The Quick Snapshot

While the broader TSX Composite drifted lower yesterday as traders entered "holiday hibernation, BCE Inc. bucked the trend, climbing ~1.84% to close near CAD 32.02.

Why the sudden love for a stock that has battled headwinds all year? It wasn’t a single press release drop. Instead, it was a "perfect mini-storm" of defensive rotation, lingering analyst optimism, and a yield-hungry market positioning for 2026 rate cuts.

Here is your no-fluff breakdown of why the telecom giant is moving, how its business model is radically shifting, and the risks you must watch.

Key Drivers: Why the Green Candle?

Source: Kalkine Group

- The "Santa Claus" Defensive Rotation: As volume thins out between Christmas and New Year's, smart money often rotates into "Safe Havens." On Dec 29, the Communication Services sector led the TSX (up ~1.13%). Investors parked cash in BCE for safety, betting on its recurring revenue streams over volatile cyclical stocks (like mining or tech) ahead of 2026.

- The "Analyst Upgrade" Afterglow: The market is still digesting major upgrades from earlier in December:

- BMO Capital Markets: Upgraded to "Outperform" (Dec 11).

- CIBC: Upgraded to "Sector Outperform" (Dec 9).

- Why? The consensus is that the worst of the regulatory punishment and interest rate pain is priced in.

- The Yield Magnet (5.5%+ Yield): With the ex-dividend date passed (Dec 15) and a payment coming Jan 15, 2026 ($0.4375/share), income investors are locking in positions. As bond yields fluctuate, BCE’s dividend—now looking safer due to asset sales—remains a prime target for passive income portfolios.

Business Model 2.0: Not Your Grandpa’s Phone Company

BCE is aggressively pivoting from a "Canadian Utility" to a "North American Tech-Co."

- US Expansion (Project Ziply): BCE is no longer landlocked in Canada. The integration of Ziply Fiber (US Pacific Northwest) is live. This transforms BCE into the 3rd largest fiber operator in North America, diversifying revenue away from the saturated Canadian market.

- AI as a Service: This is the sleeper hit. BCE’s "Enterprise Solutions" are booming (up 34% YoY in Q3), driven by Ateko and Bell Cyber. They aren't just selling internet lines to businesses; they are selling the AI and security layers on top of it.

- Leaner Operations: The company is executing a massive $1.5B cost-saving plan (2025-2028), ruthlessly cutting legacy copper networks and reducing headcount to improve margins.

Latest Financial Pulse (Q3 2025 Recap)

- Revenue: $6.05B (+1.3% YoY). Growth is back, fueled by Ziply.

- Adjusted EPS: $0.79 (Beat estimates of $0.52). Profitability is stabilizing.

- Free Cash Flow (FCF): $1.0B (+20.6% YoY). Critical for protecting that dividend.

- Leverage: Net Debt remains high at ~3.8x EBITDA, but the sale of their MLSE stake (Maple Leafs/Raptors parent co) provided billions to pay down debt and fund the US expansion.

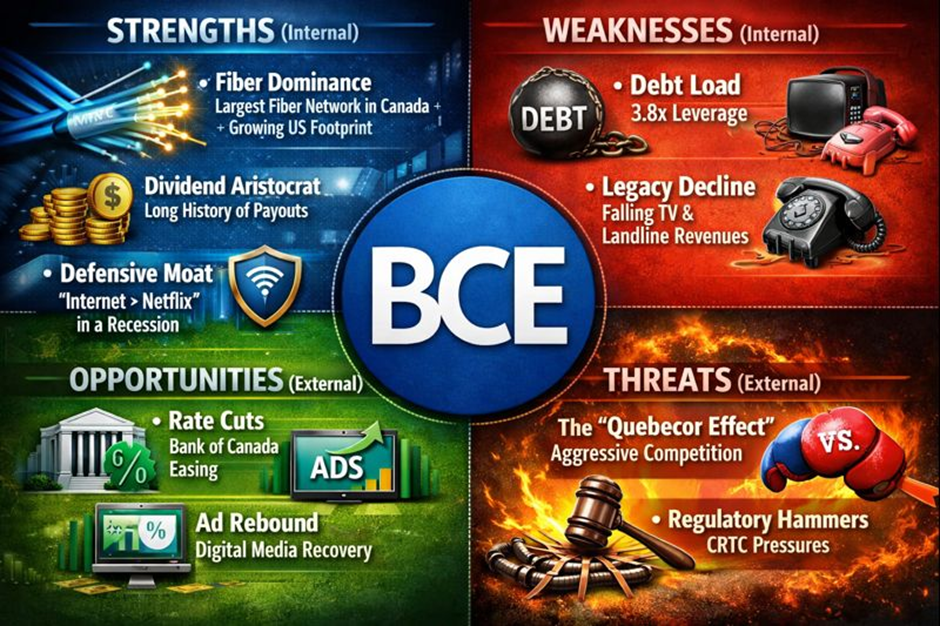

SWOT Analysis: The Bull vs. Bear Case

Source: Kalkine Group

Strengths (Internal)

- Fiber Dominance: Largest fiber footprint in Canada + growing US footprint.

- Dividend Aristocrat Status: A long history of payouts (though the payout ratio is tight).

- Defensive Moat: In a recession, people cancel Netflix before they cancel their internet.

Weaknesses (Internal)

- Debt Load: 3.8x leverage is uncomfortable. High interest rates hurt them more than others.

- Legacy Decline: Traditional TV and landline revenues are melting away faster than they can be replaced.

Opportunities (External)

- Interest Rate Cuts: Every rate cut by the Bank of Canada in 2026 directly boosts BCE’s bottom line (lower debt servicing costs).

- Digital Ad Rebound: As the economy stabilizes, Bell Media ads could bounce back.

Threats (External)

- The "Quebecor Effect": Aggressive pricing from competitors (Quebecor/Freedom) is forcing BCE to lower prices, hurting margins.

- Regulatory Hammers: The CRTC (regulator) continues to force big telcos to share their fiber networks with smaller rivals, potentially killing investment returns.

The Risks You Can't Ignore

- The "Value Trap" Risk: BCE looks cheap, but if growth stalls (0-2% revenue guidance), the stock price may stagnate even if the dividend pays out.

- Dividend Safety: While FCF is up, the payout ratio is consistently near or above 100% of earnings (though lower as % of FCF). If a recession hits, that dividend could be frozen or cut—a scenario famously dubbed the "dividend trap."

- Execution Risk: Mergers are hard. If the Ziply Fiber integration in the US hits snags, it could drain cash instead of generating it.

Conclusion

BCE’s +1.84% pop isn't about a single day of news—it's a sign that the market believes the company has turned a corner. The massive restructuring, the sale of sports assets to pay down debt, and the bold move into the US fiber market are finally earning respect from analysts.

Please wait processing your request...

Please wait processing your request...