The junior mining sector just got a wake-up call. On January 6, 2026, Stakeholder Gold Corp. (TSXV: SRC) saw its stock price surge by approximately 26% (peaking as high as 43% in early trading), closing the gap on a multi-month consolidation phase.

While the broader gold market has been buoyed by geopolitical volatility and record highs, Stakeholder’s aggressive move suggests something more specific is brewing under the surface of its Yukon and exotic stone portfolios.

The Catalyst: Why the 26% Spike on January 6?

Source: Kalkine Group

The sudden rally in SRC shares appears to be a "perfect storm" of technical positioning and recent fundamental milestones.

- The "January Effect" & Sector Rotation: Small-cap gold explorers often see a surge in early January as tax-loss selling ends and investors hunt for high-beta plays.

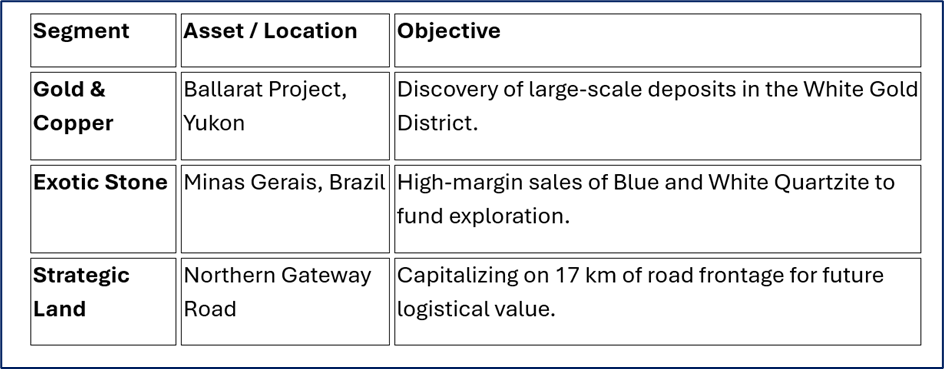

- Yukon Infrastructure Momentum: The company’s Ballarat Project straddles 17 km of the proposed Northern Gateway Road. Recent updates regarding the road’s progress have turned Stakeholder’s 19,440-hectare land package into a strategic real estate play within the White Gold District.

- Exotic Stone Revenue Confirmation: Unlike traditional "burn-only" explorers, Stakeholder has been shipping Blue and White Quartzite. Strong year-to-date operating results (reported late Q4 2025) showing gross margins of 76.9% in the stone business have finally begun to resonate with retail investors looking for de-risked exploration.

The 2026 Business Model: Exploration Funded by "Exotics"

Stakeholder Gold operates a rare hybrid business model designed to solve the "junior miner’s dilemma"—dilution.

By generating cash flow from its Brazilian quartzite business, Stakeholder aims to fund its Yukon drill programs without the constant need for "flow-through" private placements that dilute existing shareholders.

Source: Company Data

Latest Financial & Operational Updates

According to recent filings (Q3/Q4 2025):

- Operational Cash Flow: The exotic stone business achieved a 76.9% gross margin in H1 2025, with revenue continuing to scale into 2026 following the first shipments of the new White Quartzite product.

- Exploration Footprint: The company recently completed 5,036 soil samples and ridge-and-spur sampling at Ballarat. Results have identified two primary targets: Skye Gold and Loki Copper.

- Land Tenure: Stakeholder successfully filed assessment work to maintain its 930 contiguous claims through to 2036, securing its position in the Yukon for the next decade.

SWOT Analysis: The SRC Reality Check

Source: Kalkine Group

Strengths

- Revenue-Generating: Real cash flow from stone sales reduces the need for dilutive financing.

- Strategic Location: Proximity to the Northern Gateway Road in the Yukon.

- High Margins: Low-cost quarrying of quartzite provides a unique funding engine.

Weaknesses

- Micro-cap Liquidity: Low average daily volume can lead to extreme price volatility.

- Unprofitable (Net): Despite high gross margins in stone, the company is still in the "net loss" phase due to heavy exploration spending.

Opportunities

- Drill Discovery: A major hit at Skye Gold or Loki Copper could lead to a massive re-rating.

- M&A Potential: Positioned in a district (White Gold) that has seen significant interest from majors like Newmont and Agnico Eagle.

Threats

- Commodity Pricing: A drop in gold or industrial stone demand could squeeze margins.

- Permitting/Regs: Yukon environmental regulations remain a complex hurdle for any project moving toward development.

Key Risks to Watch

Investors should remain cautious. The 26% jump comes with inherent risks:

- Dilution History: While the goal is self-funding, Stakeholder has historically used private placements (e.g., Nov 2025) to bolster its treasury.

- Exploration Risk: There is no guarantee that the soil anomalies at Ballarat will translate into a mineable resource.

- Geopolitical/Supply Chain: The exotic stone business relies on logistics from Brazil, which can be subject to shipping delays or cost fluctuations.

Conclusion

Stakeholder Gold’s performance on January 6, 2026, reflects a growing market appreciation for its "revenue-first" exploration strategy. By leveraging the cash flow from Brazilian quartzite to hunt for "elephant-sized" deposits in the Yukon, SRC is attempting to rewrite the junior mining playbook. While the stock remains a high-risk micro-cap, the combination of a 76%+ margin business and a strategic 17 km road-frontage land package makes it one of the more unique stories in the TSX-V materials sector this year.

Please wait processing your request...

Please wait processing your request...