Finding multi-bagger potential in the mature Canadian banking sector requires looking beyond simple yield and focusing on "total return" compounding—where stock buybacks, dividend hikes, and earnings multiple expansions converge.

As of early 2026, the sector is navigating a "K-shaped" economic recovery, where high-income resilience and a steepening yield curve are creating a tailwind for select lenders.

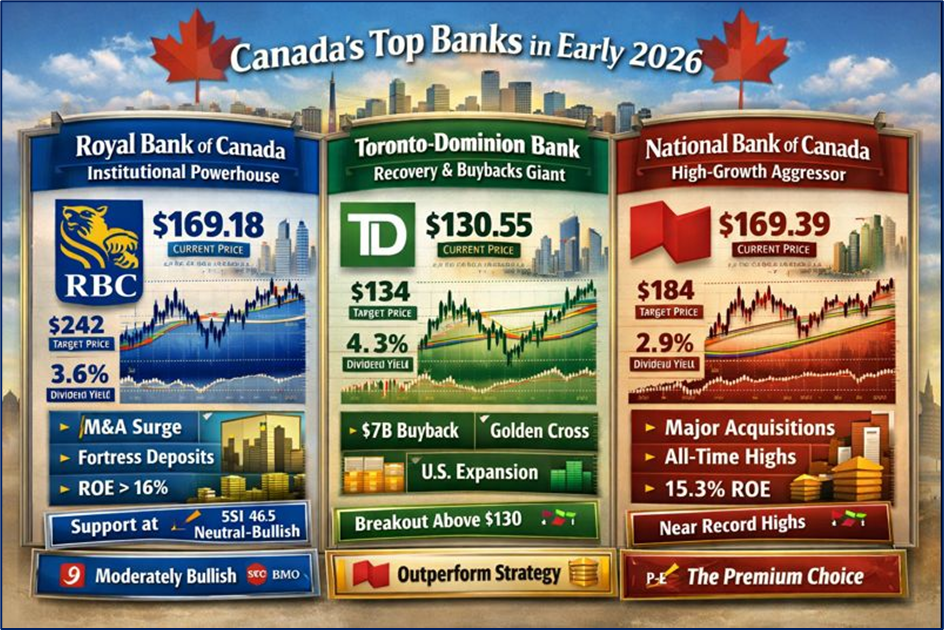

Source: Kalkine Group

1. Royal Bank of Canada (TSX: RY) – The Institutional Powerhouse

Royal Bank remains the definitive "Gold Standard" for institutional investors. Its massive scale and successful integration of high-margin wealth segments have allowed it to maintain a dominant market share.

- Key Drivers: 2026 has seen RY capitalize on the global resurgence of M&A activity through its Capital Markets division. Domestically, its "fortress" deposit base provides a low-cost funding advantage that peers struggle to match.

- Technical Analysis: As of Jan 19, 2026, RY is trading near $169.18, showing strong resilience. It is comfortably maintaining support above its 200-day moving average of $162.85. The RSI (14-day) sits at 46.5, indicating a neutral-to-bullish stance with significant "headroom" before reaching overbought territory.

- Analysts & Smart Money: Sentiment is "Moderately Bullish" to "Buy." Scotiabank recently boosted its price target to $242.00, and BMO Capital Markets raised theirs to $245.00, citing RY's superior ROE (Return on Equity) which remains above 16%.

- Dividends & Value: With a quarterly dividend of $1.48, RY yields roughly 3.6%. Its robust CET1 ratio of 15.1% ensures that further dividend hikes or tactical acquisitions remain highly likely in late 2026.

2. Toronto-Dominion Bank (TSX: TD) – The Recovery & Buyback Giant

After navigating regulatory hurdles in previous years, TD has reinvented itself as the premier "capital return" play of 2026.

- Key Drivers: TD’s "2026 Playbook" focuses on its massive U.S. retail footprint and wholesale banking growth. The bank is currently executing a landmark $7 billion share repurchase program (NCIB), which is significantly boosting earnings per share (EPS).

- Technical Analysis: TD is a momentum favorite in Q1 2026, having recently cleared its 200-day moving average of $112.27. The stock is currently trading around $130.55, successfully testing the psychological resistance level of $130. A "Golden Cross" (50-day moving average at $123.69 crossing the 200-day) confirms a long-term bullish trend.

- Analysts & Smart Money: Upgrades are frequent; National Bank Financial recently moved TD to "Outperform" with a target of $134.00, while BMO has set a high-water mark of $135.00.

- Dividends & Value: TD offers a sector-leading yield of 4.3% based on a quarterly payout of $1.08. Trading at a P/E of 11.3x, it remains the best value-unlocking candidate among the majors.

3. National Bank of Canada (TSX: NA) – The High-Growth Aggressor

National Bank continues to be the "alpha" of the group, focusing on agility and high-margin segments rather than broad geographical expansion.

- Key Drivers: NA’s recent strategic acquisitions of the Canadian Western Bank and Laurentian Bank portfolios have transformed it from a regional player into a national contender. It reported a staggering 15.3% ROE in its latest quarterly results.

- Technical Analysis: NA is currently trading at $169.39, hovering just below its all-time high of $177.54. It remains a momentum leader with a stair-step chart pattern. Technical support is firm at $162.00, and the stock remains highly sensitive to broader TSX 60 moves (Beta: 1.15).

- Analysts & Smart Money: Scotiabank maintains a "Buy" rating with a "blue-sky" target of $184.00. Analysts expect 5–10% EPS growth through the remainder of 2026 as acquisition synergies materialize.

- Dividends & Value: While the yield is a more modest 2.9%, NA boasts the highest dividend growth rate in the sector. It is the "premium" choice, trading at a P/E of 17.1x, justified by its industry-leading growth metrics.

Conclusion & Outlook

The 2026 outlook for Canadian banks is defined by capital strength. While risks like U.S. trade policy (USMCA) and housing market sensitivity remain, the "Big 3" discussed above are currently the primary targets for "smart money" seeking a blend of safety and aggressive compounding.

Note - Keep a close eye on the January 28, 2026, earnings reports; any beat on the $3.15–$3.30 EPS consensus across the sector could trigger the next major leg up.

Please wait processing your request...

Please wait processing your request...