The Red Metal’s Revenge: Why Fund Managers are Crowding into Copper

The global investment community has reached a rare consensus: we are entering a multi-year copper supercycle. Driven by the relentless expansion of AI data centres, the electrification of the global vehicle fleet, and a chronic lack of new mine discoveries, analysts at Goldman Sachs and Citigroup are forecasting copper prices to surge toward $12,500 - $13,000 per metric ton by the second quarter of 2026.

Investment banks have identified a structural supply gap that cannot be closed by recycling alone, forcing "smart money" to pivot toward high-quality producers on the Toronto Stock Exchange (TSX). Institutional fund managers are aggressively rotating out of diversified miners and into pure-play or copper-heavy operators that can provide immediate leverage to these skyrocketing prices.

Source: Kalkine Group

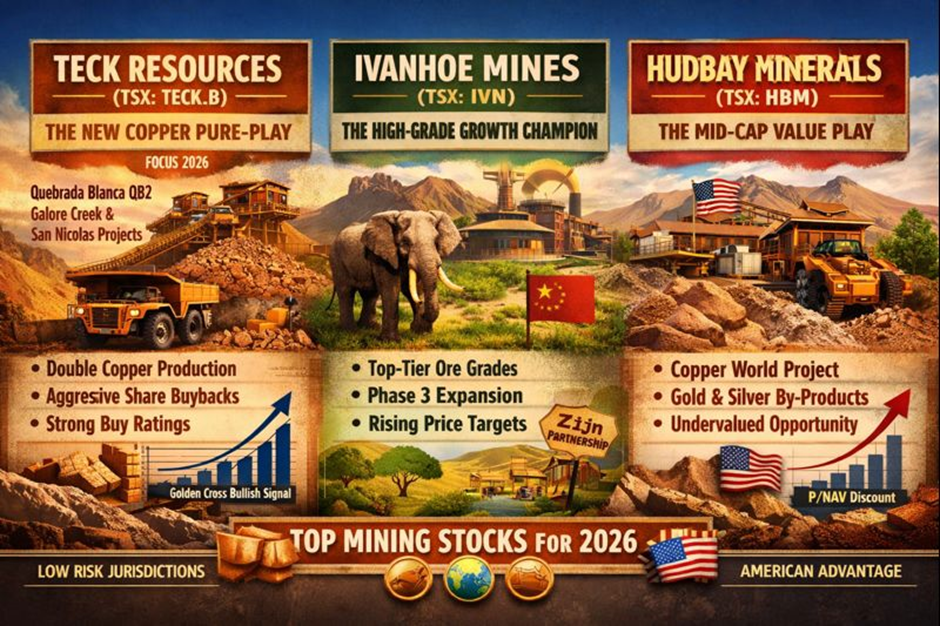

Teck Resources Limited (TSX: TECK.B) – The New Global Copper Pure-Play

The Transformation Catalyst and 2026 Strategic Drivers

Teck Resources has completed its metamorphosis from a diversified coal-and-metals giant into a streamlined copper powerhouse. Following the divestment of its steelmaking coal business, the company is now laser-focused on its Quebrada Blanca (QB2) operation in Chile. Fund managers favor Teck because it offers the cleanest exposure to copper among large-cap Canadian miners. The primary driver for 2026 is the full-scale ramp-up of QB2, which is expected to double Teck’s copper production capacity. This massive influx of cash flow is earmarked for aggressive share buybacks and the development of a world-class project pipeline that includes the Galore Creek and San Nicolas projects.

Financial Vitality and Operational Excellence

Teck's business model is now built around high-margin, long-life assets in low-risk jurisdictions. For the 2026 fiscal year, analysts expect a significant reduction in net debt and a "meaningful" increase in the base dividend, currently supplemented by a variable dividend policy tied to free cash flow. Latest Valuation: Teck trades at a forward EV/EBITDA that many brokers consider a discount compared to its peer Freeport-McMoRan, especially given its peer-leading growth profile. Technical Analysis: The stock has recently established a strong support floor near its 200-day moving average, with a "Golden Cross" formation emerging in early 2026, signaling a long-term bullish trend.

