The Federal Funds Rate (FFR) is arguably the single most important interest rate in the global financial system. It’s the tool the U.S. Federal Reserve (the Fed) uses to manage the economy, influencing everything from the cost of your mortgage to the profitability of major companies. For retail investors, 'smart money,' and institutional managers alike, mastering this rate is the key to navigating market volatility and maximizing portfolio returns.

They are two independent central banks, but when the U.S. Federal Reserve (The Fed) and the Bank of Canada (BoC) make rate decisions, they rarely act in isolation. The rate set by the Fed (the Federal Funds Rate, or FFR) and the rate set by the BoC (the Target for the Overnight Rate) are locked in a high-stakes, decades-long correlation. This correlation is the most crucial factor for Canadian investors, influencing everything from the value of the Canadian Dollar (the 'Loonie') to the strength of the Canadian housing market.

The Core Correlation: Same Storm, Different Boats

Historically, the FFR and the BoC's Overnight Rate have moved in the same general direction. When the US tightens (raises rates) to fight inflation, Canada usually follows suit. When the US eases (cuts rates) to stimulate growth, Canada generally tags along.

Why the Close Tie? (The North American Economic Engine)

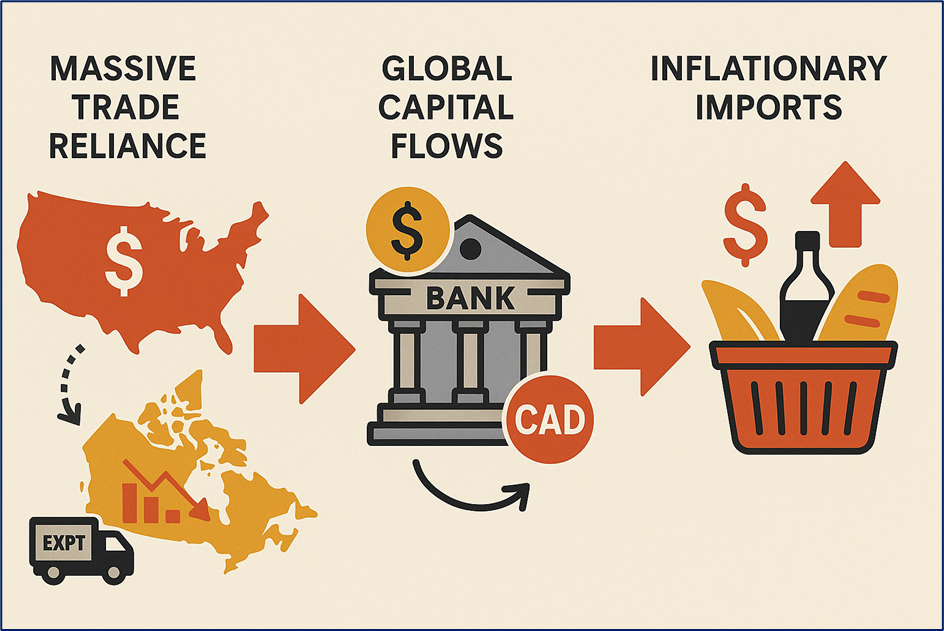

- Massive Trade Reliance: Canada's economic health is fundamentally tied to the US. A vast majority of Canadian exports go south of the border. If the Fed raises rates and slows the U.S. economy, demand for Canadian goods slows, putting downward pressure on Canada's growth and, eventually, its own interest rates.

- Global Capital Flows: The US financial market is the world's largest. If the FFR is significantly higher than the BoC rate, global "smart money" and institutional investors pull capital out of Canadian dollar assets (like government bonds) and move it into higher-yielding, safer US assets. This massive outflow of money weakens the Canadian Dollar (CAD).

- Inflationary Imports: When the CAD weakens due to the rate gap, it makes imports from the US (and globally, since many goods are priced in US Dollars) more expensive for Canadian consumers. This causes imported inflation, forcing the BoC to raise rates just to offset the currency's decline.

