The quiet Canadian resource sector is now ground zero for the fiercest geopolitical battle of the decade: the race to secure critical minerals. Forget gold; the new currency is Lithium, Graphite, Nickel, and Rare Earth Elements (REEs). With the Federal Government unleashing a massive C$6.4 billion investment and designating these metals as crucial to national defense, Canada is no longer just a source—it’s the West's protected supply chain fortress.

Part I: The Seismic Shift – Latest Data and the C$30.2 Billion Sector

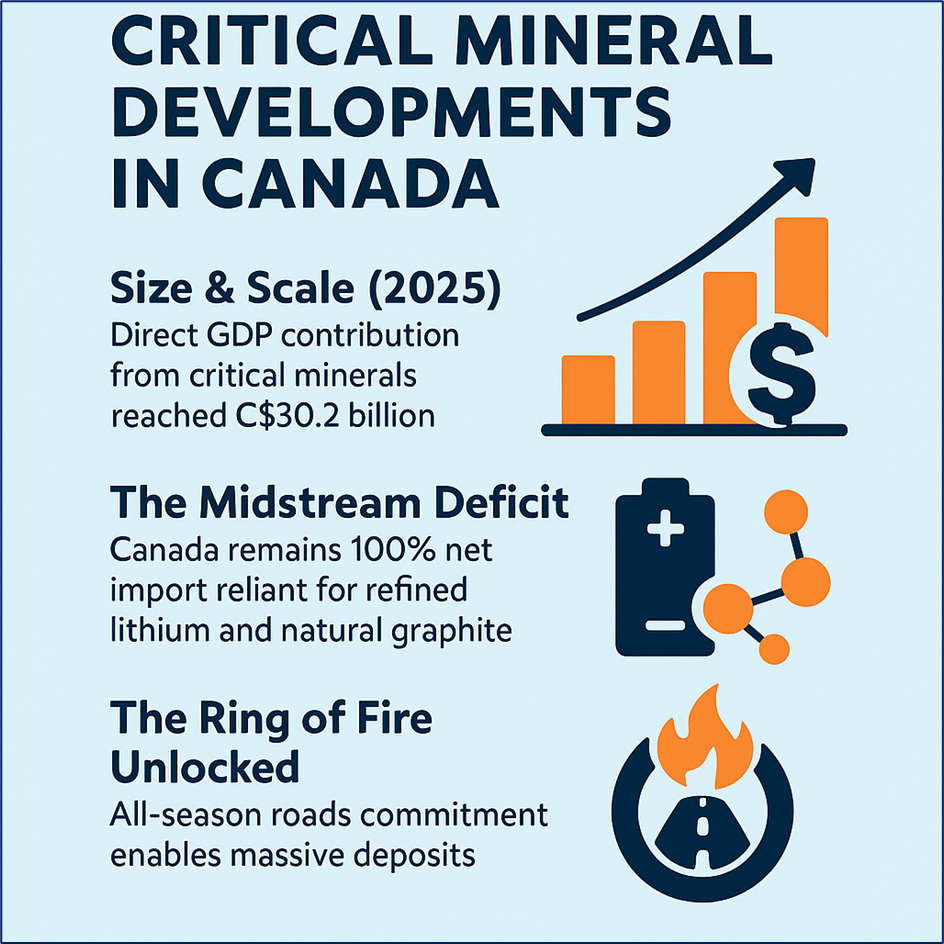

Data That Proves the Thesis:

- Size & Scale (2025): The critical mineral sector's direct contribution to Canada's GDP surged to C$30.2 billion (latest government figures), driven by both price spikes and increased project velocity. This represents an aggressive 63% growth in nominal GDP contribution since 2019.

- The Midstream Deficit: Despite massive reserves, Canada’s fatal flaw has been a reliance on foreign processing. Latest data shows Canada remains 100% net import reliant for refined lithium and natural graphite for battery anodes. The 2026 theme is explicitly targeting this gap through aggressive domestic refining incentives.

- The Ring of Fire Unlocked: Ontario’s commitment to building all-season roads into the Ring of Fire region—a vast deposit of Nickel, Copper, and Chromite—is a literal infrastructure investment that de-risks multi-billion-dollar projects, setting up a major production push for 2026-2030.

Source: Kalkine Group

Part II: Regulation, Investment, and The UK Connection

The Canadian Critical Minerals Strategy (CCMS) is not a suggestion; it’s a fully funded industrial plan using sovereign tools to align private capital with national interests.

The Government’s C$6.4 Billion Strategic Toolkit:

- Offtake Agreements as De-Risking: The most powerful tool is the use of Offtake Contracts (guaranteed buyers) from government-backed entities. Recent deals for Graphite (e.g., Nouveau Monde Graphite) and Scandium (e.g., Rio Tinto) provide cash-flow certainty, turning pre-production projects into bankable assets for retail investors to track.