Latest Analyst Consensus: The "Strong Buy" Parade

In January 2026, BMO Capital Markets and Scotiabank reiterated their "Outperform" ratings, citing Teck's superior balance sheet and successful operational execution at QB2. While some downgrades occurred in 2024 due to project delays, the 2026 sentiment is overwhelmingly positive as those execution risks have faded.

Risk Factors: Potential for labor strikes in Chile, fluctuating water availability for processing plants, and the inherent volatility of the LME copper price.

Ivanhoe Mines Ltd. (TSX: IVN) – The High-Grade Growth Champion

Kamoa-Kakula: The Engine of Growth

Ivanhoe Mines is the darling of institutional investors seeking "pure growth." Its flagship Kamoa-Kakula complex in the Democratic Republic of Congo (DRC) is not just a mine; it is a generational asset. By 2026, Ivanhoe is projected to be the world’s third-largest copper producer. The latest operational updates highlight the commencement of Africa's largest and greenest copper smelter, which will drastically reduce transportation costs and carbon footprints. Smart money is betting on Ivanhoe because its ore grades—averaging between 3.5% and 4.5%—are nearly ten times higher than the global industry average.

Business Model and Financial Resilience

Ivanhoe’s model relies on strategic partnerships, notably with Zijin Mining, which provides both technical expertise and a direct pipeline into Chinese demand. The company is transitioning from a developer to a massive cash generator. While it does not currently pay a significant dividend, management has signaled that 2026 could see the introduction of a formal capital return framework. Latest Valuation: Despite its recent rally, many analysts argue the stock has not yet priced in the full value of its Western Foreland exploration area, which could be another Kamoa-scale discovery.

Technical Landscape and Analyst Sentiment

Technically, IVN is trading in a robust ascending channel. Volume profiles show heavy institutional accumulation on any minor dips. Latest Analyst Upgrades: UBS and Morgan Stanley have recently raised their price targets, pointing to the successful de-risking of Phase 3 expansions.

Risk Factors: Heightened geopolitical risk in the DRC, potential changes to mining codes, and infrastructure bottlenecks related to power supply and regional rail logistics.

Hudbay Minerals Inc. (TSX: HBM) – The Mid-Cap Value Play

Copper World and The American Advantage

Hudbay Minerals has emerged as the preferred pick for brokers looking for "undervalued" mid-cap gems. The primary driver for 2026 is the development of the Copper World project in Arizona. This asset provides Hudbay with a strategic foothold in the United States, a jurisdiction that is increasingly prioritizing domestic mineral security. Fund managers appreciate Hudbay’s diversified production base, which includes high-margin operations in Peru (Constancia) and Canada (Snow Lake), providing a steady stream of gold and silver by-products that lower their overall "cash cost" per pound of copper.

Operational Update and Valuation Gap

Hudbay’s recent financial results showed record-breaking throughput and a significant beat on EBITDA, driven by higher-grade ore at its Pampacancha deposit. The company maintains a disciplined business model focused on organic growth and debt deleveraging. Latest Dividend: Hudbay pays a semi-annual dividend, which, while modest, is seen as sustainable and likely to grow as Copper World approaches production. Latest Valuation: On a Price-to-Net Asset Value (P/NAV) basis, Hudbay continues to trade below its historical average, making it a prime candidate for a re-rating or a potential takeover target by a larger major.

Technical Analysis and Broker Ratings

The stock has shown significant relative strength compared to the TSX Materials Index. Analysts at National Bankshares and RBC Capital Markets have issued "Buy" ratings in the first week of 2026, highlighting the company’s ability to generate significant free cash flow even if copper prices remain stagnant.

Risk Factors: Permitting hurdles for the Arizona project, social unrest possibilities in Peru, and inflationary pressures on mining consumables like diesel and explosives.

The Verdict: Positioned for a Supply-Constrained World

The case for TSX copper stocks in 2026 is built on a simple, inescapable reality: the world needs more copper than it can currently produce. Whether it is the large-cap stability of Teck, the explosive high-grade growth of Ivanhoe, or the strategic North American leverage of Hudbay, these three companies represent the "best-in-class" options for investors looking to capitalize on the energy transition. Smart money is already positioned; for retail investors, the window of opportunity is defined by these operational milestones and the looming global deficit.

Please wait processing your request...

Please wait processing your request...