Can Superior Plus’s blend of propane, natural gas, and renewable fuels deliver dependable income and long-term growth for investors in 2026 and beyond?

Key Takeaways — February 2026 Snapshot

- Superior Plus Corp (TSX: SPB) rose ~2.3% on Feb 5, 2026, extending near-term positive momentum.

- Dividend appeal remains intact, supported by stable cash flows and a monthly payout.

- Analyst consensus: Moderate Buy, with ~26% upside implied by average price targets.

- Macro forces—Canada’s economy, TSX Composite volatility, and CAD trends—continue to shape near-term moves.

- Medium-to-long term thesis hinges on execution: efficiency gains, renewable fuel expansion (RNG, hydrogen), and sector rotation.

Why Is Superior Plus Stock Moving Higher in February 2026?

Investors tracking SPB are reacting to a mix of income stability and energy infrastructure relevance. As a distributor spanning propane, compressed natural gas (CNG), renewable natural gas (RNG), and hydrogen services across Canada and the U.S., Superior Plus sits at the intersection of defensive utility demand and energy transition themes.

In early 2026, sentiment toward energy distribution and infrastructure has improved as markets reassess:

- predictable cash generation,

- resilience during economic slowdowns,

- and optional upside from cleaner-fuel investments.

That blend helps explain renewed interest and the recent price uptick.

Canada’s Economy, the TSX Composite, and What They Mean for SPB

Is the macro backdrop supportive for dividend-paying energy distributors?

Broadly, yes—with caveats.

Canada’s GDP trajectory, capital spending, and central-bank policy ripple through the TSX Composite, influencing utility and energy names like Superior Plus.

Key Macro Drivers in Early 2026

- Interest rates & inflation expectations: Higher-for-longer or stabilizing rates tend to favor income stocks with visible cash flows.

- Energy demand trends: A steady recovery in industrial and commercial activity supports propane and gas distribution volumes.

- Canadian dollar (CAD): Currency strength affects cost structures, cross-border earnings, and asset valuations.

When volatility rises, yield-oriented names often regain appeal—positioning SPB as a potential defensive allocation.

How Does Superior Plus Compare With Canadian Peers?

Against other Canadian utility and energy distribution names:

- Valuation: SPB often trades at a premium to some peers due to its diversified footprint and growth optionality.

- Income: Monthly dividends translate to a yield around ~2.5%, appealing to cash-flow-focused investors.

- Growth narrative: Exposure to RNG and hydrogen provides a longer-term angle that many traditional utilities lack.

Peers such as AltaGas and ATCO offer competition, but analysts generally see Superior Plus as slightly better positioned for blended income + growth—albeit with earnings variability tied to sector cycles.

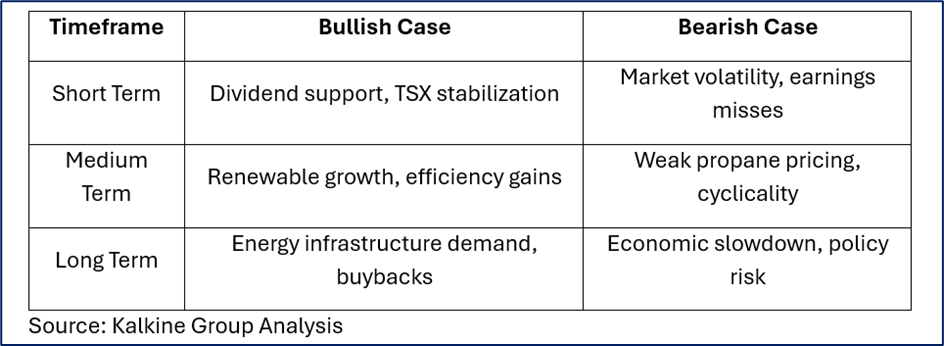

Technical & Fundamental Outlook: Short, Medium, and Long Term

Short Term (3–6 months): Neutral → Modestly Bullish

- Upside: Dividend reliability, seasonal energy demand.

- Risks: TSX volatility, earnings-related surprises.

Medium Term (6–18 months): Cautiously Bullish

- Upside: Operational efficiencies, selective buybacks, scaling renewable segments.

- Risks: Commodity pricing swings, propane margin pressure.

Long Term (2+ years): Neutral to Moderately Bullish

- Upside: Structural demand for energy distribution, cleaner-fuel transition.

- Risks: Policy shifts, execution missteps, macro downturns.

Overall, the trajectory improves if management executes and sector rotation favors infrastructure and income assets.

Dividends, Cash Flow, and Business Updates

- Dividend policy: Monthly payout of CAD $0.045 has remained stable through 2025 and into 2026.

- Earnings focus: Q4 2025 and full-year results (Feb 2026) are key near-term catalysts.

- Strategic priorities: Cost discipline, balance-sheet optimization, and expansion in RNG and hydrogen to support medium-term growth.

Dividend sustainability remains a central pillar of the investment case.

Bull vs. Bear Scenarios for Superior Plus

This framework highlights how outcomes can diverge depending on execution and macro conditions.

Analyst Sentiment & Price Targets

- Consensus: Moderate Buy

- 12-month outlook: Price targets imply meaningful upside, though estimates vary widely.

- Interpretation: Analysts are constructive on income stability and longer-term growth, but cautious about timing and sector risks.

Key Risks Investors Should Watch

- Energy and commodity price volatility.

- Cyclical demand in propane and natural gas.

- Economic slowdowns reducing commercial consumption.

- Pressure on dividend coverage if margins compress.

Balancing these risks against income stability is crucial for long-term holders.

FAQ — Superior Plus Stock (SEO-Optimized)

Q: Is Superior Plus stock rising in February 2026?

A: Yes, SPB has shown recent gains, supported by dividend appeal and sector dynamics.

Q: What is Superior Plus’s dividend yield?

A: Roughly ~2.5%, paid monthly.

Q: Do analysts expect SPB to rise further?

A: Consensus remains Moderate Buy, with upside potential over 12 months.

Q: How does Canada’s economy impact SPB?

A: Stronger growth and energy demand help; slower growth can weigh on sentiment but may boost demand for defensive income stocks.

Bottom Line: Is Superior Plus Worth Owning in 2026?

Superior Plus offers a hybrid investment case in 2026: dependable monthly income paired with selective growth from renewable fuels and infrastructure services. While short-term moves may track broader market swings, the medium-to-long term story depends on execution, efficiency gains, and the pace of the energy transition.

For investors seeking steady dividends with moderate upside, SPB remains a name worth watching closely in the Canadian energy landscape.

Informational analysis only. Not investment advice.

Please wait processing your request...

Please wait processing your request...