The North Star Trade: Why Smart Money is Rotating into Canadian Value Giants

As the global equity rally faces exhaustion in early 2026, the world’s most sophisticated institutional players—from J.P. Morgan to National Bank Financial—are pivoting toward the "safety of value" within the TSX. While the S&P 500 grapples with premium multiples, the Canadian Large Cap landscape offers a rare intersection of high dividend yields and massive intrinsic discounts.

The following selection represents the top consensus picks from the latest January 2026 analyst briefings and institutional flow data, identifying companies where the business model resilience significantly outstrips the current share price.

Source: Kalkine Group

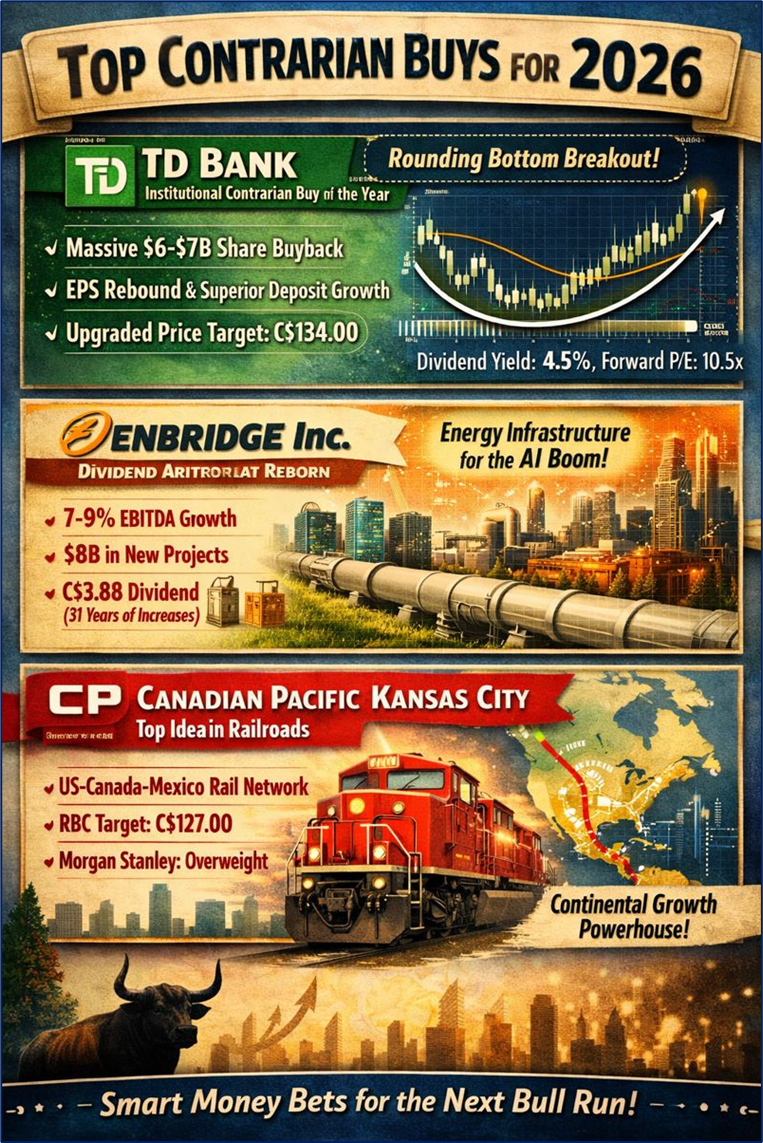

Toronto-Dominion Bank (TSX: TD): The Institutional "Contrarian Buy" of the Year

The Bull Case and Strategic Drivers

Toronto-Dominion Bank has emerged as a top pick for 2026 as it successfully navigates the tail-end of its regulatory remediation in the United States. Global fund managers are betting on TD due to its "lower bar" in Capital Markets, which sets the stage for significant earnings per share (EPS) revisions. A key driver is the bank’s superior deposit growth and retail loan expansion, which outperformed peer averages throughout 2025. Smart money is particularly focused on TD’s massive $6–$7 billion share buyback program, which acts as a powerful floor for the stock price during market volatility.

Current Technical Analysis

Technically, TD is exhibiting a classic "rounding bottom" formation on the weekly charts. After a period of underperformance relative to the Big Five, the stock has recently pierced its 200-day simple moving average (SMA). Momentum oscillators like the RSI are trending upward toward the 60-level, suggesting that the "washout" phase is over and institutional accumulation has begun.

Latest Analyst Ratings and Business Model Updates

- National Bank Financial: Upgraded from Sector Perform to Outperform (Dec 18, 2025).

- Price Target Hike: Increased to C$134.00 from C$124.00.

- Business Model: TD continues to operate a highly diversified retail-focused model, with approximately 55% of earnings coming from Canadian P&C banking and a growing footprint in the U.S. wealth management sector.

