Investors waking up after the Christmas break noticed a quiet but firm green candle for Jamieson Wellness Inc. (TSX: JWEL). On December 24, 2025, the stock nudged up ~1%, closing at CAD 33.28. While the broader TSX composite ended the shortened session lower, Jamieson’s resilience highlighted its status as a premier "defensive growth" play.

As we head into 2026, the story isn't just about vitamins—it's about a Canadian icon transforming into a global health powerhouse. Here is the analytical deep dive into why JWEL is trending.

Key Drivers: Why the Stock Nudged Higher

The Christmas Eve gain was fueled by a mix of seasonal sentiment and fundamental strength:

Source: Kalkine Group

- The "Health Kick" Front-Running: Investors traditionally accumulate health and wellness stocks in late December, anticipating the "New Year, New Me" surge in consumer spending on supplements and vitamins.

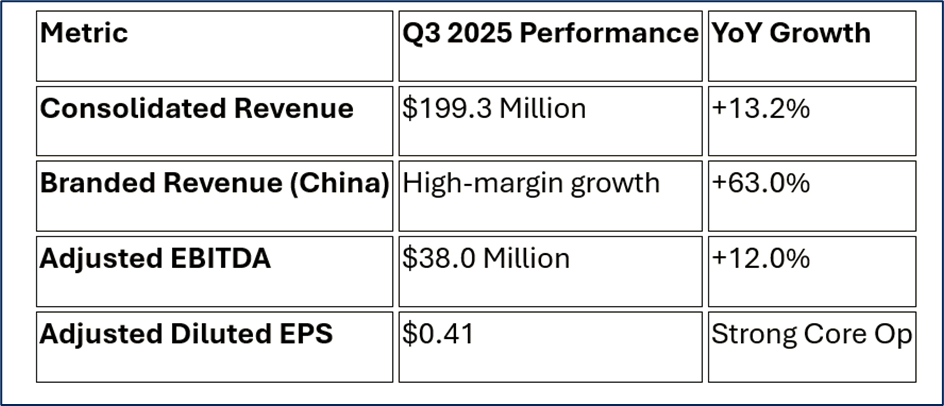

- China Momentum: Branded revenue in China surged 63% in the most recent quarter. The market is pricing in a massive Q4 2025 result following the successful 11/11 (Singles' Day) shopping festival.

- Dividend Reliability: Jamieson recently increased its quarterly dividend to $0.23/share, a 9.5% hike that signals management's confidence in cash flow.

Latest Financial & Operational Updates

Jamieson’s 2025 fiscal year has been defined by "scaling up."

Source: Company Data

2025 Full-Year Guidance: Management has narrowed its revenue target to $810 – $830 million. The company is officially on the "Road to $1 Billion," a milestone analysts expect them to hit by 2027.

The Latest Business Model: "The Global 360 Ecosystem"

Jamieson has evolved from a Canadian manufacturer into a vertically integrated global brand owner. Its model now rests on three pillars:

- Jamieson Brands (Core): Dominating the Canadian market with #1 brand equity while aggressively expanding into the Middle East and SE Asia.

- Youtheory (Lifestyle Growth): A U.S.-based acquisition focusing on collagen and "beauty from within," bridging the gap between pharmacy health and lifestyle wellness.

- Direct-to-Consumer (DTC) & Social Commerce: Moving away from just "shelf space" to "screen space," leveraging influencers on TikTok and Amazon to drive 50%+ growth in digital-heavy markets like China.

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Unrivaled Heritage: Over 100 years of "360 Pure" quality standards.

- High Margins: Branded products offer significant pricing power over generic competitors.

- Geographic Diversification: Reduced reliance on Canada as China and the U.S. become major revenue drivers.

Weaknesses

- Debt Load: Net debt sits around $371 million. While manageable, it remains a point of scrutiny for conservative analysts.

- Inventory Buildup: Recent increases in inventory to mitigate supply chain risks have temporarily weighed on cash-from-operations.

Opportunities

- The "Longevity" Trend: Aging populations in the West and a growing middle class in Asia are increasing per-capita spend on VMS (Vitamins, Minerals, and Supplements).

- E-commerce Dominance: Continued expansion into social commerce platforms (Little Red Book, Douyin) offers a low-CapEx way to reach millions.

Threats

- Tariff Volatility: Global trade uncertainties, particularly between the U.S., Canada, and China, could impact raw material costs.

- Retail Competition: Private label (store brands) continues to pressure the "value" segment of the market.

Critical Risks to Watch

- Macroeconomic Pressure: While health is "defensive," a severe recession could see consumers trade down from premium Jamieson products to cheaper generic brands.

- Currency Fluctuations: As international revenue grows, JWEL is increasingly exposed to the USD and CNY exchange rates.

- Regulatory Hurdles: Stricter Health Canada or FDA regulations on supplement labeling could increase compliance costs.

Conclusion

Jamieson Wellness (TSX: JWEL) is no longer just a "boring" dividend stock. By successfully pivoting to a digital-first, global expansion strategy—particularly in the high-margin Chinese market—the company has found a new gear for growth. The 1% gain on December 24 reflects a market that is starting to recognize JWEL as a rare bird: a defensive asset with double-digit growth potential.

Please wait processing your request...

Please wait processing your request...