The S&P/TSX Composite Index is expected to open on a positive note following the recent wave of selling pressure. In the previous session, modest gains were supported by strength in the energy and utilities sectors, helping to cushion broader market weakness.

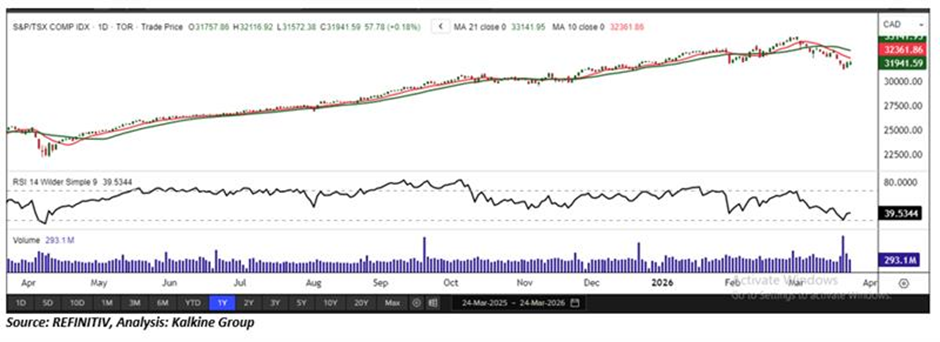

However, from a technical standpoint, the index continues to trade below a key rising trendline resistance near the 32,200 level, signalling ongoing caution in the near-term market structure. As long as the index remains below this barrier, the risk of further consolidation or corrective movement is likely to persist. On the upside, immediate resistance is positioned around 32,200, and a sustained breakout above this level will be crucial to restore stronger bullish momentum in the sessions ahead.

Global equities are showing mixed signals ahead of the North American session:

- U.S. markets ended slightly lower yesterday after weaker-than-expected manufacturing data raised concerns about industrial activity, despite solid consumer spending.

- European indices are steady, supported by improved services sector activity and stabilizing energy prices.

- Asian markets closed higher, with Chinese equities boosted by optimism over industrial policy and infrastructure spending.

Bond yields in the U.S. and Canada remain elevated, reflecting ongoing concerns about inflation and expectations that central banks may maintain higher-for-longer rates. These dynamics continue to influence investor sentiment and equity valuations globally.

Macro News Impacting the TSX

The TSX Composite is expected to track commodity strength while weighing macro risks:

- Investors are eyeing upcoming Canadian economic indicators, particularly retail sales and inflation updates.

- Banks and interest-rate-sensitive sectors may experience muted activity amid cautious sentiment, while energy and mining could see selective buying.

Commodity view — what to watch

- Crude oil: WTI crude oil futures dropped more than 6% to $86.8 per barrel on Wednesday as US diplomatic efforts to end the war with Iran gained traction, overshadowing reports of additional troop deployments and the near-closure of the Strait of Hormuz.

- Gold: Gold climbed above $4,500 on Wednesday, extending gains from the previous session as hopes for an end to the prolonged Middle East conflict grew on reports that the US was pursuing talks with Iran.

- Silver: Silver climbed above $73 per ounce on Wednesday, extending gains for a third straight session as optimism for an end to the prolonged Middle East conflict grew on reports that the US was pursuing talks with Iran.

- Base metals: Copper climbed to around $5.5 per pound on Wednesday, erasing the previous session’s losses as hopes for a Middle East ceasefire supported a broad rebound across metals markets.

Sector highlights

Energy: Expected to lead gains with oil holding above key support levels.

Materials & Mining: Supported by stronger copper and gold prices, and sustained global industrial demand.

Financials: Likely to remain cautious due to elevated bond yields and rate sensitivity.

Technology & Industrials: Influenced by global growth signals and investor risk appetite.

Forex watch

- The Canadian dollar (CAD) is slightly stronger against the U.S. dollar, helped by higher oil prices and relative economic stability.

- A firm CAD may temper export-driven stock gains but benefits energy and resource sectors.

Bottom line:

The TSX Composite is expected to open with moderate gains supported by commodities, particularly energy and materials. Market participants are likely to adopt a selective approach, balancing optimism in resources with caution in rate-sensitive sectors.

Macro developments from the U.S., Europe, and China, along with commodity performance, will continue to set the tone for the day. Investors are advised to monitor key earnings and economic releases, which could provide intraday catalysts.

Please wait processing your request...

Please wait processing your request...