Analytical Takeaways (Q4 2025 – Q4 2026 Outlook)

- Policy Catalyst: Canada's Critical Minerals Strategy (CMS) will continue to serve as the primary domestic policy driver, funnelling capital and streamlining political support toward copper and select associated metals. The focus is shifting from strategy announcement to project operationalization in 2026.

- Structural Deficits Persist: Both the copper and silver markets are forecast to remain in a structural deficit throughout 2026. This dynamic is driven by sustained, non-cyclical demand (electrification, solar) colliding with chronic production challenges (geopolitical risk, operational delays, declining grades).

- Gold’s Margin Defense: Elevated gold prices (with some forecasts indicating the potential for levels exceeding $5,000/oz by late 2026) are primarily viewed as a sustained function of global fiscal deficits and geopolitical uncertainty. For producers, the operational priority in 2026 is cost control to maximize these high-price margins.

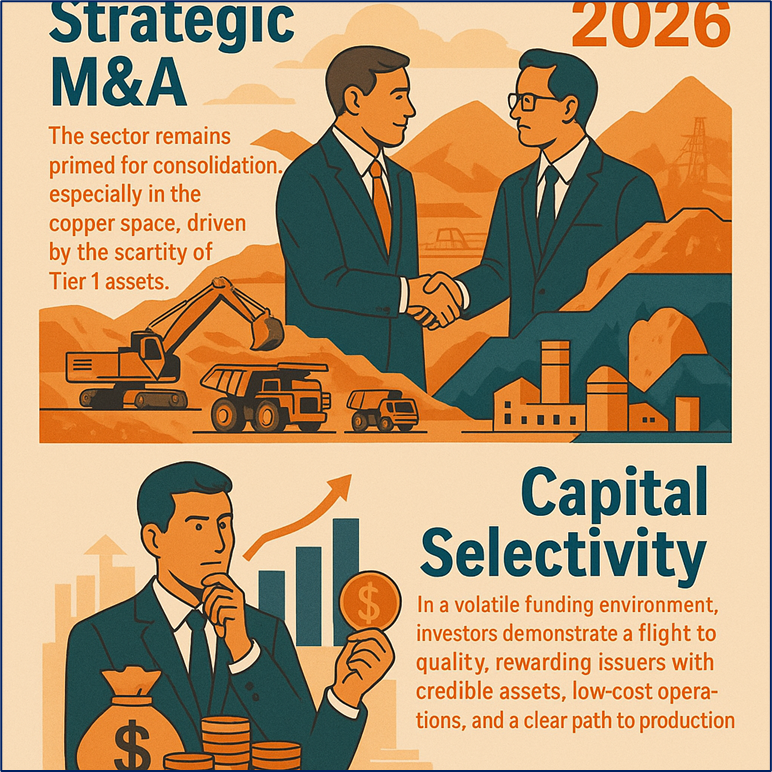

- Execution is the Primary Risk: For copper miners, the key factor influencing valuation in 2026 is the successful execution of ramp-ups at new Tier 1 assets (e.g., Teck's QB2) and the resolution of major geopolitical disruptions (e.g., First Quantum's operations).

- Global Demand & Supply Dynamics Shaping 2026

The market trajectory for 2026 is fundamentally defined by the imbalance between accelerating demand and constrained new supply delivery across all three metals.

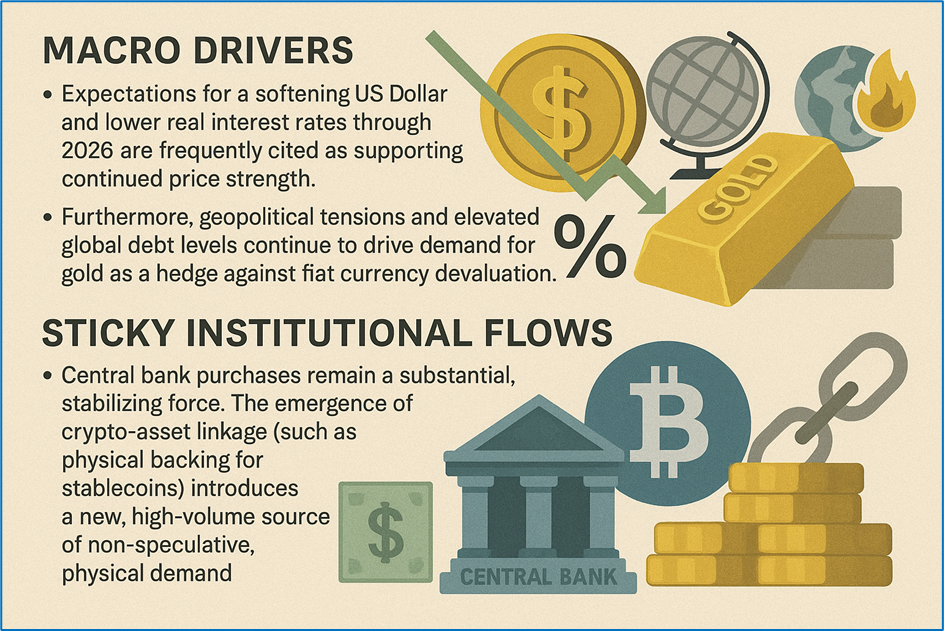

Gold (Au): Macro Hedging and Sticky Demand

The outlook for gold in 2026 is anchored by two persistent demand pillars:

Source: Kalkine Group

Copper (Cu): The Electrification Squeeze

Copper remains indispensable for the global energy transition, which is creating non-cyclical demand that supply struggles to meet.

- Structural Demand: Core drivers for 2026 include the sustained acceleration of:

- Electric Vehicle (EV) Production: EVs utilize approximately 3.6 times more copper than internal combustion engine vehicles.

- Grid Modernization: Large-scale infrastructure projects (e.g., in the US and Europe) and China's Ultra-High Voltage expansion require massive volumes of copper cabling.

- Emerging AI/Data Centre Buildout: Hyperscale data centres represent a new, high-intensity copper user for power distribution and cooling systems.

Source: Kalkine Group

- Supply Forecast: Despite strong price signals, the refined copper market is forecast by some institutions (like the ICSG) to swing into a deficit of ~150,000 tonnes in 2026, with others projecting shortfalls significantly higher (~400,000 tonnes). This constraint is attributed to aging mines, declining ore grades, and recent operational disruptions.

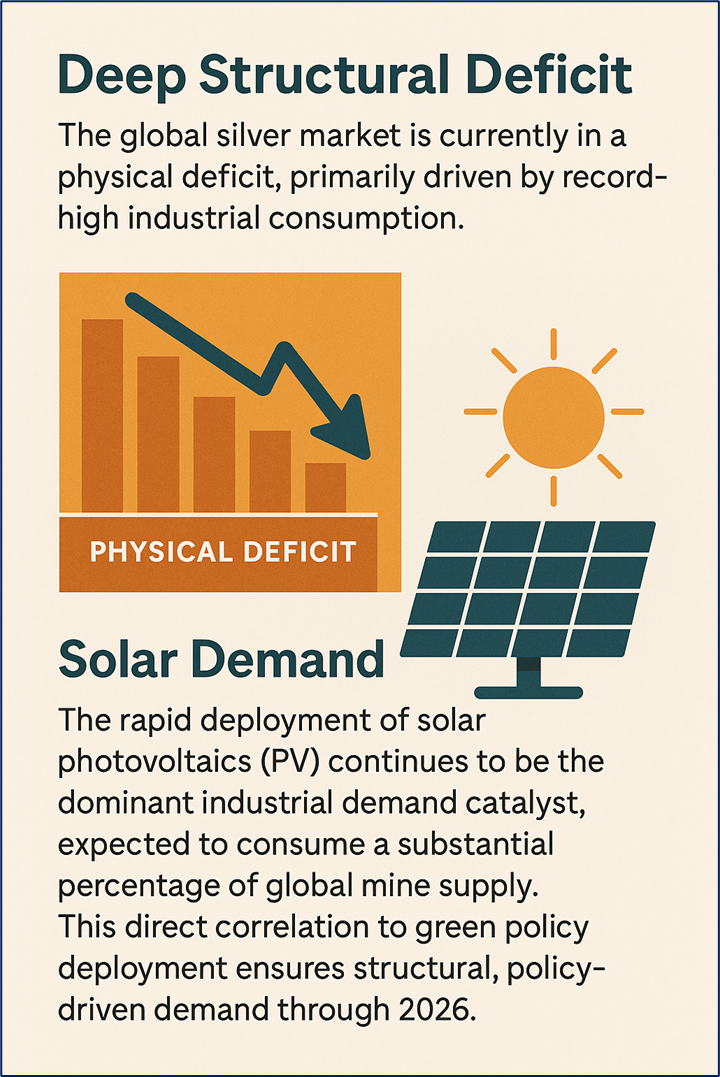

Silver (Ag): Industrial Engine of the Green Transition

Silver’s unique dual role as an industrial metal and a monetary asset positions it for high leverage to the energy transition.

Source: Kalkine Group

- Investment Drivers and Regulatory Environment

Canada's policy and capital markets define the operating environment for TSX-listed miners.

Regulatory and Policy Trajectory for 2026

The focus shifts from strategy planning to implementation, impacting project timelines and risk.

- CMS Project Acceleration: The federal government’s commitment of funds and the designation of certain minerals as essential under the Defence Production Act signals a concerted effort to accelerate permitting and development for projects aligned with national security and allied supply chains.

