The S&P/TSX Composite Index is expected to open on a weaker footing after recently trading close to record highs. The prior session’s advance was broad-based, with notable leadership from energy and materials stocks.

Despite this constructive backdrop, escalating geopolitical tensions between Israel and Iran are likely to dampen near-term risk appetite and encourage a more cautious tone in early trade.

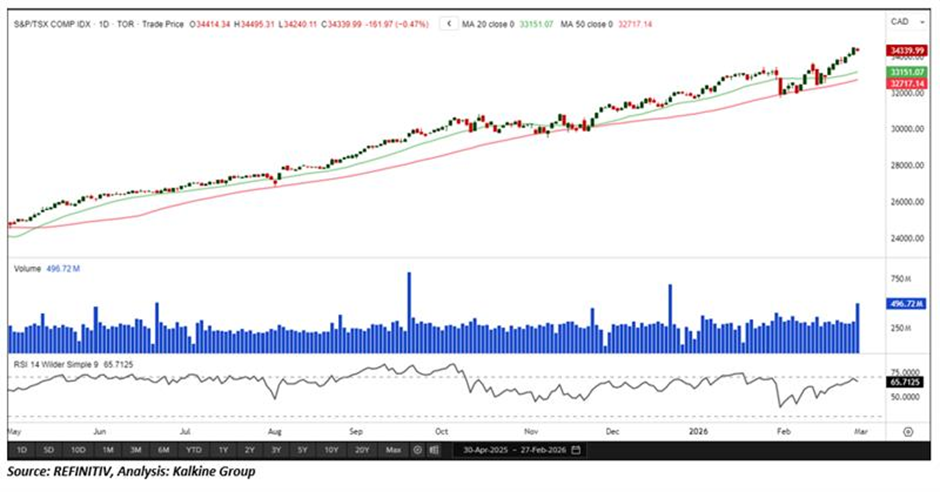

Technically, the index continues to hold above key support near the 33,700 level, which remains critical in preserving the prevailing bullish structure. A sustained move below this zone could prompt short-term consolidation. On the upside, resistance around 34,650 may act as an immediate hurdle. A decisive breakout above this level, accompanied by firm volume, would signal renewed momentum and open the door for further gains.

Global macro backdrop

Risk appetite is being tempered by lingering uncertainty around the path for global interest rates and fresh data releases from major economies. Investors are watching economic indicators and central bank commentary for clues on the timing of policy easing or further tightening. Equity futures in major markets are trading in a range, reflecting investor reluctance to take big directional bets ahead of key releases.

Canada-specific themes

Domestically, attention remains on inflation trends, wage growth and housing activity — all factors the Bank of Canada has flagged as important to its policy outlook. Canadian yields and the differential with U.S. Treasury yields will be important for bank stocks and the broader market’s risk tone.

Commodity view — key drivers for the TSX

- Crude oil: Energy names on the TSX will track moves in global crude. Supply discipline among major producers and any geopolitical developments could lift prices and help the heavyweight energy sector.

- Gold: Precious metals remain a key watch — gold typically benefits during risk-off episodes and can support Canadian gold producers’ stocks when bullion firm.

- Base metals: Copper and industrial metals are sensitive to Chinese demand and global manufacturing signals. Mixed readings on demand can translate to selective movement across miners.

Sector highlights

- Energy: A sustained uptick in crude would directly favour integrated producers and exploration & production names.

- Materials: Precious-metals miners and select base-metal producers will lead any commodity-driven advance; explorers may outperform on positive headlines.

- Financials: Major banks remain sensitive to yield curve dynamics and loan-growth expectations; muted move in yields typically produces muted action in the sector.

- Real estate & housing-exposed names: Respond to domestic mortgage and housing data; continued softening in activity could keep the sector subdued.

- Technology & growth: Rate-sensitive and likely to follow U.S. tech cues and bond-market moves.

FX and rates snapshot

The loonie will track oil and the broader U.S. dollar trend. North American yield moves — especially the 2- and 10-year spread — will influence bank stocks and rate-sensitive sectors. Expect intraday swings if U.S. fixed-income markets react to economic prints.

Outlook

TSX set for a cautious open as commodity moves and rate expectations dictate early action — energy and materials likely to lead while financials watch the yield curve.

Commodity prices and fixed-income moves will be the primary drivers for the TSX at the open. With the macro calendar still active, expect measured trading and selective sector rotation rather than a broad market breakout.

Please wait processing your request...

Please wait processing your request...