- The "Rate Cut" Tailwind: With interest rates stabilizing or dipping in late 2025/early 2026, capital-intensive sectors like Utilities and REITs are projected to see improved margins and lower borrowing costs.

- Energy Discipline: Canadian energy majors are no longer just drilling for growth; they are "cash flow machines," prioritizing debt repayment and shareholder returns (buybacks + dividends) over aggressive expansion.

- Banking Recovery: After a volatile 2024-2025 due to loan loss provisions, the "Big Six" banks are focusing on efficiency and core North American operations.

- Quality Over Yield: In 2026, the strategy shifts from chasing the highest yield (which can be a trap) to the safest growing cash flow (Free Cash Flow or FCF).

The 2026 Market Outlook

As we move into 2026, the TSX is seeing a rotation. The "AI trade" that dominated the US markets is maturing, and investors are seeking defensive value. Canadian dividend stocks—often termed "Widow-and-Orphan" stocks—are back in vogue. The consensus among analysts is that 2026 will favor companies with pricing power (to fight lingering inflation) and low payout ratios (to ensure dividend safety).

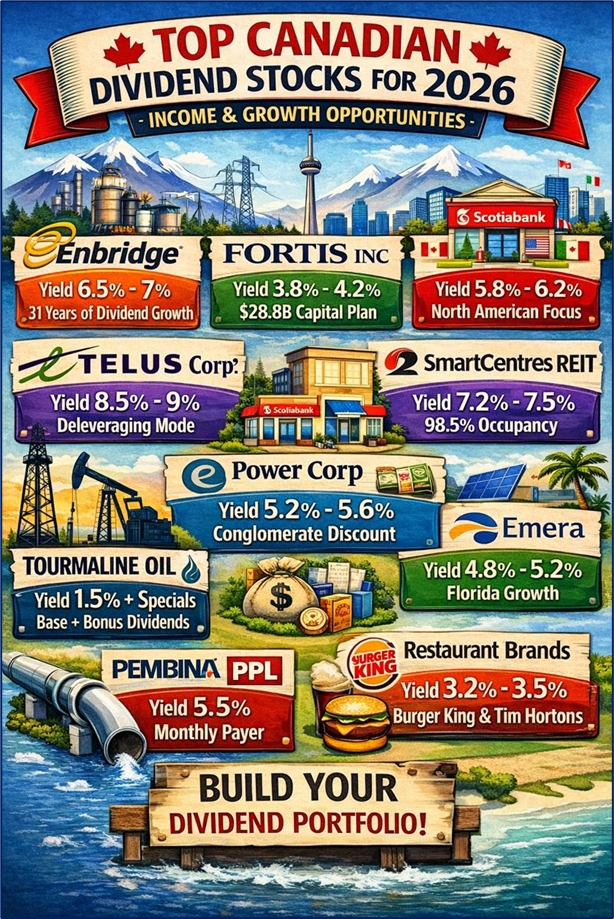

Top 10 High-Yield & Sustainable Stocks to Watch

Source: Kalkine Group

- Sector: Energy Infrastructure

- Estimated Yield: ~6.5% - 7.0%

- 2026 Update: Enbridge remains the heavyweight champion of income. For 2026, they have increased their dividend by 3% (marking 31 consecutive years of increases). The company’s pivot to natural gas utilities and renewables is paying off, providing regulated, utility-like stability to their cash flows.

- Why Watch: It’s a "sleep well at night" stock. Their payout ratio is well-managed within their distributable cash flow (DCF) guidance.

- Sector: Utilities

- Estimated Yield: ~3.8% - 4.2%

- 2026 Update: A true "Dividend King." Fortis has rolled out a massive $28.8 billion capital plan for 2026-2030. They have officially extended their guidance of 4-6% annual dividend growth through 2030.

- Why Watch: Boring is beautiful. With 99% regulated assets, Fortis is virtually immune to commodity price swings.

- Sector: Banking

- Estimated Yield: ~5.8% - 6.2%

- 2026 Update: Scotiabank is executing a strategic pivot, reducing exposure to riskier Latin American markets and refocusing capital into the stable North American corridor (Canada, US, Mexico).

- Why Watch: Often offers the highest yield among the "Big Five" banks. If their North American strategy gains traction in Q1/Q2 2026, the stock could see significant capital appreciation alongside the dividend.

