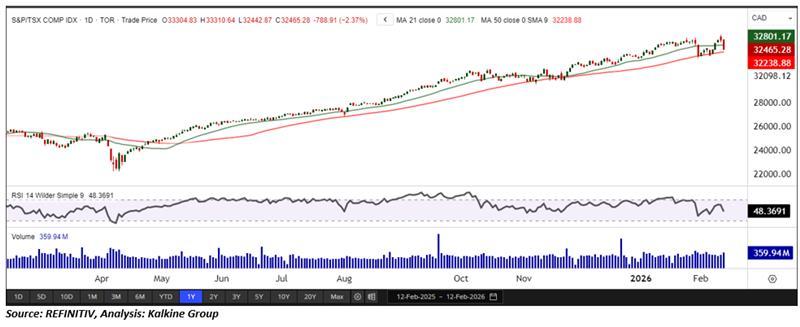

Index Update: After opening slightly above yesterday's close, today the benchmark S&P/TSX Composite Index gave ground early in the session and saw further downside as the day progressed before settling at 32,465.28, down by 788.91 points (or 2.37%).

Macro Update: The Bank of Canada's Summary of Deliberations from its interest rate decision last month was released yesterday. The report revealed that the governing council of the central bank highlighted that persisting geopolitical turbulence and growing trade uncertainty have increased the risks to its economic outlook for Canada and thereby made it difficult for it to predict which way interest rates are heading. Last month, the BoC maintained its policy interest rate on hold at 2.25%. While announcing the rates, the central bank asserted that it would respond appropriately if the economic outlook changed. The next monetary policy decision announcement is scheduled for March 18. The council has highlighted three key risk areas - the upcoming Canada-United States-Mexico trade agreement's renewal, ongoing geopolitical events, and trade disruptions. Today in the U.S., the Department of Labor revealed that initial jobless claims fell by 5,000 from the previous week to 227,000 (in the first reading for February), above market expectations of 222,000. However, continuing jobless claims increased to 1,862,000 for the week ending January 31 from 1,841,000 of the previous week.

Top Movers: Among the individual stocks, Saputo Inc (3.64%), The North West Company Inc (3.36%), Loblaw CO (2.53%), AltaGas Ltd (3.76%), Emera Incorporated (3.22%), and Rogers Communications Inc (2.24%) were the prominent gainers.

Our Stance: Momentum signals are mixed, with the Relative Strength Index (RSI) at 48.36, indicating lingering weakness and keeping the trend in neutral-to-bearish territory. On the downside, 31,400 represents immediate support. A decisive break below this level could accelerate corrective pressure toward 32,100, while the next major support zone is located near 32,000, where buyers may attempt to re-enter.

Commodity Update: The Japanese yen headed for its strongest weekly performance in nearly 15 months, supported by confidence after Prime Minister Sanae Takaichi’s election victory eased fiscal concerns. In commodities, gold rose 1.12% to USD 5,004.30, silver gained 1.62% to USD 76.90, and copper added 0.75% to USD 12,985. Brent crude advanced 0.40% to USD 67.55 but remained on track for a second weekly decline amid easing Iran-related supply risks.

Technical Update:

The S&P/TSX Composite Index retreated sharply on Thursday, falling 788.91 points (−2.37%) to close at 32,465.28, as short-term profit-taking interrupted the recent upside momentum. From a technical standpoint, the index continues to trade below its 21-period Simple Moving Average (SMA), which remains a key short-term resistance level and caps recovery attempts. Momentum signals are mixed, with the Relative Strength Index (RSI) at 48.36, indicating lingering weakness and keeping the trend in neutral-to-bearish territory. On the downside, 31,400 represents immediate support. A decisive break below this level could accelerate corrective pressure toward 32,100, while the next major support zone is located near 32,000, where buyers may attempt to re-enter.

Please wait processing your request...

Please wait processing your request...