The Canadian consumer lending giant goeasy Ltd. (TSX: GSY) saw its shares edge up by 0.58% to close at CAD 131.25 on December 24, 2025. While the gain might seem modest, it represents a critical stabilization for a stock that has navigated a turbulent fourth quarter, marked by leadership changes and a challenging credit environment.

Key Drivers: Why the Needle Moved on Christmas Eve

The upward nudge on December 24 was driven by a combination of technical milestones and strategic corporate actions:

Source: Kalkine Group

- The "Ex-Dividend" Magnet: December 24 was the ex-dividend date for goeasy’s quarterly dividend of $1.46 per share. Investors often buy in just before this date to capture the payout, providing a natural floor for the stock price.

- Share Buyback Confidence: On December 19, the TSX approved the renewal of goeasy's Normal Course Issuer Bid (NCIB). This allows the company to repurchase up to 1.2 million shares (roughly 10% of its float). The program officially commenced on December 23, 2025, signaling to the market that management believes the current price is undervalued.

- Leadership Handover: With CEO Dan Rees stepping down at year-end, the market is beginning to price in the transition to Patrick Ens, the incoming CEO effective January 1, 2026. Ens’s deep experience as President of easyfinancial provides a sense of continuity that is calming nervous retail investors.

Latest Business Model: The "Non-Prime" Powerhouse

In 2025, goeasy has aggressively shifted from a simple lender to a sophisticated, data-driven financial ecosystem.

- The Omnichannel Strategy

Goeasy operates a seamless hybrid model combining over 400 physical locations with a robust digital platform. In 2025, digital loan originations reached record levels, fueled by a 22% surge in applications.

- The Shift to "Secured" Lending

The most significant evolution in the 2025 business model is the pivot toward secured loans (Auto and Home Equity).

- Secured loans now represent approximately 48% of the total portfolio.

- This shift lowers the risk of defaults (charge-offs) and provides a "graduation" path for customers to eventually reach prime lending rates.

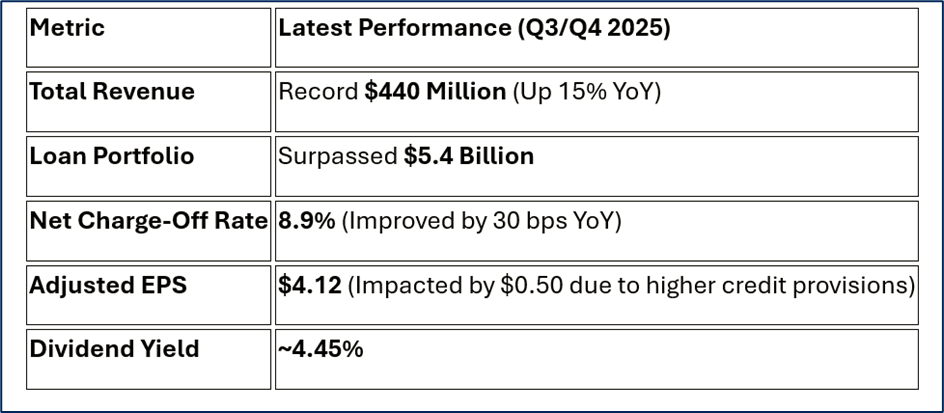

Financial & Operational Update: The Q3/Q4 Snapshot

Despite a "miss" in Q3 earnings that saw the stock dip earlier in the fall, the underlying operational metrics remain massive:

Source: Company Data

The company has successfully renewed its $1.4 billion securitization facility, ensuring it has the "dry powder" (liquidity) to fund growth through 2026.

SWOT Analysis: A Reality Check

Source: Kalkine Group

Strengths

- Dominant Market Position: 9.6 million Canadians fall into the "non-prime" category; goeasy is their first choice.

- Proprietary AI Scoring: Their machine-learning models are reportedly 200% more predictive than traditional credit bureau scores.

- Dividend Aristocrat Status: 21 consecutive years of payments and 11 years of double-digit increases.

Weaknesses

- Debt-to-Equity Ratio: High leverage (approx. 381%) makes the company sensitive to interest rate volatility.

- Earnings Volatility: Recent misses show that even record revenue can be offset by a sudden need for higher "provisions for credit losses."

Opportunities

- Market Share Gains: As traditional banks tighten lending standards in a cooling economy, goeasy captures the spillover.

- Acquisition Potential: Their strong liquidity position makes them a prime candidate to acquire smaller fintech competitors.

Threats

- Regulatory Caps: Any further federal changes to the criminal rate of interest (interest rate caps) could squeeze profit margins.

- Economic Cooling: Rising unemployment in Canada could lead to higher default rates among their core customer base.

The Risk Landscape

Investors should remain focused on Credit Quality. While the charge-off rate improved to 8.9%, the company increased its "Allowance for Credit Losses" from 7.9% to 8.1% in late 2025. This suggests management is bracing for a slightly bumpier road in early 2026 as Canadian consumers grapple with high household debt.

Conclusion

Goeasy’s performance on December 24 reflects a stock in transition. While the company is delivering record-breaking revenue and loan growth, the market is carefully weighing these gains against a shifting leadership team and a cautious economic outlook. The combination of a healthy 4.4% dividend and an active share buyback program provides a strong incentive for long-term "hold" strategies, even as the stock trades nearly 60% below some analysts' fair value estimates.

Please wait processing your request...

Please wait processing your request...