While the broader markets often wind down before the holidays, Pet Valu Holdings Ltd. (TSX: PET) gave investors a small reason to cheer on December 24, 2025. The stock edged up 0.61%, closing at CAD 28.00. Though the gain seems modest, it follows a period of intense volatility and signals a potential "value floor" for the Canadian pet giant.

Below is a deep dive into the drivers, the latest business model shifts, and why the "humanization of pets" remains a recession-resistant engine for this company.

Key Drivers: Why the Green Day?

The 0.61% uptick on Christmas Eve wasn't just holiday spirit; it was driven by a combination of tactical positioning and operational stability:

Source: Kalkine Group

- Value Rotation: As 2026 approached, institutional investors began rotating capital into "Value" stocks with strong cash flows. With a P/E ratio around 20.4x (well below the sector average), PET looked like a bargain.

- The "Holiday Treat" Effect: Historically, pet spending spikes in late December. Recent partnerships with Uber Eats and DoorDash have streamlined last-minute gifting, a key revenue driver for the Q4 period.

- Supply Chain Confidence: The recent completion of the $110 million supply chain transformation (including the massive Calgary distribution center) is finally shifting the narrative from "heavy spending" to "efficiency gains."

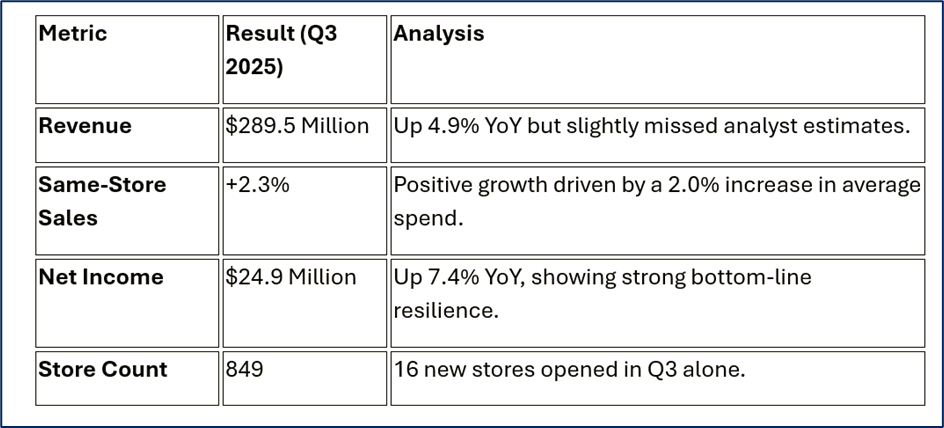

Financial & Operational Update: The Q3 Reality Check

Pet Valu's recent Q3 2025 results were a mixed bag that actually helped set the stage for the current stock price.

Source: Company Data

The Silver Lining: Despite a downward revision in full-year guidance to $1.175B – $1.185B, management’s focus on free cash flow is gaining traction. Analysts expect free cash flow to jump significantly in 2026 as the heavy lifting of warehouse automation concludes.

The "New" Business Model: More Than Just Kibble

Pet Valu is aggressively moving away from being a "commodity" retailer to a "specialty experience" hub.

- Culinary Focus: The company has rolled out a new store layout focused on premium and fresh pet food. 120 stores now feature "enhanced culinary" sections.

- Service Integration: By offering self-serve dog washes and full-service grooming in more locations (currently 22% of stores offer both), Pet Valu creates "sticky" customers who can't get those services from Amazon.

- The "ACE" Advantage: Their "Animal Care Experts" (ACEs) provide localized, expert advice—a primary differentiator against big-box competitors like Walmart.

SWOT Analysis

Source: Kalkine Group

Strengths

- Dominant Canadian Footprint: Largest specialty pet retailer in Canada with 849+ locations.

- Franchise-Heavy Model: High-margin franchise fees provide stable recurring revenue.

- Private Label Success: Brands like Performatrin offer higher margins than national brands.

Weaknesses

- Debt Obligations: Significant debt from recent infrastructure investments.

- Margin Compression: Higher SG&A costs (SaaS fees and compensation) have pressured EBITDA margins to ~22%.

Opportunities

- E-commerce Expansion: Growth in loyalty programs and digital delivery partnerships.

- Store Expansion: Management sees a long-term path to 1,200+ locations in Canada.

- Premiumization: Owners continue to spend on high-quality, "human-grade" food despite inflation.

Threats

- Consumer Frugality: If the Canadian economy softens further in 2026, "discretionary" pet toys may suffer.

- Intense Competition: Pressure from Petco, PetSmart, and digital-first players like Chewy.

Key Risks to Watch

- Execution Risk: The success of 2026 depends entirely on the new automated distribution centers delivering the promised 30% jump in free cash flow.

- The "53rd Week" Complication: 2025 is a 53-week fiscal year. Investors must be careful not to mistake the extra week of revenue for permanent organic growth.

- Interest Rates: As a company with notable leverage, sustained high interest rates could impact net income margins.

Conclusion: The "Loyal Companion" Portfolio Play

Pet Valu's 0.61% rise on December 24 reflects a market that is starting to forgive the company for its guidance miss earlier in the quarter. With a consensus "Buy" rating and a price target near $38.56, PET is currently trading at a significant discount to its perceived intrinsic value.

The story for 2026 isn't just about selling dog food; it’s about whether Pet Valu can turn its massive new infrastructure into a cash-generating machine. For now, the "humanization of pets" trend remains the company's strongest tailwind.

Please wait processing your request...

Please wait processing your request...