Valuation and Dividends

- Latest Dividend: Current annualized dividend of C$4.08, yielding approximately 4.5%–4.8% based on recent price action.

- Valuation: Trading at a Forward P/E of roughly 10.5x, a notable discount to its 5-year historical average of 12.2x.

Outlook and Risks

The outlook for 2026 remains bullish as the bank realizes cost synergies from its internal restructuring. However, risks include potential "macro headwinds" in the Canadian housing market if interest rates remain "higher for longer," alongside the ongoing oversight costs related to U.S. anti-money laundering compliance.

Enbridge Inc. (TSX: ENB): The Dividend Aristocrat Reborn as a Growth Engine

Key Reasons for the Smart Money Surge

Enbridge is no longer just a "yield play"; it is being re-rated by investment banks as a critical infrastructure backbone for the AI-driven energy surge. Analysts from Simply Wall St and major Canadian brokers highlight Enbridge’s 2026 guidance as a turning point. The company has reaffirmed a 7%–9% EBITDA growth rate through 2026, supported by $8 billion in new projects entering service this year. Hedge funds are drawn to the fact that 98% of Enbridge’s cash flow is backed by long-term, inflation-linked contracts or regulated cost-of-service frameworks.

Current Technical Analysis

Enbridge’s stock is currently testing a multi-year resistance zone near the C$58 mark. High-volume breakouts in early January suggest that the "yield-trap" narrative is being replaced by "growth-at-a-reasonable-price" (GARP). The stock remains in a strong ascending channel, with support firmly established at the C$53 level.

Latest Analyst Upgrades and Operational Updates

- Consensus Rating: Maintains a Moderate Buy with a fair value estimate reaching as high as C$71.12 (Simply Wall St analysis, Jan 2026).

- Operational Milestone: Successfully integrated recent U.S. gas utility acquisitions, making Enbridge the largest natural gas utility franchise in North America.

- Guidance: 2026 Adjusted EBITDA projected at $20.2 billion to $20.8 billion.

Latest Dividend and Valuation

- Dividend Increase: Announced a 3% hike to C$3.88 annualized (C$0.97 quarterly) effective March 1, 2026. This marks 31 consecutive years of increases.

- Valuation: Currently trading at a discount of approximately 13% to 15% relative to its estimated intrinsic cash-flow value.

Outlook and Risks

The outlook is bolstered by the rising demand for natural gas to power AI data centers. The primary risk remains the company’s elevated leverage (Debt-to-EBITDA of 4.5x–5.0x), which requires disciplined capital allocation to maintain its "BBB+" credit rating.

Canadian Pacific Kansas City (TSX: CP): The "Top Idea in Railroads" for the USMCA Era

The Drivers: Continental Synergy and AI Efficiency

Canadian Pacific Kansas City (CPKC) is the "top idea" for RBC Capital and Morgan Stanley in the transportation sector. As the only single-line rail network connecting Canada, the U.S., and Mexico, CPKC is uniquely positioned to benefit from the "near-shoring" trend in manufacturing. Global fund managers are aggressively eyeing the company's "meaningful EPS outperformance" expected in the latter half of 2026 as the integration of Kansas City Southern reaches full maturity.

Current Technical Analysis

The stock has recently faced a "healthy consolidation" after a downgrade to "Hold" by National Bank, which cited short-term valuation peaks. However, technical indicators show the stock is finding strong support at its 200-day moving average of $75.05. For long-term investors, the current price represents a "buy-the-dip" opportunity before the next leg of the USMCA trade cycle begins.

Latest Analyst Actions and Business Model

- RBC Capital: Reiterated Outperform rating (Jan 9, 2026) with a C$127.00 price target.

- Morgan Stanley: Upgraded to Overweight with a target of C$120.00.

- Business Model: A high-margin, wide-moat precision scheduled railroading (PSR) model with exclusive access to the Mexican industrial heartland.

Valuation and Operational Performance

- Latest Valuation: Trading at a P/E ratio of 21.8x, which analysts argue is "undervalued" when factoring in the unique triple-country growth trajectory (PEG ratio of 1.58).

- Dividend: Maintains a stable, albeit lower-yielding, dividend as management prioritizes debt reduction following the merger.

Outlook and Risks

The long-term outlook is exceptionally strong due to sector consolidation and the company’s role in green logistics. Key risks include broader "macro headwinds" in the first half of 2026 and potential regulatory hurdles regarding further industry consolidation involving rivals like Union Pacific.

Conclusion: The 2026 Value Reversal

The convergence of institutional "smart money" into TD, ENB, and CPKC signals a shift away from speculative tech and toward durable, cash-flow-rich Canadian giants. These stocks currently offer a rare combination of dividend growth, monopolistic market positions, and double-digit valuation discounts. For the retail investor, the 2026 TSX landscape is less about finding the next "moonshot" and more about securing ownership in the essential engines of the North American economy at a discount.

Please wait processing your request...

Please wait processing your request...