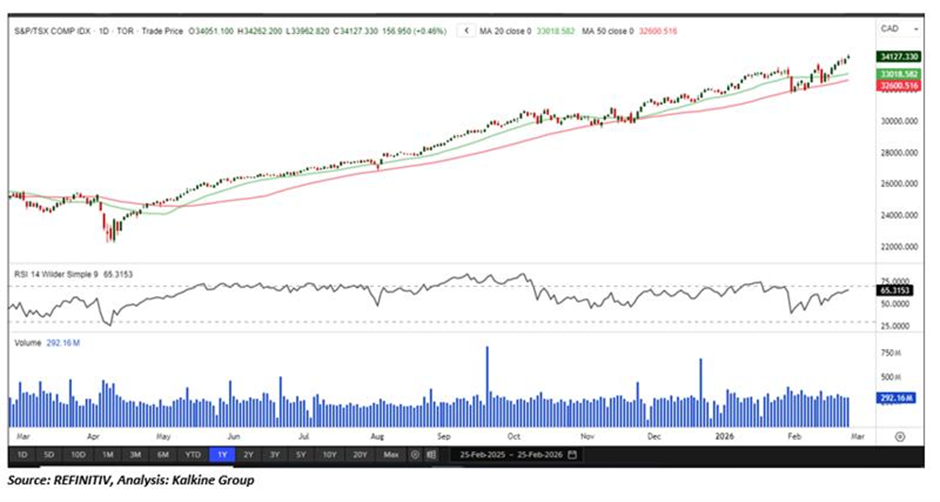

Index Update: The S&P/TSX Composite Index gave back some ground in the final hour of trading but still ended the day up 156.95 points or 0.5 percent at a new record closing high of 34,127.33.

Macro Update: Geopolitical risks also remain on investors' radar as the third round of nuclear negotiations between the United States and Iran kicked off in Geneva against a backdrop of continued mistrust. Ahead of the meeting, the U.S. imposed sanctions on more than 30 individuals, companies and vessels linked to Tehran's oil trade. U.S. Secretary of State Marco Rubio said Iran possessed a very large number of ballistic missiles that threaten U.S. interests in the region and it was trying to develop weapons that can reach the continental United States. Vice President JD Vance said Tehran should take Washington's threats of military action seriously. In economic releases, U.S. weekly jobless claims data will be in the spotlight later today, followed by January's producer price index report on Friday.

Top Movers: The financial sector led the charge after National Bank of Canada soared 6.6% and Bank of Montreal surged 3.8% following Q1 profit beats. These gains, alongside a 2.5% rise in CIBC and 2% in TD, comfortably offset a 5.5% slump in Loblaw and a 2.2% drop in Canadian National Railway. Tech shares remained a significant tailwind, with Shopify rising 2.6% and Thomson Reuters jumping 10.1% amid broader optimism ahead of major US software earnings. While commodity-linked stocks saw mixed results, Barrick Gold and Canadian Natural Resources both eased slightly, the strength in Bay Street’s heavyweights ensured a record-breaking session.

Our Stance: Momentum indicators remain constructive, with the 14-period RSI at 65.31, signaling firm buying interest while remaining below overbought levels, suggesting room for further gains. Immediate support is seen near the 34,100 mark; holding above this zone would preserve the bullish structure, whereas a decisive break could trigger a corrective move toward the 33,800–33,600 support range.

Commodity Update: The U.S. dollar traded softer in early Asian hours on Thursday as upbeat earnings from Nvidia supported broader risk sentiment, while markets awaited clarity on fresh U.S. import tariffs. Precious metals eased, with gold declining 0.52% to USD 5,199.00, silver slipping 2.54% to USD 88.68, and copper down 0.38% to USD 13,279.00. Brent crude edged up 0.30% to USD 71.12, holding near seven-month highs despite rising U.S. inventories.

Technical Update:

On Wednesday, the S&P/TSX Composite Index advanced 156.95 points, or 0.57%, to close at 34,127.33, supported by steady trading volumes that indicate sustained investor participation and stable market breadth. From a technical perspective, the index continues to trade comfortably above its 50-period Simple Moving Average, reinforcing the strength and continuity of the prevailing short-term uptrend. Momentum indicators remain constructive, with the 14-period RSI at 65.31, signaling firm buying interest while remaining below overbought levels, suggesting room for further gains. Immediate support is seen near the 34,100 mark; holding above this zone would preserve the bullish structure, whereas a decisive break could trigger a corrective move toward the 33,800–33,600 support range.

Please wait processing your request...

Please wait processing your request...