The stock of Laurentian Bank of Canada (TSX: LB) surged yesterday following the announcement of a massive, value-unlocking strategic transaction. This comprehensive article breaks down the core reasons for the rally, the bank's transitioning model, risks, and the outlook for investors.

1. The Catalyst: A Dual Acquisition and Cash Premium

The primary driver of the stock surge was the announcement that Laurentian Bank's operations will be acquired in a two-part transaction valued at approximately C$1.9 billion.

- The Premium: The buyers agreed to pay C$40.50 per share in cash for all outstanding shares. This price represented a significant premium - around 20% over the closing price just before the news broke, fuelling yesterday's intense buying activity.

- The Split Buyers:

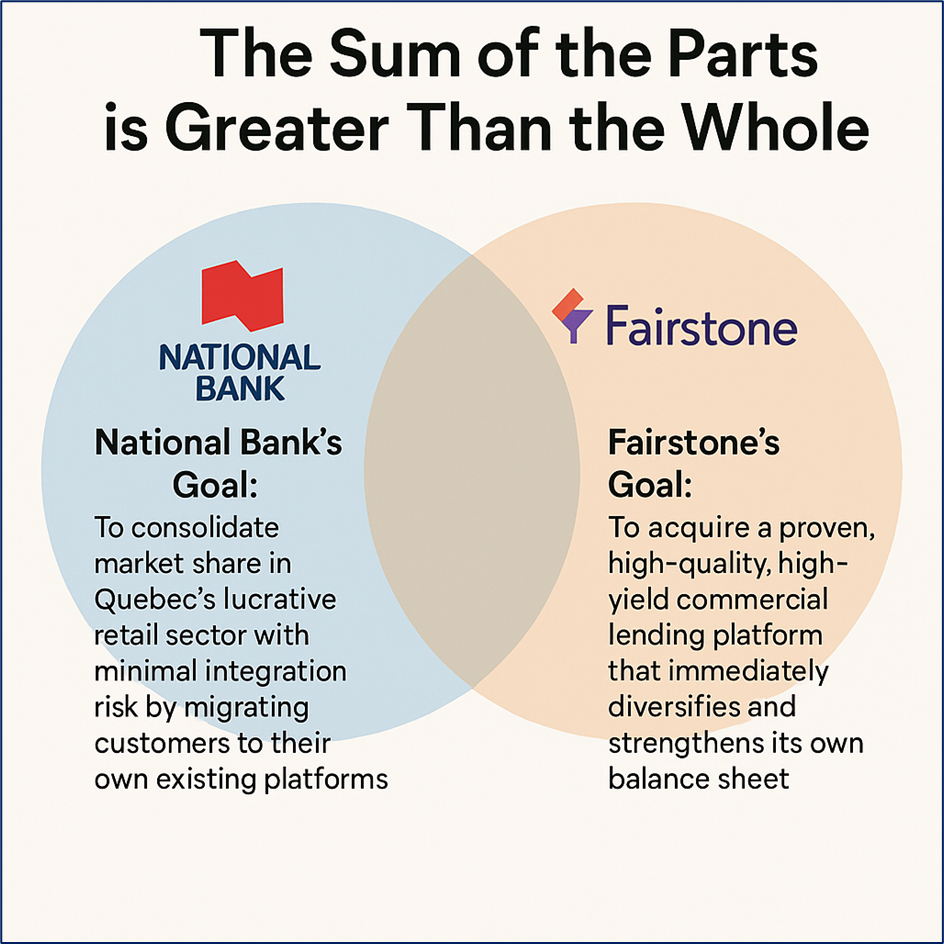

- Fairstone Bank of Canada (backed by Smith Financial Corporation) will acquire the majority of the organization, focusing on the specialized Commercial and Capital Markets divisions.

- National Bank of Canada (NA) will acquire the Retail and Small-to-Medium Enterprise (SME) banking portfolio, including approximately C$3.3 billion in loans and C$7.6 billion in deposits.

