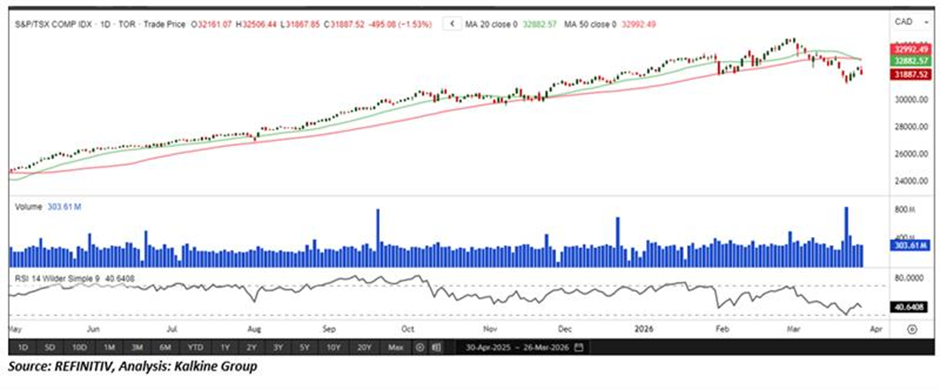

The S&P/TSX Composite Index is expected to open on a softer note, extending the impact of the recent market sell-off and reflecting continued weakness in investor sentiment. In the previous session, losses were largely driven by the basic materials and technology sectors, which intensified overall selling pressure.

However, from a technical perspective, the index remains below a key rising trendline resistance near the 32,100 level, signalling ongoing fragility in the near-term market structure. As long as the index trades beneath this barrier, downside risks are likely to persist, potentially resulting in further consolidation or corrective movement. Immediate resistance is positioned around 32,100, and a sustained failure to reclaim this level may keep the broader market tone cautious in the near term.

Global markets are showing a subdued tone ahead of the North American open:

- U.S. equities closed slightly lower in the previous session, as investors reacted to softer economic data and ongoing concerns about inflation staying elevated longer than expected.

- Federal Reserve commentary continues to emphasize a cautious approach, with policymakers signaling that rate cuts may be gradual and dependent on incoming data.

- European markets are trading mixed, with weakness in manufacturing offset by resilience in services activity.

- Asian equities ended the session on a mixed note, with Chinese markets stabilizing on policy support expectations while Japan saw pressure from currency fluctuations.

Global bond yields remain relaively elevated, continuing to weigh on equity market sentiment, particularly in rate-sensitive sectors.

Macro News Impacting the TSX

The TSX Composite is likely to see sector-driven movement at the open:

- Investors are watching Canadian GDP and inflation signals, which could shape expectations around the Bank of Canada’s next policy move.

- Domestic equities continue to take cues from commodity prices and global macro trends, particularly developments in the U.S. and China.

Commodity view — what to watch

- Crude oil: Oil crude futures rose back above $95 per barrel on Friday, near the highest since July 2022, amid skepticism that the US and Iran could reach a deal to end the war soon.

- Gold: Gold rose above $4,400 per ounce on Friday after a sharp decline in the previous session, as President Donald Trump pushed back his deadline for Iran to secure a deal to end the war.

- Silver: Silver strengthened to around $70 per ounce on Friday, reversing losses from the previous session as President Donald Trump postponed his deadline for Iran to secure a deal to end the war.

- Base metals: Copper rose above $5.5 per pound on Friday and was set for its first weekly gain since the Middle East conflict began, supported by hopes for a diplomatic resolution between the US and Iran.

Sector highlights

- Energy: May face mild pressure due to softer oil prices but remains supported by longer-term fundamentals.

- Materials: Likely to benefit from stable metals prices and strong gold performance.

- Financials: Sensitive to bond yield movements and macroeconomic outlook.

- Technology & Industrials: Expected to follow global sentiment and economic signals.

Forex watch

- The Canadian dollar (CAD) is slightly weaker against the U.S. dollar, reflecting softer oil prices and broader USD strength.

- Currency movements could influence export-driven sectors, with a weaker CAD potentially supporting earnings for commodity exporters.

Bottom line:

The TSX Composite is expected to trade cautiously at the open, with a slight downside bias as investors digest mixed commodity signals and macro uncertainty. Energy weakness may weigh on the index, while strength in gold and materials could help limit declines.

As the week concludes, market participants are likely to remain selective, balancing defensive positioning with opportunities in commodity-linked sectors. Volatility may increase due to portfolio rebalancing and positioning ahead of the new quarter.

Please wait processing your request...

Please wait processing your request...