Silvercorp Metals Inc. (TSX: SVM) closed the penultimate trading day of 2025 with a sharp 3.4% gain, outperforming several of its mid-tier peers and catching the eyes of retail "stackers" and institutional analysts alike.

As silver prices flirt with multi-year highs, the company’s unique "China Cash + Global Growth" strategy is finally hitting its stride.

Key Drivers: Why SVM Popped on Dec 30, 2025

The rally wasn't just a "Santa Claus" bump; it was driven by a convergence of macro tailwinds and company-specific milestones:

Source: Kalkine Group

- The "S&P/TSX Composite" Effect: Effective December 22, Silvercorp was added to the S&P/TSX Composite Index. This forced buying from ETFs and institutional funds seeking to match the index, providing a massive liquidity cushion.

- Silver’s AI & Solar "Double Whammy": Silver prices soared late in 2025 as the global AI data center boom and 80% of Chinese solar panel manufacturing (major consumers of silver) outpaced supply.

- Condor Project PEA Fireworks: On Dec 22, Silvercorp released a Preliminary Economic Assessment (PEA) for its Condor gold project in Ecuador, revealing a staggering $522M after-tax NPV and a 29% IRR. At near-spot prices, that NPV jumps to over $1.5B, signaling massive untapped value.

- The El Domo De-Risking: The market is beginning to price in the 2026 production start for the El Domo copper-gold mine, which is now fully permitted and largely funded.

Latest Business Model: The "Dividend Miner" evolves into a "Growth Giant"

Silvercorp has shifted from being a pure-play Chinese silver producer to a diversified global developer.

- The Cash Engine: High-grade, low-cost mines in China (Ying & GC) generate consistent free cash flow.

- The Growth Leg: These profits are being funneled into high-potential jurisdictions like Ecuador (El Domo, Condor).

- The Synergy: By using its own cash for construction rather than dilutive equity raises, Silvercorp preserves shareholder value—a rarity in the junior/mid-tier mining space.

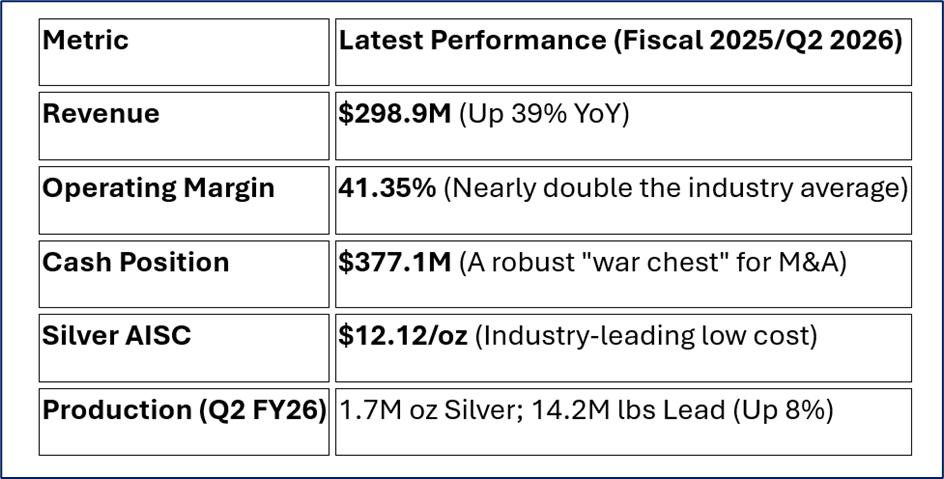

Financial & Operational Update (Latest FY 2025/2026 Data)

Silvercorp’s recent earnings confirm it remains a "Margin Machine":

Source: Company Data

Operational Milestone: The Ying Mine mill expansion is now fully operational, increasing capacity from 2,500 to 4,000 tonnes per day, allowing the company to process more ore even when grades fluctuate.

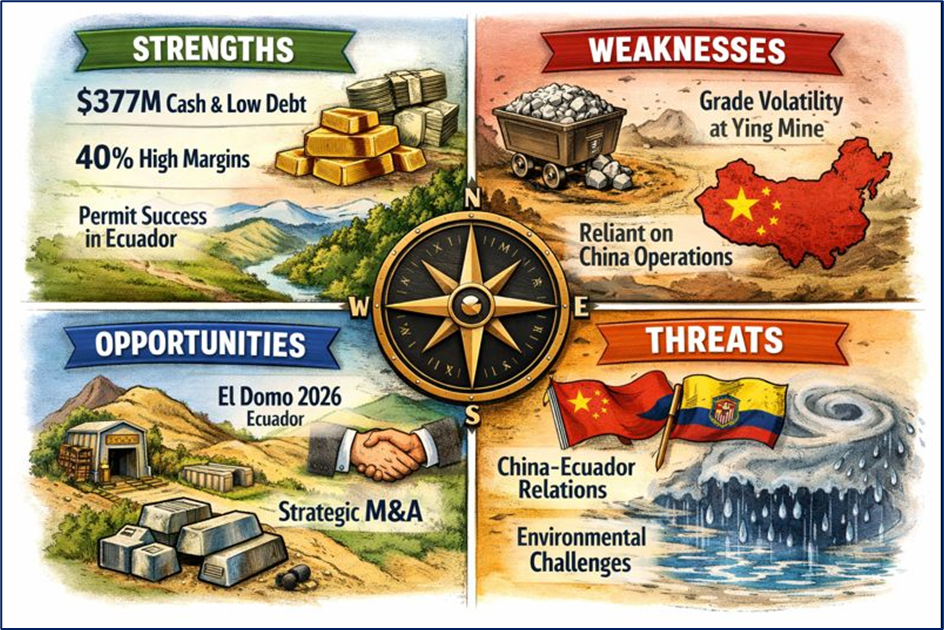

SWOT Analysis

Source: Kalkine Group

Strengths

- Cash-Rich: $377M in cash with very low debt.

- High Margins: Operating margins exceed 40%, far higher than many North American peers.

- Permitting Prowess: Successfully navigated complex environmental permits in Ecuador.

Weaknesses

- Grade Volatility: Occasional dips in silver head grades at Ying can lead to production misses.

- Geopolitical Concentration: Still heavily reliant on Chinese operations for 100% of current cash flow.

Opportunities

- El Domo 2026: First production in Ecuador will radically change the company's risk profile.

- Strategic M&A: Using its high-priced equity and cash to swallow smaller, distressed developers.

- Base Metal Rally: Rising Lead and Zinc prices provide "negative" cash costs for silver.

Threats

- China-Ecuador Relations: Shifts in international trade policy.

- Environmental Challenges: Heavy rain and typhoon conditions in China have caused temporary shutdowns in 2025.

Risks to Watch

Investors shouldn't ignore the "Safety Incident" mentioned in mid-2025, which caused a temporary production shortfall. Additionally, the Condor project is still in the "Citizen Participation" phase; while momentum is positive, social license in South American mining is never guaranteed.

Conclusion: The 2026 Outlook

Silvercorp enters 2026 in its strongest position in a decade. With a Forward P/E of ~8.1x (compared to a trailing P/E of 56x), the market is just beginning to realize the earnings power of the new Ying expansion and the Ecuador pipeline. If silver stays above $30/oz, SVM’s "cash cow" in China will likely continue to fund its "golden future" in South America.

Please wait processing your request...

Please wait processing your request...