While most of the market was settling into the holiday break, Blackrock Silver (TSXV: BRC) was lighting up the boards. On December 24, 2025, the stock surged roughly 7.4%, closing at a fresh 52-week high of CAD 1.30.

This wasn't just holiday cheer; it was a perfect storm of a massive capital injection, record-breaking silver prices, and "bonanza" grade drill results. Here is the analytical breakdown of what’s driving this Nevada-focused explorer.

The Christmas Eve Catalyst: C$15M Strategic Inflow

Source: Kalkine Group

The primary driver for the Dec 24 move was the announcement of a C$15 million strategic private placement.

- Cornerstone Backing: The financing is being led by two major "cornerstone" purchasers, signaling institutional confidence in the project's scale.

- Pricing Power: Units were priced at $1.10, and the market’s immediate reaction to push the price to $1.30 suggests investors view this as a "validation" event rather than just a dilutive one.

- The War Chest: These funds are earmarked for the Tonopah West project—specifically for permitting and an exploration decline—moving the company from "explorer" toward "developer" status.

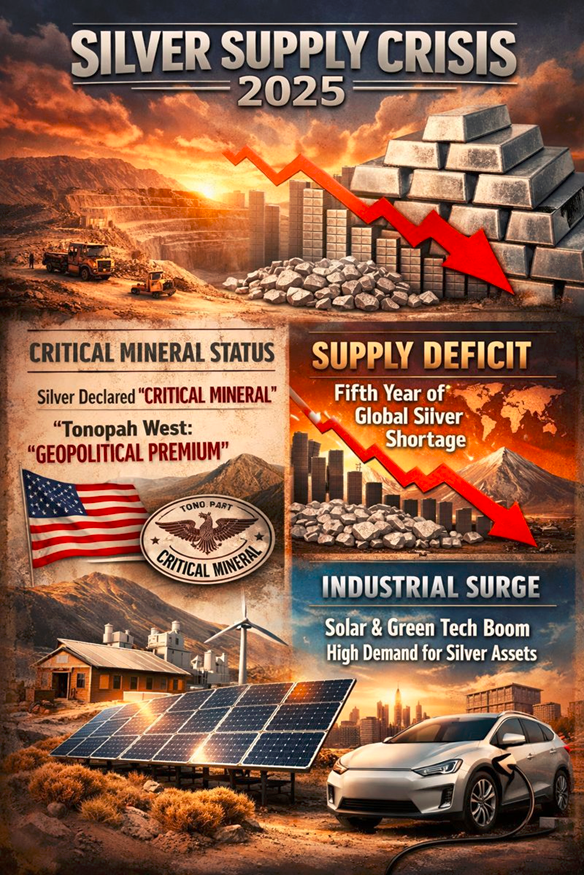

The Macro Tailbreak: Silver at $77+

You can’t talk about BRC without talking about the "White Metal." On December 24, silver prices hit a staggering $77/oz, fueled by:

Source: Kalkine Group

- Supply Deficit: 2025 marks the fifth consecutive year of a global silver supply gap.

- Critical Mineral Status: Following the U.S. classification of silver as a "critical mineral" earlier in 2025, domestic projects like Tonopah West have gained a massive "geopolitical premium."

- Industrial Surge: Solar and green tech demand has reached an inflection point, making primary silver assets (like BRC's) highly coveted.

Latest Business Model & Operational Updates

Blackrock Silver has shifted its model from broad-spectrum exploration to aggressive de-risking of its flagship Nevada assets.

Tonopah West (Flagship)

- The "Bonanza" Zone: Recent final assays from the Eastern Expansion Program (Dec 2, 2025) confirmed high-grade silver-gold mineralization extending 1.2km beyond the previous resource.

- Killer Intercept: One drill hole (TXC25-173) hit 2,122 g/t AgEq (Silver Equivalent) over nearly a meter, proving the "high-grade" thesis remains intact.

- Upcoming Catalyst: An updated Mineral Resource Estimate (MRE) and a new Preliminary Economic Assessment (PEA) are scheduled for February 2026.

Infrastructure Advantage

Unlike remote "fly-in" projects, Blackrock’s assets sit on private land with direct highway and power access near Tonopah, Nevada—the "Silver State." This significantly lowers the barrier to production.

SWOT Analysis: The Hard Truth

Source: Kalkine Group

Risk Factors: What Could Go Wrong?

Despite the 2025 rally, retail investors must weigh the "Junior Miner" risks:

- Dilution: While the $15M raise is positive, warrants at $1.50 could create a "ceiling" on the stock price in the mid-term.

- Execution: The transition from drilling holes to building a mine is notoriously difficult and capital-intensive.

- Market Sentiment: Small-cap miners on the TSXV are highly sensitive to broader interest rate movements and "risk-off" cycles.

Conclusion

Blackrock Silver’s 7.4% jump on Dec 24 wasn't a fluke; it was the market pricing in decreased bankruptcy risk (via the $15M raise) and increased asset value (via $77 silver). With the updated PEA arriving in early 2026, the company is entering its most critical phase of valuation discovery.

Please wait processing your request...

Please wait processing your request...