Source: Kalkine Group

The Crucial Difference: Why Divergence is Possible (The "Whipsaw")

Despite the correlation, the BoC is not a puppet of the Fed. Its primary job is to manage Canadian domestic conditions (Canadian inflation and employment). This difference in mandate and underlying economic structure creates opportunities for divergence—the "whipsaw" moments that investors must watch.

- The Domestic Debt Difference (Canada's Achilles' Heel)

- Canada's High Household Debt: Canadian households carry significantly higher levels of debt (especially mortgage debt) compared to their US counterparts. Crucially, Canadian mortgages also tend to have shorter refinancing terms (often 5 years vs. 30 years fixed in the US).

- BoC Sensitivity: This means the Canadian economy is far more rate sensitive. A 1% rate hike in Canada hits the Canadian consumer much faster and harder than a similar hike hits the US consumer. This domestic vulnerability gives the BoC reason to be less aggressive or to start cutting rates sooner than the Fed, as has been seen in recent periods of divergence.

- The US Dollar Factor

- A widening gap (FFR > BoC Rate) usually leads to a weaker Loonie. While a weak Loonie helps Canadian exporters by making their goods cheaper for US buyers, it also causes sticky imported inflation, which the BoC must weigh carefully. Historically, the BoC can tolerate a divergence of around 150 basis points (1.5%) before the pressure on the Loonie becomes a major inflationary concern.

Fed Funds Rate: Definition and Methodology

- The Definition: Banks Borrowing from Banks

The Federal Funds Rate (FFR) is the target interest rate set by the Federal Open Market Committee (FOMC) at which depository institutions (banks and credit unions) lend their excess reserves to other depository institutions overnight. This lending occurs on an uncollateralized basis.

- The rate you see reported is the Effective Federal Funds Rate (EFFR), which is the volume-weighted median of all overnight federal funds transactions.

- The FOMC sets a target range (e.g., 3.75%–4.00%), and the Fed uses its tools to steer the EFFR within that range.

- The Methodology: Steering the Rate

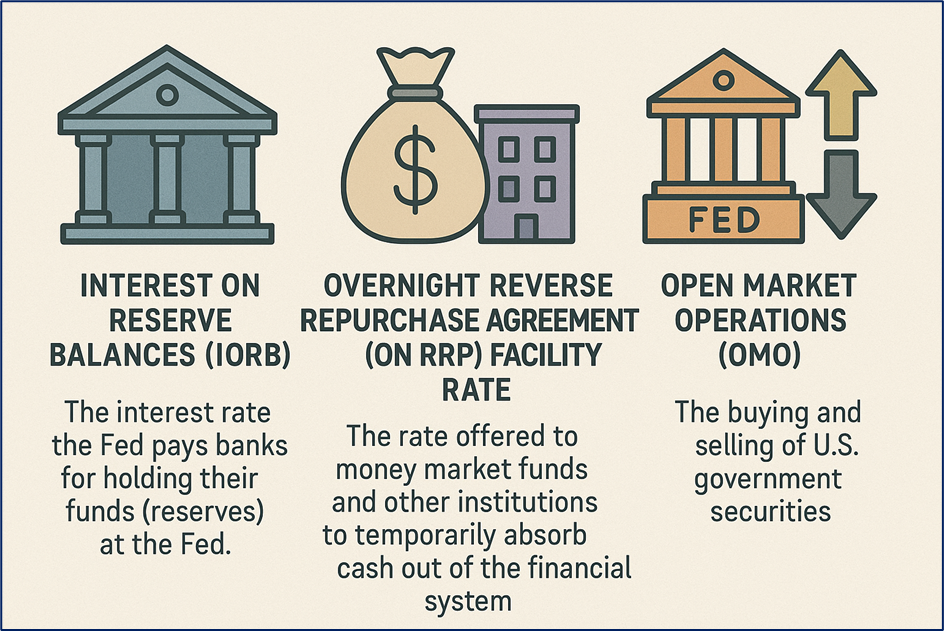

The Fed doesn't directly set the FFR; it steers the EFFR within the target range using several administered rates:

- Interest on Reserve Balances (IORB): The interest rate the Fed pays banks for holding their funds (reserves) at the Fed. This acts as a floor, as banks won't lend to others below what the Fed pays them risk-free.

