As the global geopolitical landscape shifts toward a state of permanent rearmament, the Canadian defense sector has emerged as a fertile ground for wealth compounding. In 2026, the S&P/TSX Composite has outpaced Wall Street, driven by a rotation into "hard assets" and sovereign security plays.

Top global fund managers from BlackRock to Goldman Sachs are increasingly viewing Canadian aerospace and defense firms not just as cyclical trades, but as secular growth engines with multi-bagger potential.

Source: Kalkine Group

Here is the updated analysis for MDA Space, Exchange Income Corp, and CAE Inc., incorporating current 2026 market data and technical setups.

The Orbital Intelligence Play

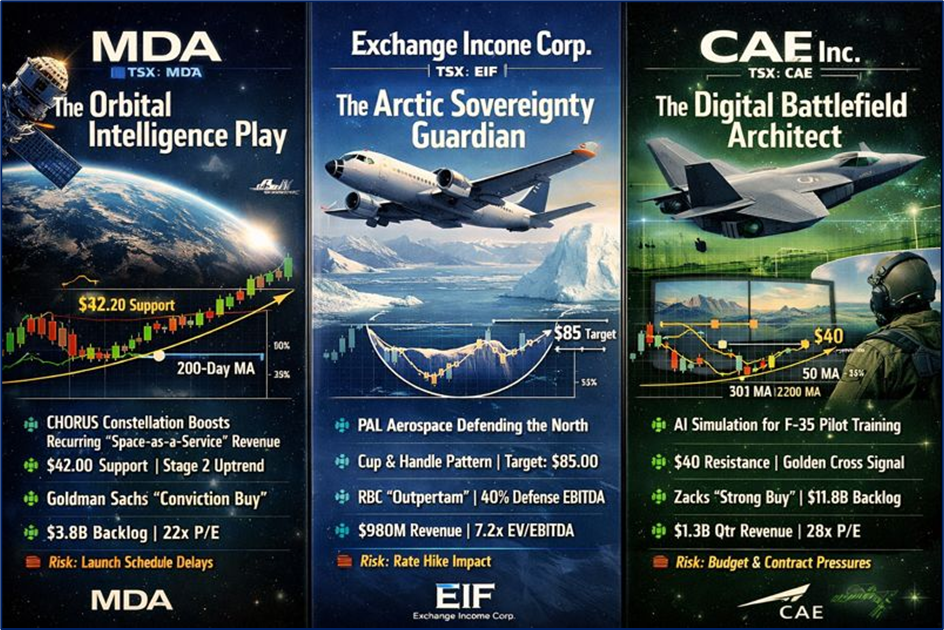

MDA has transitioned from a hardware manufacturer to a high-margin data provider. The successful monetization of the CHORUS constellation has shifted the business model toward recurring "Space-as-a-Service" revenue, providing high-resolution Earth observation for NATO and commercial clients.

- Technical Analysis: MDA is currently in a confirmed Stage 2 advancing phase. Having broken out in 2025, the stock has established a formidable support base at $42.00. The 200-day moving average is trending sharply upward at a $30 angle, acting as a dynamic floor. Volume remains higher on "up" days, confirming institutional accumulation.

- Smart Money: Goldman Sachs maintains a "Conviction Buy," citing MDA’s 90% dominance in Canadian satellite tech. EODHD/Others data shows a 4:1 Buy-to-Hold ratio, with hedge funds increasing exposure to hedge against terrestrial geopolitical instability.

- Financials: The company boasts a record $3.8 billion backlog. Recent EBITDA margins expanded by 450 basis points, driven by the highly efficient Brampton production line.

- Valuation: Trading at a Forward P/E of 22x, it remains a value play compared to US peers like Rocket Lab.

Risk Factor: Deployment of international military comms networks is the primary catalyst; failure in launch schedules remains the top risk.

2. Exchange Income Corp (TSX: EIF)

The Arctic Sovereignty Guardian

EIF has evolved from a steady income stock into a high-growth defense powerhouse. Through PAL Aerospace, EIF is now the critical infrastructure provider for Arctic surveillance as the region becomes a primary geopolitical flashpoint in 2026.

- Technical Analysis: EIF has shattered its "income trap" reputation by clearing $62.00 resistance on record-breaking volume. The weekly chart displays a classic "Cup and Handle" pattern, a bullish continuation signal. With the handle now fully formed, technical targets sit at $85.00, supported by a rising Relative Strength (RS) line.

- Smart Money: RBC Capital Markets recently upgraded the stock to "Outperform," targeting $1.5 billion in defense-specific revenue. Major pension funds like CDPQ and OTPP are consistent buyers for the 5.1% yield and defense growth.

- Financials: Defense now accounts for 40% of total EBITDA (up from 25%). Quarterly revenue recently topped $980 million, beating analyst estimates by 12%.

- Valuation: Despite the price surge, EIF trades at 7.2x EV/EBITDA, which is significantly below the industry average for defense contractors.

Risk Factor: Acquisition-led growth strategies may face headwinds if interest rates remain elevated through late 2026.

The Digital Battlefield Architect

CAE has successfully rebranded as an AI-simulation leader. By 2026, its proprietary AI for simulating electronic warfare has become the gold standard for F-35 pilot training, moving the company away from capital-intensive hardware toward high-margin software licenses.

- Technical Analysis: CAE has completed a multi-year "V-shaped" recovery. The stock is currently testing the $40.00 psychological level (pre-pandemic highs). A "Golden Cross" (the 50-day moving average crossing above the 200-day) occurred in November 2025, signaling that the long-term trend has shifted from bearish to decisively bullish.

- Smart Money: Zacks ranks CAE as a "Strong Buy." BMO Capital highlights the "margin expansion story," with defense margins hitting a record 14.5% as the L3Harris partnership scales.

- Financials: The "Simulation-as-a-Service" model has pushed the total backlog to $11.8 billion. Q3 2025 revenue reached $1.3 billion, fueled almost entirely by the Defense & Security division.

- Valuation: Trading at a P/E of 28x. While high for the TSX, it reflects a "software premium" similar to US firms like Palantir. Management is prioritized on reaching a 2.0x Net Debt/EBITDA target.

Risk Factor: Fixed-price contract overruns and the pace of US defense budget approvals remain the primary variables for 2026 performance.

Conclusion

The 2026 TSX defense basket has matured. MDA offers the highest pure-growth potential in space, EIF provides a unique combination of high yield and Arctic defense growth, and CAE acts as the high-tech software backbone of global military training. For the wealth-compounding investor, these three represent the "Iron Triangle" of Canadian aerospace and defense.

Please wait processing your request...

Please wait processing your request...