Key Takeaways

- Markets appear resilient on the surface, but cross-asset stress is building beneath: commodities, crypto, FX, and rates are flashing caution.

- Tech and AI valuations face their toughest scrutiny in months as mega cap crowding hits extreme levels.

- Top investment banks turn more defensive - focusing on liquidity, quality and risk-control, not aggressive positioning.

- Broad commodity weakness hits oil, copper, silver and natural gas amid dollar strength and soft demand expectations.

- Crypto ETFs record significant outflows, signalling a shift from momentum euphoria to defensive allocations.

- Volatility in bonds and currencies intensifies as rate-cut expectations drift further out.

- Market flows now matter more than headlines — and correlations across asset classes are climbing sharply.

- Investors globally are tilting toward diversification and lower-beta exposures.

Markets can pivot faster than before - in either direction. The next big move may not be slow, and it may not be subtle.

Global Markets: Strength at the Surface, Stress Below the Waterline

Markets ended the week mixed - strong sessions in parts of global equities, but clear fragility across commodities and crypto. Investment-bank tone is unified across the board: constructive but increasingly cautious.

Equities: Optimism Tempered by Tech Valuation Stress

Despite pockets of strength, the broader weekly tone was soft. Tech-heavy indices, especially in the U.S., struggled with valuation fatigue and sensitive positioning around interest-rate expectations.

Data Source - EODHD/Others, Nasdaq-100 one year chart, 21 Nov 2025

Two dominant themes drove equity sentiment:

- Extreme concentration in AI & megacap tech trades

- Uncertainty around the timing and pace of upcoming rate cuts

What the Big Banks Are Saying

- BlackRock: Maintaining U.S. overweight but warns of overheating and crowding in AI mega-caps.

- Goldman Sachs: Notes momentum remains dangerously concentrated in a handful of tech giants.

- Morgan Stanley: Says current positioning is fragile and heavily dependent on perfect macro conditions.

- JP Morgan: Preparing clients for higher volatility as policy narratives shift.

- UBS: Highlights rising cross-asset correlations — raising the need for careful risk budgeting.

Fixed Income & FX: Macro Crosswinds Intensify

Bond yields swung sharply throughout the week as markets pushed out expectations for meaningful rate cuts.

FX volatility picked up too — with the Japanese yen weakening even during risk-off periods, a signal of underlying instability in currency markets.

Commodity Corner: Oil, Metals & Precious Markets Slide Together

Commodities were under heavy pressure this week:

- Oil: Fell on soft demand signals and unwinds in speculative positioning.

- Copper & Industrial Metals: Reacted negatively to growth worries across Europe and China.

- Silver: Dropped as real yields rose and the dollar strengthened.

- Natural Gas: Faced downside pressure amid warmer-weather expectations and oversupply signals.

Trading desks at Citi, BofA and Barclays all reported defensive flows and a shift away from high-beta commodity exposures.

₿ Crypto: ETFs See Outflows, Sentiment Turns Defensive

The crypto market’s mood shifted sharply as spot-Bitcoin ETFs recorded substantial outflows. Analysts note a transition from momentum chasing to capital preservation, aligning more closely with broader risk-off tendencies.

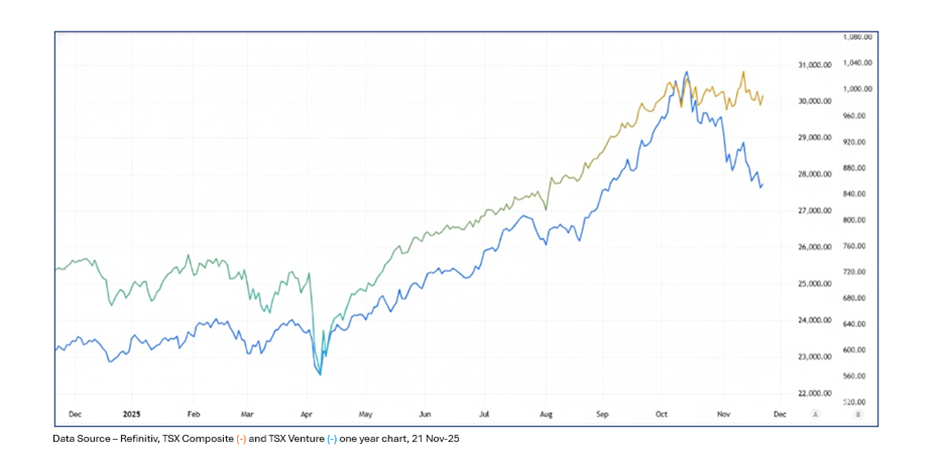

Canada Weekly Equity Markets Roundup: A Defensive Tone with Commodity Drag

Canada’s markets mirrored the global risk tone this week — defensive, cautious, and led by movement in commodities and rates.

TSX Performance Snapshot (Weekly Mood)

- The TSX Composite absorbed pressure from falling oil and metals, while defensive sectors provided stability.

- The TSX Venture remained subdued as small-cap risk appetite faded.

Canada Sector Trends This Week

Energy

Oil weakness pulled the entire sector down. Heavyweights like Suncor, Cenovus, and Canadian Natural Resources faced broad selling as crude retreated.

Materials & Mining

Copper and precious-metal softness weighed on First Quantum, Teck, Barrick, and Agnico Eagle. Global growth uncertainty remains the biggest headwind for this sector.

Financials

Canadian banks were relatively stable. RY, TD, BMO saw modest moves — with investors positioning cautiously ahead of next month’s earnings updates and loan-loss trends.

Industrials & Railways

Names like Canadian National Railway and CP held firmer as investors rotated into cash-flow-reliable businesses.

Technology (Canada’s Growth Pocket)

Mirroring global trends, Lightspeed, Shopify, Nuvei and other growth-centric names saw softer action as valuation sensitivity increased.

What Canadian Portfolio Managers Are Highlighting

Leading insights from RBC GAM, TD Asset Management, CI Global Asset Management, and Fidelity Canada emphasised:

- Quality Over Momentum

Focus is shifting toward companies with:

- strong balance sheets

- reliable dividends

- resilient cash flows

- pricing power

- Energy & Materials Are the Wildcards

A stabilisation in oil, gold and copper could quickly alter the TSX’s trajectory.

- Rates Still Dominate Market Direction

Bank of Canada tone remains a key driver — especially for rate-sensitive sectors like housing, utilities, and consumer cyclicals.

- U.S. Macro Matters More Than Domestic Data

Canada remains tightly correlated to U.S. yields, tech sentiment, and global liquidity trends.

Forward Strategy Themes Emerging Across Global & Canadian Markets

- Selective equity participation (less broad buying, more targeted).

- Growing fatigue in AI & growth-driven trades.

- Multi-asset diversification gaining traction.

- Higher reliance on macro data and fund flows.

- Increasing probability of sharp, nonlinear market swings.

Final Word: Markets Are Entering a High-Velocity Phase

This week marks a turning point. Global equities are holding on — but commodities, crypto, and FX markets are signalling deeper stress.

We’ve entered a regime where:

- liquidity is thinner

- valuations are elevated

- cross-asset volatility is rising

- correlations are tightening

Please wait processing your request...

Please wait processing your request...