- Overnight Reverse Repurchase Agreement (ON RRP) Facility Rate: The rate offered to money market funds and other institutions to temporarily absorb cash out of the financial system. This provides an additional, tighter floor for short-term rates.

- Open Market Operations (OMO): The buying and selling of U.S. government securities. Buying securities injects money (liquidity) into the system, which puts downward pressure on the FFR. Selling securities removes money, putting upward pressure on the FFR.

Source: Kalkine Group

How to Calculate Rate Hike Probability

The market's expectation for the FFR is calculated using Fed Funds Futures contracts traded on exchanges like the CME Group. These contracts settle based on the average Effective Federal Funds Rate (EFFR) for a given month.

The key assumption for a 25-basis point (bp) rate move is that the average monthly EFFR change reflects the probability of a hike/cut. The CME Fed Watch Tool is the common source, which applies the following basic logic for an upcoming meeting:

Probability of a Rate Hike (P-Hike):

The probability is derived from the price of Fed Funds Futures contracts. These contracts are a betting mechanism on the average effective federal funds rate for a given month.

The Formula (Simplified)

The implied probability of a rate change is roughly calculated by comparing the current futures price to the prices that would prevail if the rate were cut or held constant.

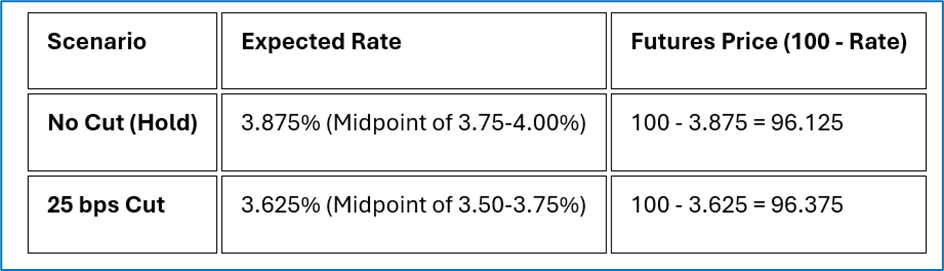

- A Fed Funds Futures contract expiring in the month of the meeting is priced at:

Price = 100 – (Expected Federal Funds Rate)

Calculation Example (Illustrative)

- Current Target Rate: 3.75% - 4.00%

- Current Futures Price: Let's say the December futures contract settles at a price implying an effective rate of 3.65%.

Source: Kalkine Group

Actual Market Price (Implied Rate of 3.65%): 100 - 3.65 = 96.35

The actual market price (96.35) is much closer to the 25 bps Cut Price (96.375) than the No Cut Price (96.125).

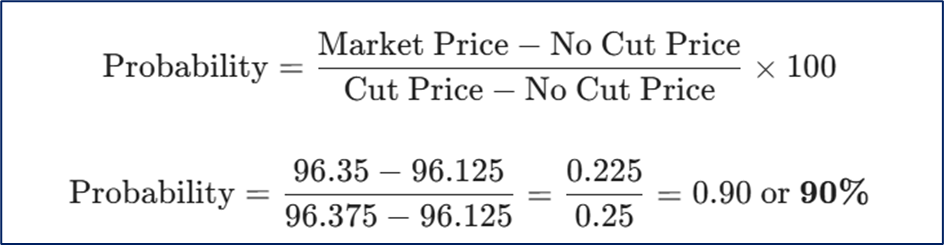

The probability of the 25 bps Cut is calculated based on how far the market price is along the spectrum between the two scenario prices:

Source: Kalkine Group

Monetary Policy Strategy and Outlook

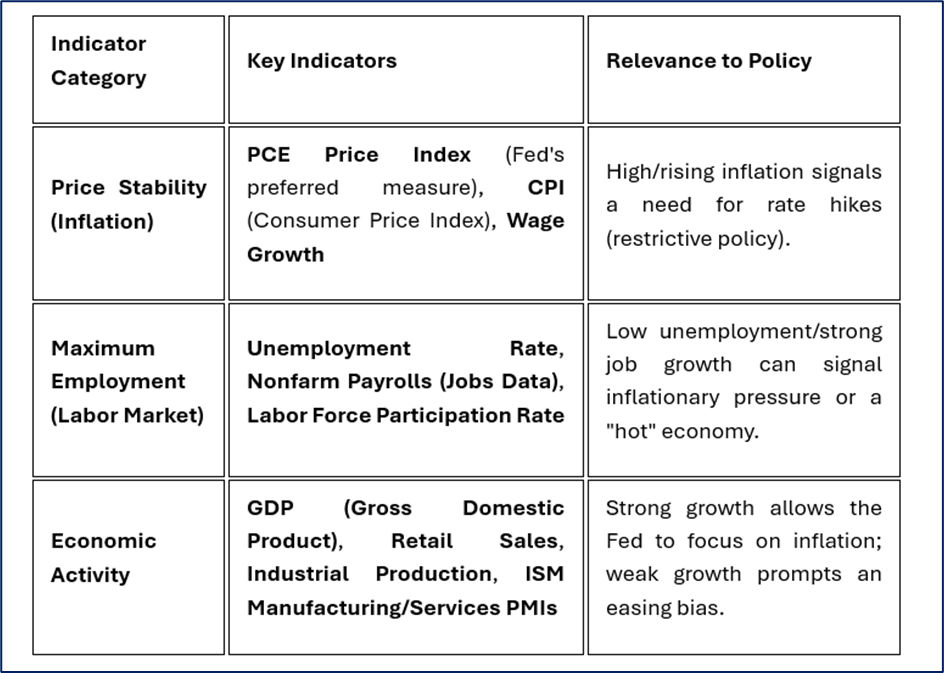

The Fed operates under a "dual mandate" set by Congress: to promote maximum employment and stable prices (which the FOMC defines as 2% inflation, measured by the Personal Consumption Expenditures (PCE) price index).

- Current Strategy: The Fed uses the FFR to manage aggregate demand. Raising rates is a restrictive (tightening) policy to slow the economy and fight inflation. Lowering rates is an accommodative (easing) policy to stimulate growth and employment.

- Outlook: The official outlook is usually communicated through the FOMC Statement and the Chair's press conference, focusing on the trade-off between fighting inflation and sustaining a strong labor market.

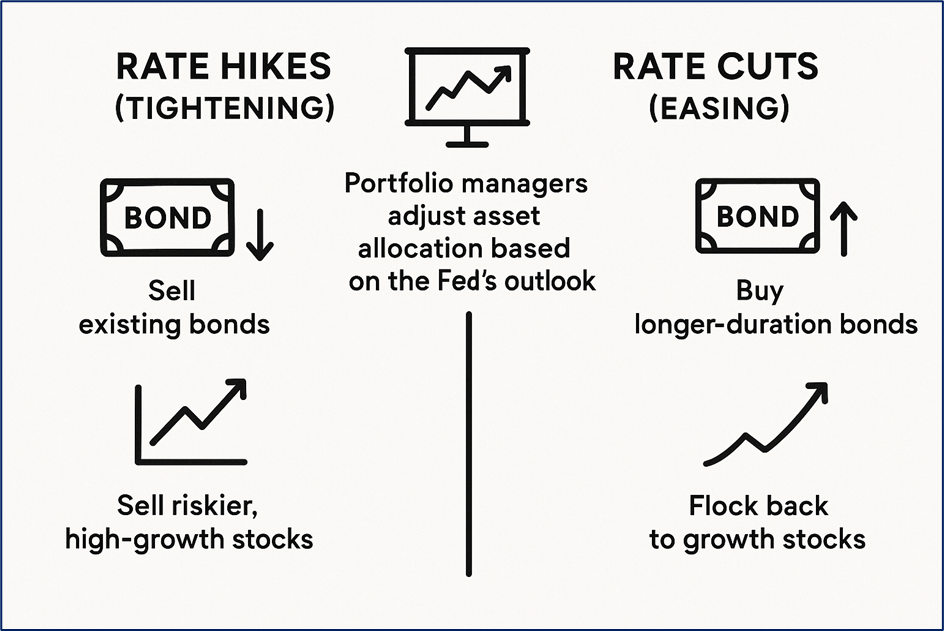

Smart Money & Institutional Investor Updates

Smart money (hedge funds, sophisticated institutional investors, and portfolio managers) reacts instantly to Fed communications, often attempting to front-run rate changes.

