Ero Copper Corp. (TSX: ERO) dominated the TSX on December 30, 2025, closing up ~4.2% at a record-breaking CAD 39.31. This rally isn't just a flash in the pan—it’s the culmination of a massive 111% surge over the past year.

As the world pivots toward electrification, Ero Copper has positioned itself as a high-growth, low-cost producer ready to ride the "Super Cycle."

Why the Surge? Key Drivers Behind the Dec 30 Rally

The 4.2% jump was fueled by a "perfect storm" of operational milestones and macroeconomic tailwinds:

Source: Kalkine Group

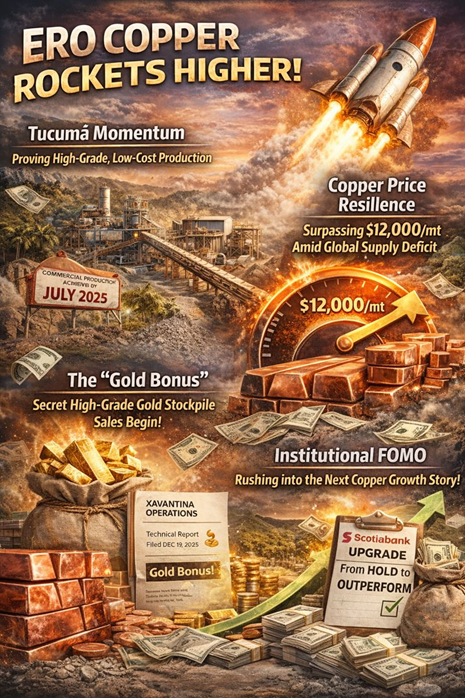

- Tucumã Momentum: Investors are reacting to the successful ramp-up of the Tucumã Operation, which achieved commercial production in July 2025. By year-end, the mill is hitting its design throughput, proving the project can deliver on its promise of high-grade, low-cost output.

- Copper Price Resilience: Global copper prices are trending toward $12,000/mt due to severe supply disruptions at major global mines (like Grasberg). Ero is one of the few producers actually increasing supply into this deficit.

- The "Gold Bonus": On December 19, 2025, Ero filed a Technical Report for its Xavantina Operations, confirming a high-grade gold concentrate stockpile. Sales of this "hidden" asset began in Q4 2025, providing a significant cash flow injection.

- Institutional FOMO: Following a series of "Hold" to "Outperform" upgrades (notably Scotiabank), institutional investors are rotating into Ero as a pure-play copper growth story with a strengthening balance sheet.

Latest Business Model: The "Growth & Optimization" Strategy

Ero Copper operates primarily in Brazil, utilizing a unique business model focused on three core pillars:

- High-Grade Base: Managing the long-life Caraíba Operations (Pilar and Vermelhos mines), which provide steady, high-grade copper.

- Low-Cost Expansion: The Tucumã Project is the crown jewel, operating as an open-pit mine with C1 cash costs significantly lower than the industry average ($1.05–$1.25/lb guidance).

- Precious Metal Synergy: Leveraging the Xavantina Operations for gold production to offset copper costs, effectively acting as a natural hedge and margin booster.

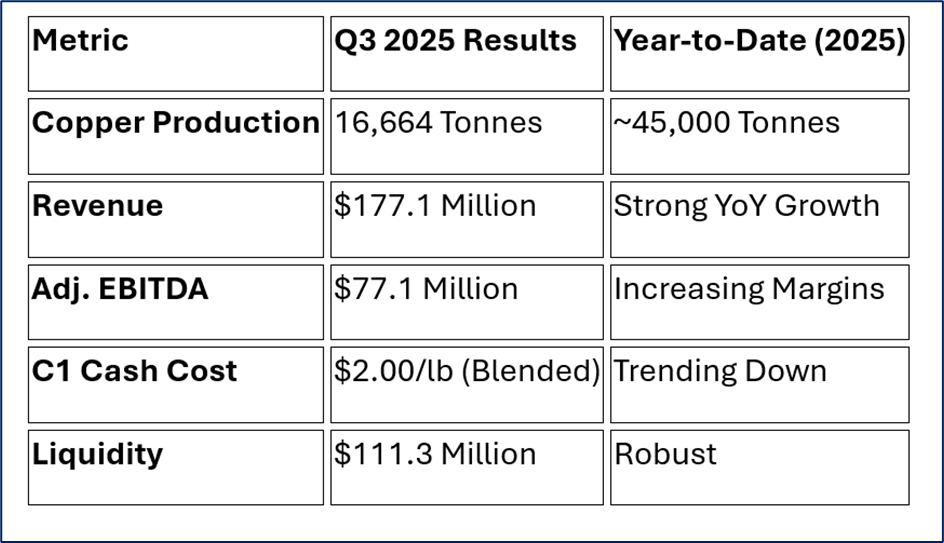

Financial and Operational Performance (Latest Update)

Source: Company Data

Operational Highlights:

- Caraíba: Record plant throughput of nearly 1.0 million tonnes in Q3.

