Kelt Exploration Ltd. (TSX: KEL) caught the eye of value hunters on December 29, 2025, closing up 1.72% at CAD 7.67. While the broader TSX index struggled in negative territory, Kelt rode a wave of sector-wide strength and company-specific milestones.

With the highly anticipated Albright Gas Plant finally operational and a massive debt-reduction plan nearing completion, investors are asking: Is this the start of a sustained bull run, or just a year-end relief rally?

The Spark: Why Kelt Outperformed the TSX Today

Kelt’s gain was driven by a "perfect storm" of macro energy tailwinds and localized operational wins:

Source: Kalkine Group

- Firming Crude Prices: WTI Crude oil futures jumped over 2.5% to $58.21/bbl today, buoyed by geopolitical tensions and supply-side constraints.

- The "Albright Effect": Recent confirmation that the Albright Sulphur Recovery Gas Plant is now processing volumes has alleviated fears of further infrastructure delays.

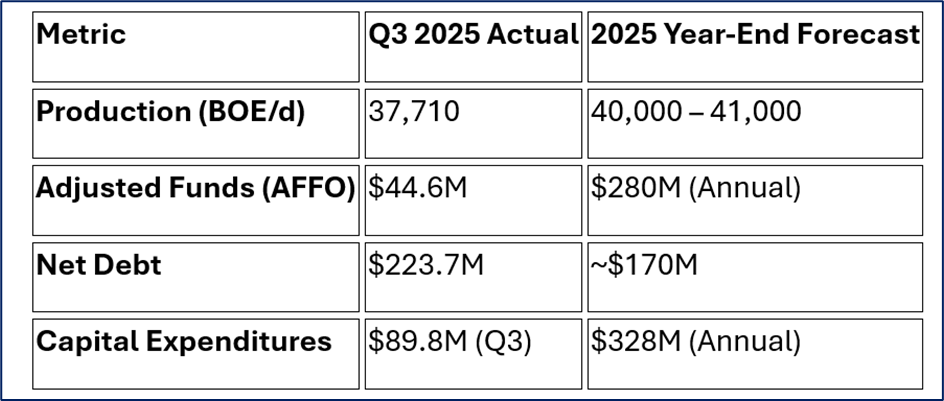

- Year-End Deleveraging: Investors are responding to management’s guidance to slash net debt from $223.7 million (Q3) to approximately $170 million by year-end.

- Analyst Upgrades: Positive momentum from a recent Roth MKM "Buy" rating and a price target of $7.97 continues to provide a floor for the stock.

Latest Business Model: The Montney Pure-Play

Kelt has sharpened its focus as a high-growth, Western Canadian Sedimentary Basin (WCSB) operator. Its business model relies on a low-cost, high-impact asset base:

- Concentrated Core Areas: Operations are focused on the Wembley/Pipestone (Alberta) and Oak/Flatrock (B.C.) regions, known for high-liquids Montney and Charlie Lake play types.

- Infrastructure-Led Growth: Instead of relying solely on third parties, Kelt strategically invests in midstream (like the Albright plant) to control its own destiny and lower operating costs.

- Liquids Focus: While a major gas producer, Kelt aggressively targets "fat" gas areas to maximize condensate and NGL yields, which command higher margins than dry gas.

Financial & Operational Update: Q4 2025 Momentum

Kelt’s most recent data shows a company in transition from a heavy spending phase to a production harvest phase.

Source: Company Data

Operational Milestone: The Q4 2025 startup of the Albright plant is the game-changer. It unlocks shut-in production and provides the capacity needed for Kelt to target 45,000+ BOE/d in early 2026.

SWOT Analysis: The Retail Reality

Source: Kalkine Group

Strengths

- Top-Tier Assets: Inventory in the Montney and Charlie Lake ranks among the most economic in North America.

- Operational Control: The newly commissioned Albright plant removes a massive bottleneck.

- Strong Balance Sheet: A projected Net Debt/AFFO ratio of 0.6x is highly conservative.

Weaknesses

- Historical Volatility: Delays in third-party infrastructure (like the Albright plant) have previously frustrated shareholders.

- Price Sensitivity: High exposure to AECO gas pricing, which has seen significant localized pressure.

Opportunities

- 2026 Production Surge: With infrastructure in place, 2026 is set to be a "harvest year" for cash flow.

- M&A Target: Given its clean balance sheet and prime land, Kelt remains a perennial takeover candidate for larger E&Ps.

Threats

- Political/Regulatory Shifts: Ongoing environmental regulations in British Columbia and Alberta remain a constant "wildcard."

- Commodity Price Slumps: A global economic slowdown could cap WTI and AECO upside.

Key Risks to Watch

- AECO Volatility: If Western Canadian gas prices remain depressed due to oversupply or storage levels, Kelt may be forced to shut in dry gas production again.

- Execution Risk: While the Albright plant is up, ramp-up phases can often hit mechanical snags.

- Interest Rates: While debt is falling, any pivot in central bank policy could affect the cost of future capital programs.

Conclusion: A 2026 Dark Horse?

Kelt Exploration’s 1.72% gain on December 29th isn't just noise; it’s a reflection of a company that has finally cleared its biggest hurdle. With the Albright plant online, the "story" for Kelt in 2026 shifts from construction to cash flow. For retail investors, the stock remains a high-beta play on Canadian energy—volatile, but fundamentally underpinned by a world-class asset base and a rapidly improving balance sheet.

Please wait processing your request...

Please wait processing your request...