- Rate Hikes (Tightening):

- Bonds: They sell existing bonds, as higher rates mean newly issued bonds offer higher yields, making older bonds less valuable. The goal is to lock in higher, safer yields on cash/short-term instruments.

- Stocks (Growth/Tech): They sell riskier, high-growth stocks. Higher borrowing costs reduce future corporate profits (discounted back to the present), and a slower economy hurts growth.

- Rate Cuts (Easing):

- Bonds: They buy longer-duration bonds to lock in yields before they fall further.

- Stocks (Growth/Tech): They flock back to growth stocks, as lower borrowing costs and a stimulative environment boost future earnings estimates.

Portfolio Managers use the Fed's outlook to adjust their asset allocation: increasing fixed income exposure when yields are high and shifting to equities when rate cuts signal a supportive economic recovery. They closely monitor the spread between the 2-year and 10-year Treasury yields, which is a classic macro indicator.

Source: Kalkine Group

Macro Indicators the Fed Watches

The Fed uses a host of indicators to gauge the economy's health, focusing on the dual mandate:

Source: Kalkine Group

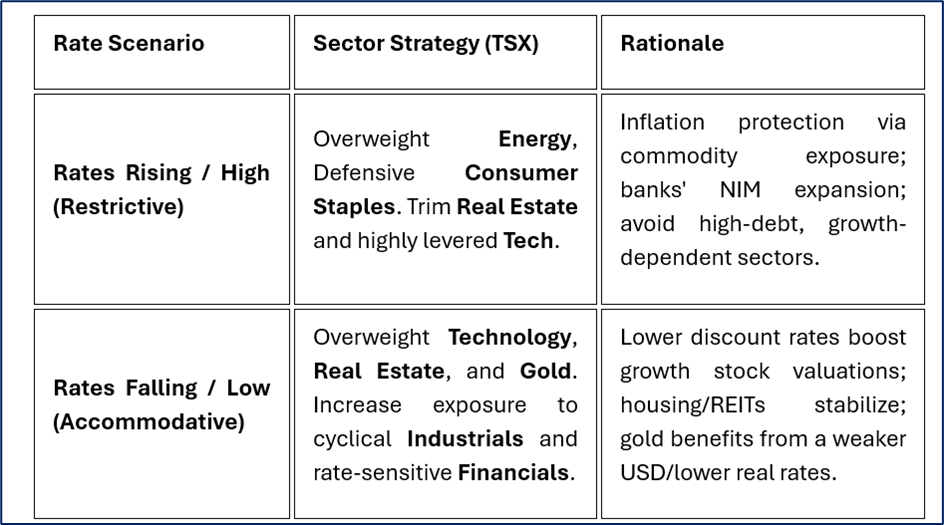

Canadian Market Watch: Sectors and Stocks to Navigate the Rate Cycle

The Canadian market (S&P/TSX Composite Index) is fundamentally different from the US market due to its heavy concentration in Financials, Energy, and Materials. This concentration makes the Canadian economy and its stock market highly sensitive to both domestic (Bank of Canada - BoC) and US (Federal Reserve - Fed) interest rate moves, as well as global commodity prices.

1. High-Interest Rate Sensitivity Sectors

These sectors are directly impacted by interest rates, either due to their reliance on debt or their status as rate-sensitive income plays.

A. Financials (Banks and Insurance)

- Impact of High Rates (Initial): Higher rates are often positive initially as banks' Net Interest Margins (NIM) expand—they earn more on loans than they pay on deposits.

- Impact of Prolonged High Rates/Recession: Negative. Prolonged high rates increase the risk of loan defaults (especially in highly indebted Canadian housing), leading to higher provisions for credit losses.

