On December 31, 2025, Gatekeeper Systems Inc. (TSXV: GSI) saw its stock climb approximately 3.4%, a notable year-end nudge that has retail investors asking: Is this the momentum trade for 2026?

While the broader markets were winding down, Gatekeeper’s uptick was fueled by a confluence of massive contract wins, a strategic pivot toward recurring revenue, and a fortified balance sheet. Here is the deep-dive analysis of why GSI is moving and what the 2026 roadmap looks like.

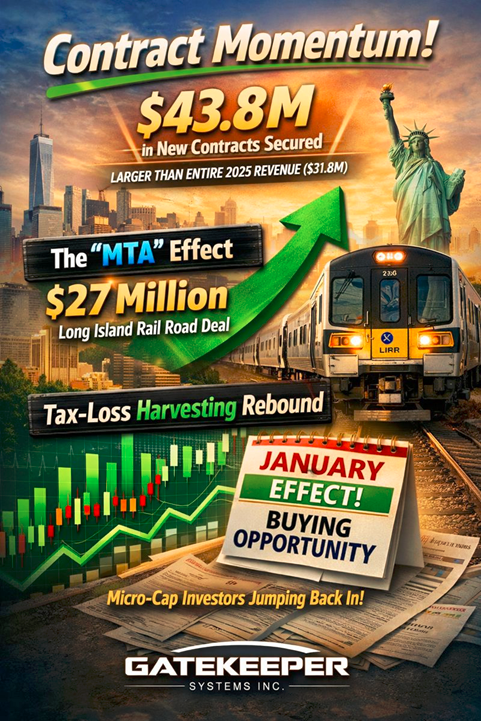

The Dec 31 Catalyst: Why the 3.4% Green Close?

Source: Kalkine Group

The year-end surge wasn't a fluke; it was a delayed reaction to the Fiscal 2025 Audited Results released just 48 hours prior (December 29).

- Contract Momentum: Investors reacted to the announcement of $43.8 million in new contracts secured just after the fiscal year-end. To put that in perspective, that single "subsequent" backlog is larger than their entire 2025 revenue ($31.8M).

- The "MTA" Effect: A massive $27 million contract with New York’s Long Island Rail Road (MTA) validated Gatekeeper as a top-tier player capable of handling the largest transit agencies in North America.

- Tax-Loss Harvesting Rebound: As a micro-cap, GSI likely saw buying pressure from investors positioning for the "January Effect," picking up shares after others finished year-end tax selling.

Latest Business Model: From Hardware Vendor to Data Giant

Gatekeeper has undergone a fundamental transformation. They are no longer just "the camera company."

- Platform-as-a-Service (PaaS): The core is the Mobile Data Collector (MDC). They have over 65,000 MDCs installed, which act as the "brain" of the bus or train.

- AI & Video Analytics: Using AI to detect stop-arm violations (cars passing school buses) and driver distractions (cell phone use).

- The Subscription Pivot: Gatekeeper launched its own Data Center in early 2024. They’ve already converted 4,000 MDCs to recurring hosted service subscriptions—a high-margin revenue stream that creates "sticky" customer relationships.

2026 SWOT Analysis: The Strategic Outlook

Source: Kalkine Group

Latest Financial & Operational Updates

Based on the December 2025 filings, the numbers tell a story of "Investing for Scale":

- Revenue (FY2025): $31.8 Million. While lower than the $37.8M in 2024 (which included a one-time $9M outlier), the "regular" business actually grew 10%.

- Backlog: The company is entering 2026 with a record-breaking sales funnel, specifically in the school bus and passenger rail segments.

- Expansion: They’ve added security veteran Hamish Dobson to the board, signaling a move toward more sophisticated AI and cybersecurity integrations.

Key Risk Factors to Watch

- The Profitability Gap: The company reported a comprehensive loss of $3.0 million for fiscal 2025. Investors are waiting to see if the massive new contract wins will finally tip the scales back to net income in 2026.

- Execution Risk: Managing a $27M contract for a body like the New York MTA is complex. Any delays in deployment could impact stock sentiment.

- Regulatory Timeline: Much of the "Opportunity" hinges on government mandates. If federal deadlines for transit safety tech are pushed back, growth could stall.

Analytical Conclusion

Gatekeeper Systems is currently in a "coiled spring" phase. They have spent 2025 spending money to build the infrastructure (Sales, Data Centers, Engineering) to catch whales. The $43.8 million in recent wins suggests the whales are biting.

The 3.4% move on Dec 31 reflects a market starting to realize that GSI’s 2026 revenue profile could look radically different—and significantly larger—than its 2025 performance.

Please wait processing your request...

Please wait processing your request...