- Xavantina: Transitioned to mechanized mining, increasing gold production by 17% quarter-over-quarter.

- Furnas Project: Deep drilling has intercepted massive copper-gold mineralization, hinting at the next major growth phase beyond 2027.

SWOT Analysis

Source: Kalkine Group

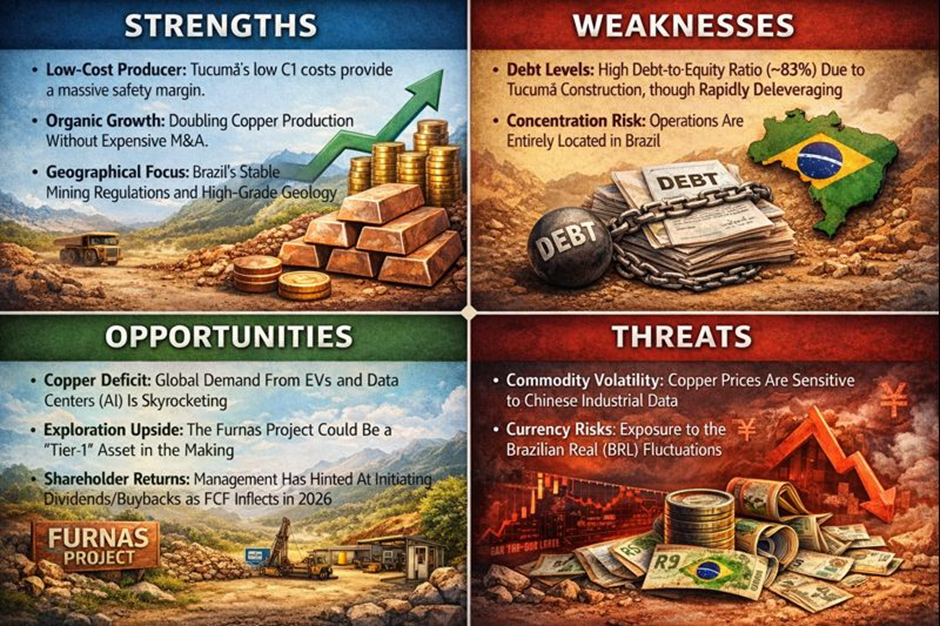

Strengths

- Low-Cost Producer: Tucumã’s low C1 costs provide a massive safety margin.

- Organic Growth: Doubling copper production without expensive M&A.

- Geographical Focus: Brazil’s stable mining regulations and high-grade geology.

Weaknesses

- Debt Levels: High debt-to-equity ratio (~83%) due to Tucumã construction, though rapidly deleveraging.

- Concentration Risk: Operations are entirely located in Brazil.

Opportunities

- Copper Deficit: Global demand from EVs and Data Centers (AI) is skyrocketing.

- Exploration Upside: The Furnas Project could be a "Tier-1" asset in the making.

- Shareholder Returns: Management has hinted at initiating dividends/buybacks as FCF inflects in 2026.

Threats

- Commodity Volatility: Copper prices are sensitive to Chinese industrial data.

- Currency Risks: Exposure to the Brazilian Real (BRL) fluctuations.

Risks to Watch

While the stock is at an all-time high, retail investors should monitor:

- Execution Risk: Any bottlenecks in the final stages of the Tucumã ramp-up.

- Cost Inflation: Rising energy and labor costs in Brazil could squeeze margins.

- Technical Overbought Signals: With a 111% annual return, the stock may see short-term profit-taking.

Conclusion

Ero Copper's performance on December 30, 2025, reflects a company hitting its stride. By successfully transitioning from a "developer" to a "multi-asset producer," Ero has captured the market's imagination. With Tucumã reaching full throttle and gold sales adding a sweet kicker to the bottom line, the company is fundamentally different—and stronger—than it was a year ago.

Please wait processing your request...

Please wait processing your request...