- Stocks to Watch: Royal Bank of Canada (RY), TD Bank (TD), Bank of Nova Scotia (BNS). Look for banks with lower exposure to housing or stronger balance sheets if a rate-induced recession is feared.

B. Real Estate (REITs and Developers)

- Impact: Extremely Negative under high-rate environments. High mortgage rates (influenced by BoC and Fed rates) crush housing affordability, slow transaction volumes, and increase the cost of financing for commercial real estate and REITs. Canada's high household debt load makes this sector particularly vulnerable.

- Stocks to Watch: Canadian Apartment Properties REIT (CAR.UN) (residential focus), RioCan REIT (REI.UN) (commercial focus), Brookfield Corp. (BN) (global asset manager with real estate exposure).

C. Utilities and Telecommunication Services

- Impact: Negative under high rates. These sectors are often viewed as bond proxies for their stable, dividend-paying income. Since they rely heavily on debt to fund infrastructure projects, high rates increase borrowing costs and reduce the present value of their future cash flows.

- Stocks to Watch: Fortis Inc. (FTS), BCE Inc. (BCE), Telus Corp. (T). Their attractiveness increases as rates begin to fall.

2. Global/Commodity-Driven Sectors

These sectors are less directly sensitive to the level of Canadian interest rates but are highly sensitive to global economic growth (which the Fed Funds Rate heavily influences) and commodity prices.

A. Materials (Gold, Copper, Mining)

- Impact: Complex. Generally, lower US rates weaken the US Dollar, which makes dollar-denominated commodities (like gold and copper) cheaper for foreign buyers, boosting their price. Gold often moves inversely to real interest rates (nominal rate minus inflation). A rate cutting cycle often benefits gold.

- Stocks to Watch: Barrick Gold Corp. (ABX), Teck Resources (TECK.A/B), Agnico Eagle Mines Ltd. (AEM).

B. Energy (Oil & Gas)

- Impact: Indirect. Energy prices are driven by global supply/demand. However, higher global growth expectations (which often follow a US rate cut or a strong economic outlook) boost demand for crude oil and natural gas, benefiting Canadian producers.

- Stocks to Watch: Suncor Energy Inc. (SU), Canadian Natural Resources (CNQ), Enbridge Inc. (ENB) (pipeline/midstream stability).

3. Growth and Trade-Sensitive Sectors

A. Information Technology

- Impact: Highly Sensitive to US Fed Funds Rate. As with US tech, Canadian tech valuations are based heavily on future growth. High US rates significantly impact the Discounted Cash Flow (DCF) models used to value these companies, hitting growth stocks the hardest. A Fed rate-cutting cycle acts as a powerful tailwind.

- Stocks to Watch: Shopify Inc. (SHOP), Constellation Software Inc. (CSU), CGI Inc. (GIB.A).

B. Industrials (Trade/Auto/Lumber)

- Impact: Sensitive to Trade and Global Demand. Firms involved in trade (autos, lumber, machinery) are sensitive to USMCA policy and cross-border demand, which is tied to the health of the US consumer and US manufacturing (both influenced by the Fed).

- Stocks to Watch: Canadian Pacific Kansas City (CP) (Rail), Waste Connections Inc. (WCN), Bombardier Inc. (BBD.B).

Portfolio Action: Positioning for Rate Moves

Source: Kalkine Group

Conclusion: Decoding Your Financial GPS

The Federal Funds Rate is the ultimate financial GPS, determining where global capital flows. For Canadian investors, this requires a dual focus:

- Track the Fed: Pay close attention to the Dot Plot and U.S. macro indicators, as the U.S. policy sets the global gravity well.

- Watch the BoC Divergence: Understand that Canada's high household debt is its key vulnerability, giving the BoC justification to move independently.

Mastering this delicate, intertwined dance between the FFR and the Overnight Rate is not just about economics—it is about positioning your portfolio to thrive, regardless of which way the North American rate roller coaster turns.

Please wait processing your request...

Please wait processing your request...