Source: Kalkine Group

Business Model: The Great Unbundling Explained

The transaction marks the end of Laurentian's attempt to compete as a full-service, hybrid bank.

The Old Model (Pre-Deal)

Laurentian operated with three main pillars:

- Retail Banking: Mortgages, personal accounts, and investments, predominantly in Quebec.

- Commercial Banking: Specialized high-yield lending in sectors like commercial real estate and inventory financing across North America.

- Capital Markets: Institutional services.

Source: Kalkine Group

The Strategic Shift (Post-Deal Reality)

The sale is the logical conclusion of the bank's long-term strategy to pivot to a "specialty commercial bank":

- Focus on Specialty: The Commercial division—the most valuable part—will be integrated into Fairstone, allowing it to scale its successful expertise in specialized lending.

- Retail Exit: Selling the lower-margin Retail arm to National Bank eliminates the high operational costs and lack of scale that plagued Laurentian's personal banking efforts.

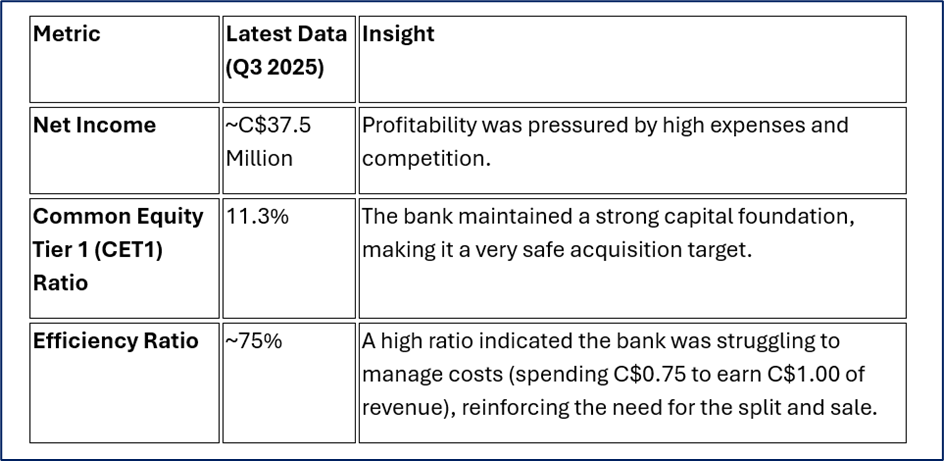

Financial & Operational Updates (Q3 2025 Context)

While the Q4 2025 results are imminent (scheduled for December 5, 2025), the decision to sell was made against a backdrop of recent operational challenges.

Data Source: Company Fillings

Operational Insight: The sale validates the market's long-held view that Laurentian's value was trapped by its high operating expenses and its inability to keep pace with digital transformation.

Strategic Rationale and Long-Term Outlook

Source: Kalkine Group

Outlook for Shareholders:

The future is now tied to a merger arbitrage opportunity. Shareholders can expect a cash payout of C$40.50 per share. The stock will likely trade just below this price until the deal is completed, offering a near-term, fixed-return investment until the expected closing in late 2026.

Key Risks

While the cash offer is firm, there are key risks tied to the transaction timeline:

- Regulatory Approvals: The deal requires clearance from both the Competition Bureau and the Minister of Finance. This process can be lengthy and occasionally unpredictable.

- Execution Risk: The long closing timeline (late 2026) means capital will be tied up. If the deal were to fail for any reason (e.g., regulatory blockage), the stock price would likely revert to its pre-announcement trading levels.

Conclusion

Laurentian Bank's surge is the market celebrating a definitive and profitable end to a long-running struggle for scale. The acquisition offers shareholders an excellent exit at a premium, marking a significant moment of consolidation in Canadian finance.

Source: Trading View, 2 December 2025

Please wait processing your request...

Please wait processing your request...