The S&P/TSX Composite Index is expected to open on a positive note as investors kept tabs on developments in the Iran war and elevated oil prices. In the previous session, limited gains were mainly supported by the energy and utilities sectors, which only partially offset broader market pressure.

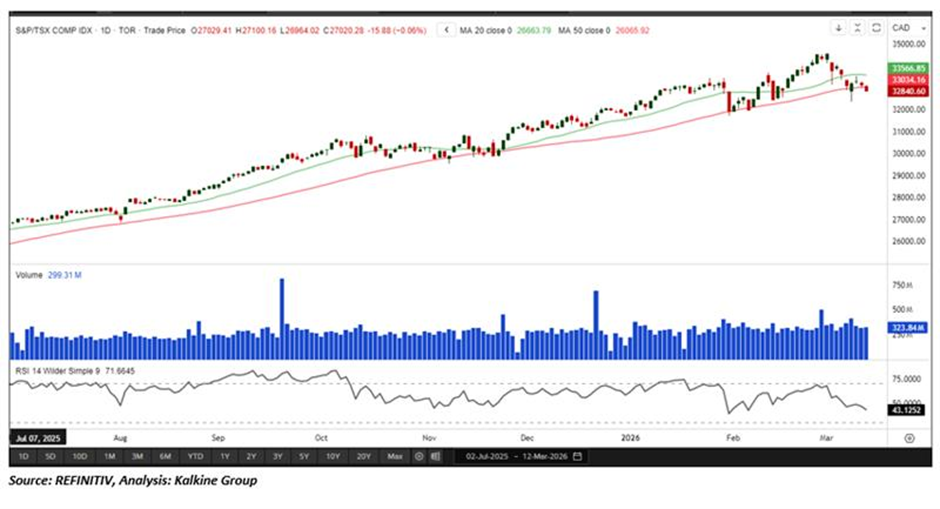

From a technical standpoint, the index continues to trade below a key rising trendline resistance near 33,300, signalling persistent near-term weakness in the market structure. As long as the index remains below this level, downside risks may persist, potentially leading to extended consolidation or further corrective movement. Immediate resistance remains near 33,300, and failure to reclaim this level could keep the broader tone defensive in the near term.

Global macro backdrop

Overnight, global equity markets showed modest gains as investors digested new economic data and earnings releases.

- In the U.S., economic indicators continue to suggest a resilient labor market and stable consumer spending, maintaining a backdrop of moderate growth.

- Inflation data remains under close scrutiny, with markets assessing the pace at which central banks, including the Federal Reserve, might adjust policy later this year.

- European equities opened mixed, reflecting concerns about regional industrial output and commodity import costs, while Asian markets ended mostly higher, supported by tech and manufacturing gains.

Investor sentiment remains sensitive to bond yield movements, with rising yields pressuring growth-sensitive sectors but benefiting financials.

Canada-specific themes

The Canadian market continues to react to U.S. economic cues, especially data on inflation, employment, and consumer spending.

- The Bank of Canada is expected to maintain its cautious stance as policymakers monitor inflation trends and economic growth.

- Rising global interest rates and bond yields could influence the financial sector and high-dividend TSX components.

- The U.S. dollar’s strength remains a factor for commodity-linked Canadian exporters.

Commodity view — what to watch

- Crude oil: Crude prices stabilized overnight near $72/bbl Brent amid mixed supply signals and global demand expectations. Energy stocks in Canada often respond sharply to daily oil price swings.

- Gold: Gold remained resilient around $1,985/oz as investors maintain a cautious stance on risk amid macroeconomic uncertainty. Rising gold prices generally support TSX-listed mining stocks.

- Base metals: Copper held steady near $4.15/lb, reflecting ongoing industrial demand from Asia. Canadian base metal miners are sensitive to these moves, given export exposure and global infrastructure demand.

Sector highlights

- Energy: TSX-listed oil and gas companies may see volatility tracking crude price fluctuations and supply-demand developments in North America and OPEC+ guidance.

- Materials: Gold and base metal miners are likely to remain in focus, with performance closely tied to global metal prices and investor sentiment toward safe-haven assets.

- Financials: Canadian banks are expected to react to bond yield shifts and interest rate expectations. Rising yields could support net interest margins, but slower economic growth may dampen loan demand.

- Technology: Tech stocks will continue to track North American peers, while industrials are influenced by global manufacturing trends and commodity pricing.

FX and rates snapshot

- The Canadian dollar has edged higher against the U.S. dollar, supported by crude prices.

- Bond yields are a focal point for investors, with movements in 10-year government bonds influencing risk appetite and equity sector rotation.

Bottom line:

The TSX Composite is expected to open with a cautious-to-mixed tone. Resource sectors, particularly energy and mining, are likely to lead early trading, while financials and industrials may track global bond yield movements. Investors are balancing macro uncertainty, commodity prices, and corporate news as they enter the last trading day of the week.

Please wait processing your request...

Please wait processing your request...