Generating a steady CAD 1,000 monthly (CAD 12,000 annually) in passive income is a cornerstone of Canadian "FIRE" (Financial Independence, Retire Early) strategies. In 2026, as the market shifts from "growth-at-all-costs" to a focus on durable cash flows, Canadian dividend stocks remain a premier vehicle for this goal.

Here is the blueprint for building a $12,000 annual income stream, backed by 2026 market data and insights from leading financial institutions like J.P. Morgan and RBC Wealth Management.

The Golden Number: How Much Do You Need to Invest?

The "price" of your second income depends entirely on the Average Dividend Yield of your portfolio. According to RBC Wealth Management's 2026 Outlook, the S&P/TSX continues to trade at a more attractive valuation multiple (15.9x) compared to the S&P 500 (21.3x), offering a higher baseline for yield-seekers.

Source: Kalkine Group Analysis

While a 6% yield requires less capital, J.P. Morgan notes that in a 2026 environment of "higher-for-longer" inflation, quality and dividend coverage are paramount. A diversified blend targeting a 5% yield is often considered the safest path to avoid "yield traps."

Top Canadian Dividend Stocks for 2026

Leading analysts highlight three sectors that dominate the Canadian landscape: Energy Infrastructure, Financials, and Utilities.

Source: Kalkine Group

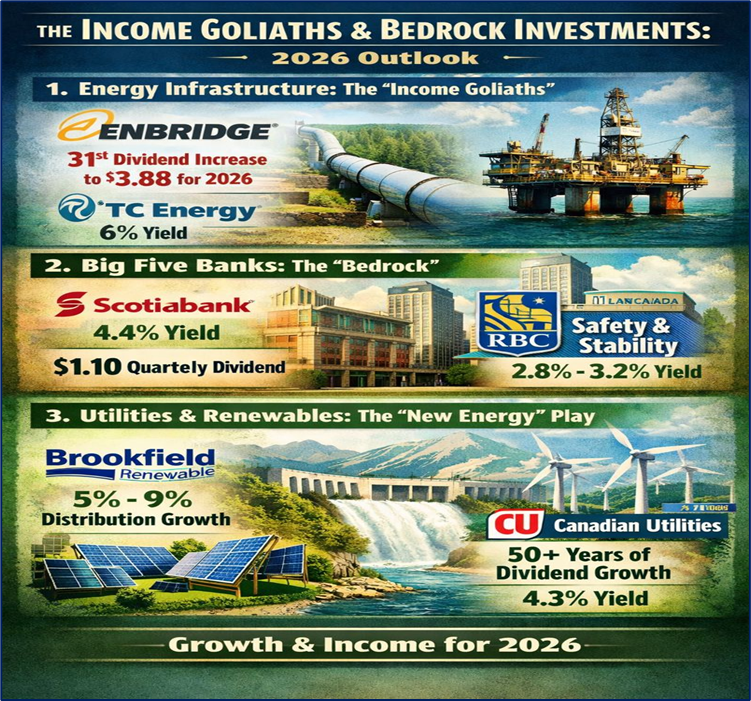

- The "Income Goliaths": Energy Infrastructure

- Enbridge (TSX: ENB): A perennial favorite. In December 2025, Enbridge announced its 31st consecutive annual dividend increase, raising the payout by 3% to $3.88 per share for 2026. With a yield typically near 6%, it is a staple for cash-flow stability.

- TC Energy (TSX: TRP): Heading into 2026, TC Energy maintains a robust yield of approximately 4.6% to 5%. Its recent focus on asset-spinning has strengthened the balance sheet, supporting its status as a reliable income producer.

- The "Bedrock": Big Five Banks

- Bank of Nova Scotia (TSX: BNS): Currently yielding roughly 4.4%, Scotiabank remains the "high-yield" play among the big banks. Its 2026 strategy focuses on optimizing capital in the Americas, which supports its steady quarterly payout of $1.10 per share.

- Royal Bank of Canada (TSX: RY): The "safety first" choice. While the yield is traditionally lower (around 2.8% to 3.2%), its dividend growth remains a benchmark for North American financials.

- The "New Energy" Play: Utilities & Renewables

- Brookfield Renewable Partners (TSX: BEP.UN): As noted in Brookfield’s 2026 Investment Outlook, the global surge in AI data centres has created a massive tailwind. BEP targets annual distribution growth of 5% to 9%, making it a rare "growth-and-income" hybrid.

- Canadian Utilities (TSX: CU): Canada's first "Dividend King" with over 50 years of increases. Yielding approximately 4.3% in early 2026, it is the ultimate "sleep-well-at-night" (SWAN) stock.

Strategy: The "Monthly Calendar" Hack

Most Canadian stocks pay quarterly. To get CAD 1,000 every month, professional investors use a "staggered" portfolio:

- Month A (Jan/Apr/Jul/Oct): Scotiabank (BNS), Telus (T).

- Month B (Feb/May/Aug/Nov): Enbridge (ENB), Royal Bank (RY).

- Month C (Mar/Jun/Sep/Dec): Fortis (FTS), Canadian Utilities (CU).

Alternatively, investors often opt for the iShares S&P/TSX Canadian Dividend Aristocrats ETF (TSX: CDZ). It pays out monthly (roughly $0.11–$0.13 per unit in recent 2025/2026 periods) and handles the diversification for you.

The 2026 Tax Advantage: The "Dividend Tax Credit"

Unlike interest from GICs or rental income (taxed as regular income), eligible dividends from Canadian corporations receive the Dividend Tax Credit.

For a resident in a middle-income bracket, $12,000 in dividends is taxed at a significantly lower effective rate than $12,000 in salary or interest. This "tax alpha" means you keep more of your $1,000 every month compared to almost any other secondary income stream.

Please wait processing your request...

Please wait processing your request...