Freehold Royalties Ltd. (TSX: FRU) continues to command attention in the Canadian energy landscape, currently offering a substantial 6.9% dividend yield that stands out in a shifting interest rate environment. Unlike traditional exploration and production companies, Freehold operates as a pure-play royalty vehicle, collecting "rent" on oil and gas production across millions of acres in North America without incurring the heavy capital costs or environmental liabilities of drilling.

This unique structural advantage, paired with a strategic pivot toward high-margin U.S. basins, has transformed the company into a premier income-generating machine for retail and institutional investors alike.

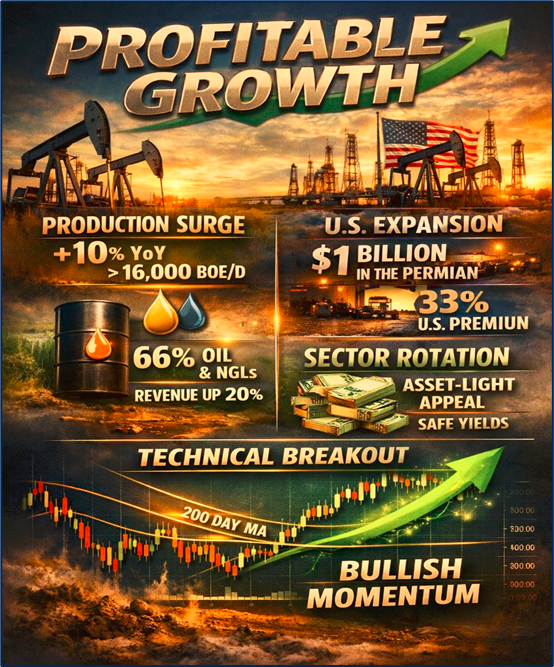

Latest Key Reasons for Surge and Drivers

Source: Kalkine Group

- Production Momentum: A significant 10% year-over-year increase in total production, reaching over 16,000 boe/d, has provided a robust foundation for share price appreciation.

- U.S. Expansion Success: The company’s aggressive deployment of nearly $1 billion into premium U.S. basins (specifically the Permian Midland) is paying off, with U.S. assets now generating a 33% pricing premium over Canadian barrels.

- Liquids Weighting: A strategic shift toward higher-value oil and natural gas liquids (now making up approximately 66% of production) has increased the revenue generated per barrel by nearly 20% compared to previous years.

- Sector Rotation: As volatility returns to broader markets, investors are rotating into "asset-light" energy models that offer immediate yield without the operational risks of drilling.

- Technical Breakouts: Recent price action saw the stock cross its 200-day moving average, triggering bullish sentiment among technical traders and momentum-focused institutional funds.

Current Business Model

Freehold Royalties operates a low-risk, high-margin business model centered on mineral ownership.

- The "Landlord" Approach: The company owns the rights to the minerals under the soil but does not drill or operate the wells themselves.

- No Capital Expenditure: Because they do not operate the assets, Freehold has zero capital costs, zero operating expenses (OPEX), and zero end-of-life abandonment liabilities.

- Gross Overriding Royalties (GORR): In Canada, they often hold a percentage of the revenue from the operator. In the U.S., they own "mineral title," meaning they own the land and lease it to major operators like ExxonMobil and ConocoPhillips.

- Revenue Generation: For every barrel of oil or cubic foot of gas produced by an operator on their land, Freehold receives a top-line percentage, making it one of the highest-margin businesses in the energy sector.

Latest Financial, Operational, and Dividend Updates (company sourced)

- Dividend Declaration: On January 15, 2026, the Board declared a monthly dividend of $0.09 per share, payable on February 17, 2026, to shareholders of record on January 30, 2026 (Company Source: GlobeNewswire).

- Production Volume: Reported Q3 2025 production of 16,054 boe/d, a 10% increase compared to 14,643 boe/d in the same period of 2024 (Company Source: Q3 2025 Financial Report).

- Funds from Operations (FFO): Generated $59 million ($0.36/share) in FFO for the most recent quarter, comfortably covering the $44 million ($0.27/share) in dividends paid during that period (Company Source: Q3 2025 News Release).

- Balance Sheet Strength: Expanded its credit facility to $500 million, extending the term to November 2028, and maintaining a conservative net debt to FFO ratio of approximately 1.1x (Company Source: Q3 2025 Conference Call).

- Portfolio Diversification: The current revenue mix is now approximately 75% U.S. and 25% Canada, reflecting the successful execution of the North American diversification strategy (Company Source: Investor Presentation November 2025).

Latest Analyst Coverage

- Scotiabank: Recently boosted its price target to $16.00 from $15.00, maintaining a "Sector Perform" rating as of January 20, 2026 (Source: MarketBeat).

- National Bankshares: Downgraded the stock from "Outperform" to "Sector Perform" on January 9, 2026, setting a target price of $15.00, citing the stock reaching its valuation parity (Source: National Bank Financial).

- Raymond James: Upgraded the stock to "Moderate Buy" with a price target of $17.50, highlighting the "ground game" in the Permian Basin as a long-term value driver (Source: Raymond James Equity Research).

- Canaccord Genuity: Raised its price objective to $17.00, noting the company’s ability to sustain dividends even if oil prices retreat toward US$50/bbl WTI (Source: Canaccord Genuity).

Outlook and Risks

Outlook for 2026

- Acquisition Pipeline: Management has indicated a continued focus on "ground game" acquisitions—buying small, high-quality mineral parcels directly from landowners in the Permian to achieve higher returns (20%+).

- Inventory Depth: With over 42,000 potential drilling locations across North America, the company has decades of inventory that can be developed by operators without Freehold spending a dollar.

- Payout Sustainability: The current dividend remains sustainable down to a WTI oil price of approximately US$50/bbl, providing a significant margin of safety.

Potential Risks

- Commodity Price Sensitivity: While the business model is asset-light, revenue is still directly tied to the price of oil and gas. A global recession leading to a sustained price collapse would impact FFO.

- Operator Capital Allocation: Freehold does not control when or where operators drill. If major partners (like CNRL or Exxon) decide to reduce capital spending on Freehold-leased lands, production growth could stall.

- Currency Fluctuations: With 75% of revenue now coming from the U.S., the CAD/USD exchange rate significantly impacts the final Canadian dollar distributions to TSX shareholders.

Conclusion

Freehold Royalties stands as a unique hybrid of a yield-heavy income stock and a diversified energy play. By decoupling itself from the operational headaches of traditional oil companies, it has carved out a niche that offers high margins and consistent monthly distributions. While its growth is tethered to the drilling decisions of its world-class operators and the vagaries of global commodity prices, its current 2026 trajectory suggests a company successfully pivoting toward the most profitable energy basins in the world.

Please wait processing your request...

Please wait processing your request...