- Indigenous Partnerships: Successful, early-stage engagement and establishment of benefit agreements will increasingly be viewed by the market as a critical de-risking factor and a prerequisite for attracting strategic capital and achieving regulatory approvals.

- ESG Reporting and Technology: Institutional investors are prioritizing companies demonstrating advanced technology adoption (AI, automation) and transparent, high-quality ESG disclosure.

Capital Markets Drivers

The TSX maintains its role as the global capital pool for the sector.

Source: Kalkine Group

- TSX Stock Landscape: 2026 Catalysts and Operational Focus

The following list provides a cross-section of TSX-listed companies across the three metals, focusing on their specific operational and financial watchpoints for the 2026 reporting cycle.

Major Producers and Diversified Miners (Gold/Copper/Zinc)

- Agnico Eagle Mines (TSX: AEM): Focus is on capital allocation given its significant net cash position (over $2.1B as of Q3 2025). Operational catalysts include the ramp-up of the high-grade East Gouldie project and optimization of the Detour Lake asset.

- Barrick Gold (TSX: ABX): Primary focus is the successful execution of its Tier 1 asset strategy and the advancement of its copper exposure through the Reko Diq project. Cost control across its global portfolio remains a critical determinant of 2026 margins.

- Teck Resources (TSX: TECK.B): Post-divestiture, the company is evaluated strictly as a pure-play copper producer. The key watchpoint is the stabilization and full ramp-up of Quebrada Blanca Phase 2 (QB2), particularly after the Q4 2025 guidance revisions related to TMF constraints.

- First Quantum Minerals (TSX: FM): The central factor for 2026 is the resolution of the Cobre Panamá dispute, following the decision to suspend arbitration and seek direct negotiation. This outcome will fundamentally determine the company's copper production profile.

- Newmont (TSX: NGT): As the world’s largest gold producer, the focus in 2026 is on portfolio rationalization following its acquisition activity and integration of new copper assets to align with the energy transition demand.

- Kinross Gold (TSX: K): Operational focus centers on cost management at its flagship Tasiast mine and execution of development projects to sustain its production profile in non-Canadian jurisdictions.

- B2Gold (TSX: BTO): The execution of its growth pipeline, specifically the Goose Project in Nunavut, Canada, is key to maintaining gold production levels in the medium term.

Silver and Polymetallic Players

- Pan American Silver (TSX: PAAS): Focus remains on the integration of the Yamana assets and delivering consistent operational performance. The long-term growth catalyst is the development timeline for the La Colorada Skarn project.

- Aya Gold & Silver (TSX: AYA): The primary focus is achieving steady-state commercial production and consistency at the recently expanded Zgounder mine in Morocco, providing high-leverage exposure to silver price movements.

- Fortuna Silver Mines (TSX: FVI): Operations are focused on its diversified portfolio (gold/silver) across the Americas and West Africa. Key watchpoints include performance stability at its newly ramped-up assets.

Mid-Tier and Growth-Focused Copper/Base Metals

- Capstone Copper (TSX: CS): Valuation trajectory is tied to the successful ramp-up of the Mantoverde Sulphide project in Chile, which is designed to significantly increase the company’s copper output capacity in 2026.

- Lundin Mining (TSX: LUN): Focus on maximizing production and achieving cost guidance across its diversified portfolio (copper, nickel, gold) and integrating recent acquisitions.

- Hudbay Minerals (TSX: HBM): Operational execution at its copper/gold assets in Peru and the successful development of its new copper projects in North America are key determinants of its 2026 production profile.

- New Gold (TSX: NGD): Focus on sustaining improved grades and operational stability at Rainy River and the successful ramp-up of the New Afton C-Zone to maximize copper and gold by-product credit.

- Sherritt International (TSX: S): As a key producer of nickel and cobalt (other critical minerals), its performance is largely tied to the stability of its Cuban joint venture and the trajectory of the battery metals market.

- Equinox Gold (TSX: EQX): Execution of its large-scale gold development pipeline, specifically the ramp-up of new mines, is critical to achieving its target production growth trajectory.

- Analytical Conclusion: The 2026 Duality

The 2026 trajectory for the Canadian mining sector is characterized by a duality:

- Macro-Financial Strength: The sector is supported by high gold prices, deeply structural deficits in critical minerals (copper/silver), and Canada's stable position as a capital market hub.

- Operational and Geopolitical Risk: This high-price environment is undermined by the high risk associated with delivering new supply (operational execution, cost inflation) and navigating complex geopolitical and permitting challenges.

For clients, the narrative in 2026 will therefore shift from simply identifying demand to identifying companies that can reliably execute on existing projects and mitigate operational risks to capitalize on historically strong price environments.

Please wait processing your request...

Please wait processing your request...