- Sector: Telecommunications

- Estimated Yield: ~8.5% - 9.0%

- 2026 Update: Cautionary Watch. Telus offers a massive yield but has paused aggressive dividend hikes to focus on debt reduction and bringing their payout ratio back to a safer 75% range. They are targeting $2.4B in free cash flow for 2026.

- Why Watch: A potential turnaround play. If they successfully deleverage while monetizing their "Telus Health" and "Telus International" segments, this high yield could be a bargain.

- SmartCentres REIT (TSX: SRU.UN)

- Sector: Real Estate

- Estimated Yield: ~7.2% - 7.5%

- 2026 Update: With occupancy rates remaining sky-high (approx 98.5%), SmartCentres proves that physical retail isn't dead—especially when anchored by Walmart.

- Why Watch: Monthly income. Their shift into mixed-use properties (condos/rentals on top of retail) creates a new growth pipeline for 2026 beyond just rent collection.

- Sector: Energy (Natural Gas)

- Estimated Yield: ~1.5% (Base) + Special Dividends (Total often >5%)

- 2026 Update: Canada’s largest natural gas producer. They use a unique "Base + Special" dividend model. As they pay down debt, they funnel excess free cash flow directly to shareholders via special quarterly payments.

- Why Watch: The most responsible way to play the energy sector. You get a safe base yield, plus massive "bonus checks" when commodity prices spike.

- Sector: Financial Services / Holding Co.

- Estimated Yield: ~5.2% - 5.6%

- 2026 Update: This holding company (owning Great-West Life, IGM Financial) trades at a "conglomerate discount" (cheaper than the sum of its parts). They have been aggressively buying back shares.

- Why Watch: Double-digit income growth from its underlying insurance subsidiaries makes this an undervalued gem for value investors.

- Sector: Utilities

- Estimated Yield: ~4.8% - 5.2%

- 2026 Update: Emera is heavily focused on its Florida operations (Tampa Electric), which is a high-growth region. Their 2026 capital plan focuses on grid modernization and renewables.

- Why Watch: A way to get US Dollar exposure (via Florida earnings) while investing in a Canadian dividend stock.

- Sector: Energy Infrastructure

- Estimated Yield: ~5.5%

- 2026 Update: Like Enbridge, but with a monthly payout. Pembina has benefitted from the completion of recent expansion projects and maintains a very strong balance sheet with low leverage.

- Why Watch: Monthly passive income favorite. It has zero reliance on commodity prices for the majority of its revenue (fee-based contracts).

- Sector: Consumer Discretionary

- Estimated Yield: ~3.2% - 3.5%

- 2026 Update: The parent company of Tim Hortons, Burger King, and Popeyes. While the yield is lower, the growth rate of the dividend is high. They are aggressively expanding internationally in 2026.

- Why Watch: Defensive growth. Even in a recession, people buy coffee and burgers. It provides sector diversification away from the heavy banks/energy TSX index.

Strategy Session: How to Play It

Source: Kalkine Group

For the Retail Investor (The "Income Builder")

- The TFSA Fortress: In 2026, maximize your TFSA (Tax-Free Savings Account) contribution room. Holding high-yield stocks like SmartCentres or Enbridge here means 100% of that juicy 6-7% yield is yours to keep—tax-free.

- The "DRIP" Effect: If you don't need the cash now, turn on the Dividend Reinvestment Plan (DRIP). With markets recovering, reinvesting dividends to buy more shares at lower prices is the compounding engine that builds wealth.

- Avoid the "Yield Trap": Do not blindly buy the highest number. A stock yielding 12% often signals distress (the price has crashed). Stick to the 4% - 7% "sweet spot."

For the Fund Manager (The "Total Return" Hunter)

- Sector Rotation: Managers are rotating out of pure "cash" positions (as T-bill yields drop) and into "Bond Proxies" like Utilities (Fortis, Emera).

- Active Management in Energy: Institutional investors prefer companies like Tourmaline or Canadian Natural Resources because of their flexibility. They can turn capital returns up or down (via special dividends/buybacks) without cutting the base dividend, protecting the stock price.

Final Outlook

2026 is shaping up to be the year of "Sustainable Income." The aggressive rate hikes of the past are over, and the market is rewarding companies with clean balance sheets and predictable cash flows. The winners this year won't necessarily be the ones with the flashiest tech, but the ones paying you to wait.

Please wait processing your request...

Please wait processing your request...