex: Construction of the Bulk Mining Zone is over 60% complete. This is the "crown jewel" growth catalyst for late 2026, expected to eventually double Marmato's output.

- Soto Norte: Environmental studies are being submitted in H1 2026, marking the next major permitting milestone for this multi-million ounce asset.

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Ultra-High Grade: Segovia remains one of the highest-grade underground mines globally (~10-11 g/t Au).

- Strong Cash Balance: ~$418M in liquidity provides a massive buffer for project development without immediate dilution.

- Management Pedigree: Led by Neil Woodyer and Ian Telfer (architects of Endeavour and Goldcorp), the "smart money" follows the leadership.

Weaknesses

- Jurisdictional Concentration: Most production is currently concentrated in Colombia, which carries inherent political and security perceptions.

- High Capital Intensity: Simultaneous expansions at Marmato and Soto Norte require heavy reinvestment of operating cash flow.

Opportunities

- 1 Million Ounce Goal: Aris has a clear, documented path to becoming a 1 Moz/year producer by the late 2020s.

- M&A Potential: As a consolidated owner of 100% of its assets, Aris is a prime target for majors looking for high-grade growth in South America.

Threats

- Regulatory Hurdles: Soto Norte's permitting process is complex and subject to environmental scrutiny.

- Currency Volatility: Fluctuations in the Colombian Peso (COP) can impact local operating costs.

Risks to Watch

While the stock is currently in favor, retail investors should monitor:

- Execution Risk: Any delays in the August 2026 completion of the Marmato decline could stall momentum.

- Gold Price Sensitivity: Mid-tier miners like ARIS often move with higher beta than seniors (Barrick/Newmont) when gold prices fluctuate.

- Social Stability: Maintaining the formalization agreements with small-scale miners is critical to operational continuity.

Conclusion

Aris Mining’s 4% pop on January 5 reflects a market that is finally pricing in consistent execution over speculative growth. With 100% ownership of its key assets and a massive cash pile, the company is no longer just a "promising junior"—it is a mid-tier operator with a clear trajectory toward 500,000 oz/year in the near term and 1 Moz/year in the long term.

Please wait processing your request...

Please wait processing your request...