- The Stockpile Mandate: Canada has formally designated critical minerals as essential to national defense. This triggers the ability to build a strategic national stockpile and support NATO allies, creating a powerful, non-market-driven buyer of last resort—a major boost against commodity price volatility.

- Allied Supply Chain Fortress (The UK Axis): The UK-Canada Critical Minerals Supply Chains Dialogue has created a unique axis. The UK, needing secure supply for its booming gigafactories and defense needs, is leveraging UK Export Finance (UKEF) to co-invest. This partnership extends to Recycling and Circularity R&D (e.g., Mkango Resources’ UK recycling focus), positioning Canadian-linked companies to supply both North America and Europe.

Source: Kalkine Group

Part III: The Critical Minerals Companies to Track in 2026

For retail investors, the focus should be on companies transitioning from "exploration hope" to "production certainty," especially those with confirmed government funding or strategic partnerships. These stocks represent a direct play on the "friend-shoring" of the Western supply chain.

The Heavy-Hitters (Midstream & Producers):

- Neo Performance Materials (TSX: NEO) – The Magnet Master:

- The Play: Not a miner, but a crucial midstream processor that turns Rare Earth Oxides into high-purity permanent magnets—the heart of EVs and wind turbines.

- 2026 Edge: Highly insulated from mining risks. It’s a direct play on US/EU defense and EV demand, positioning itself as one of the few ex-China processors globally. A geopolitical staple.

- Teck Resources (TSX: TECK.B) – The Copper Giant:

- The Play: The cornerstone of Canadian mining. While diversified, its massive Copper portfolio (in BC) is the essential foundation for all electrification infrastructure (grids, charging stations, EVs).

- 2026 Edge: Exceptional ESG profile and scale make it a preferred copper source for global EV manufacturers. A reliable, blue-chip way to bet on the electrification boom.

- Nouveau Monde Graphite (TSX: NOU) – Government’s Chosen One:

- The Play: Developing the flagship Matawinie Graphite Project in Quebec, aiming to supply battery-grade anode material.

- 2026 Edge: Confirmed offtake agreements with the Government of Canada and strategic partners like Panasonic (Japan) have de-risked its path to production, making it a critical, federally backed project.

The High-Potential Developers (Projects Nearing Critical Milestones):

- Ucore Rare Metals Inc. (TSXV: UCU) – North American REE Processing:

- The Play: Building a Rare Earth Elements separation facility in Kingston, Ontario, vital for breaking China’s chokehold on REE processing.

- 2026 Edge: Conditionally approved for a C$36.3 million investment from the Canadian government, cementing its role as a strategic national asset in the most geopolitically sensitive mineral chain.

- Northern Graphite (TSXV: NGC) – North America's Only Producer:

- The Play: Operates the only producing graphite mine in North America (Lac des Iles, Quebec) and plans to expand downstream processing.

- 2026 Edge: Benefited from the recent government critical minerals initiative, securing funding to advance its domestic processing plans, which directly addresses the 100% import reliance problem.

- Electra Battery Materials (TSXV: ELBM) – The Cobalt Catalyst:

- The Play: Operating the only North American-focused cobalt sulfate refinery in Ontario. Cobalt is crucial for high-energy density batteries.

- 2026 Edge: This is a direct play on midstream refining. Proximity to the US and Ontario EV manufacturing hubs provides a massive logistical and security advantage. Completion of the refinery in 2026 is a major catalyst.

- Lithium Americas (TSX: LAC) – US & Canada Lithium Kingpin:

- The Play: Split into two companies: one focused on US assets (Thacker Pass) and one on South American operations. The Canadian-listed entity has deep ties to the continent's lithium future.

- 2026 Edge: Backed by huge OEM investments (General Motors) and significant US government support, this is a clear 'fast-track' lithium project designed to serve the domestic EV market rapidly.

Conclusion: Beyond the Boom – The Strategic Long Game

The Canadian Critical Minerals sector is undergoing a necessary and unprecedented re-calibration. The days of simply digging up dirt are over. The focus for 2026 is unequivocally on security, domestic processing, and the complete, traceable supply chain.

The C$6.4 billion injection is not a subsidy; it is a premium paid for supply chain sovereignty. This generational investment opportunity is underpinned by stable governance and high ESG standards, offering a compelling alternative to more volatile, less-transparent global sources. For investors, the stocks that successfully bridge the gap from reserve to refined product—especially those with government and allied (UK) backing—are the ones positioned for the most explosive growth. The race for the green future runs through Canada.

Please wait processing your request...

Please wait processing your request...